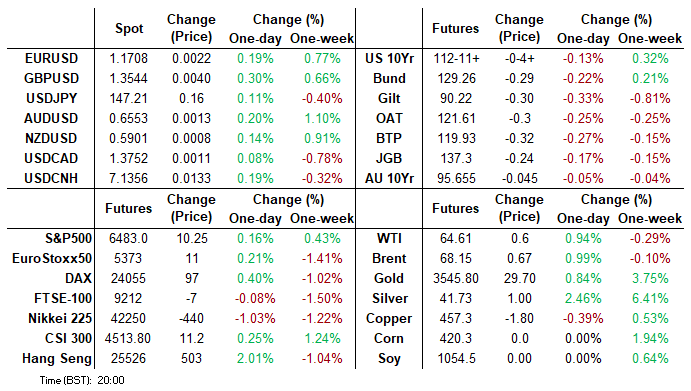

MNI ASIA MARKETS ANALYSIS - DXY Tilts Lower, US NFP Awaited

Highlights:

- US Dollar Index Tilts Moderately Lower, Labor Day Holiday Saps Momentum

- Modest Supply Pressure on EGBs/Gilts Sees Supports Tested

- Eurozone inflation data for August takes focus on Tuesday before US ISM Manufacturing PMI figures. Markets continue to gear themselves up for this week's key US employment report, due Friday.

US TSYS: Mildly Cheaper At The Labor Day Early Close

- Treasury futures dealt mildly cheaper at the early close for Labor Day after an unsurprisingly quiet session. There was no cash trading due to the holiday.

- Sell-off cues were taken from some mild weakness in EGBs on supply grounds.

- TYZ5 at 112-11+ (-04+) on cumulative volumes of 208k. An earlier low of 112-09+ saw lows since Aug 27, but as opposed to some support clearance in EGBs it didn’t come close to troubling support at 111-31 (20-day EMA).

- Technicals suggest the trend structure remains bullish with resistance at 112-20+ (Aug 28 high).

- At the front end, Fed Funds futures were mixed for near-term meetings, with Sept cut pricing building very slightly to 22.5bp priced vs a 0.5bp trimming for Dec with a cumulative 55.5bp.

- SOFR futures implied yields were up to 2.5bp higher from Friday’s close, with increases led by the SFRH7 which continues to see a terminal yield of sub-3% at 2.97% for ~135bp of cuts from current levels.

- President Trump’s Truth Social activity has also been light so far today, saying India’s offer to cut tariff rates to zero is getting late, hinting at pushes to tackle crime in Chicago, LA, NY and Baltimore and pushing “Pfizer and others” to show Covid drug success.

- US Tsy Sec Bessent meanwhile suggests that Trump may declare a “national housing emergency” this fall to address rising house prices, something last seen in 2008.

- Tomorrow is headlined by ISM mfg for August before labor data starts to take over in the usual build-up to the nonfarm payrolls report for August on Friday.

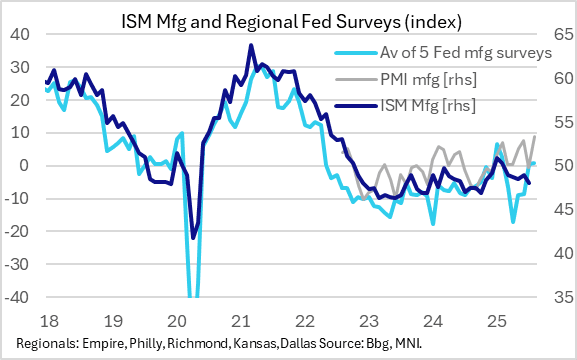

US OUTLOOK/OPINION: ISM Manufacturing Preview: Activity Set To Pick Up (1/2)

August's ISM Manufacturing report (out Tuesday Sep 2nd 1000ET) is seen by Bloomberg Consensus as showing a slight improvement to 48.9 from July's 48.0.

- The report will be published shortly after the final release of August S&P Global Manufacturing PMI, which showed a surprisingly strong 53.3 in the flash reading. That was the highest since December and marked a 2nd consecutive improvement. There has been a divergence in the ISM vs PMI readings of late, with ISM sagging as PMIs hit new recent highs.

- Additionally, the MNI Chicago Business Barometer slowed 5.6 points to 41.5 in August, though the decline wasn't quite as stark based on ISM weights.

- However the theme of general improvement is evident in the regional Fed banks' manufacturing surveys, which showed a 5th consecutive month of improvement on aggregate after April's trough, albeit roughly steady from July.

- That said, it was a mixed bag region-by-region in August's surveys. The Kansas City Fed's reading was steady, while there were improvements in New York and Richmond, and deteriorations in Dallas and Philadelphia.

- One theme across most of the regional Feds (4 out of 5, Philly the exception) saw improvements in new orders, which may tip the balance toward a solid manufacturing ISM.

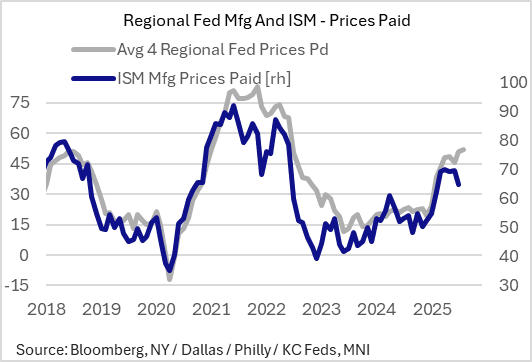

US OUTLOOK/OPINION: ISM Manufacturing Preview: Prices Paid Set To Rise (2/2)

For ISM Manufacturing Prices Paid, expectations are for a slight pickup to 65.0 from 64.8 prior. This looks to be on the low side versus the recent increase in regional Fed input prices indices: after a near 5-point pullback in July, we wouldn't be surprised by a rebound back toward the high 60s mark.

- Admittedly the regional Fed data was mixed: Philly and Dallas Fed gauges pushed to multi-month highs, though KC and Empire moderated slightly. Our gauge below doesn't include the Richmond Fed which uses a different metric: a 12-month % chg lookback, which leaped to a 28-month high in the month.

- Additionally, the S&P Global flash PMI report noted that in August "the manufacturing cost rise was especially large, being the second-steepest since August 2022", suggesting a resumption of upside price pressures.

EGBS-GILTS CASH CLOSE: Modest Pressure From Supply Sees Supports Tested

- Main EGB 10Y yields closed between 2.1-2.5bp higher today, extending Friday’s modest sell-off.

- OATs marginally led today’s sell-off, with fiscal uncertainty still weighing but OAT-Bund spreads at 79bps (just +0.2bp on the day) off last week’s highs of ~82.6bps.

- French PM Bayrou over the weekend looked to gain support ahead of the Sept. 8 confidence vote but acknowledged that talks with political parties may fail to save his government.

- BTPs meanwhile clawed back some of their earlier underperformance, having led losses into the mandate announcement for the dual 7- & 30-Year BTP syndication.

- Closing the gap, BTPs closed 0.1bp tighter vs Bunds (85.8bps). The syndication was well within the realm of possibilities, as outlined in our daily/weekly issuance documents, explaining the lack of meaningful subsequent market move.

- RXU5 trades at 129.26 (-29) off earlier lows of 129.07 that probed support at 129.15 (Aug 26 low), potentially opening a test of the bear trigger at 128.64 (Aug 15 low).

- Bear steepening seen on the German curve, with yields 1.1-2.2bp higher. 5s30s saw a fresh cycle closing high of 108.6bps. The March '19 high (111.78bp) presents the next upside target of note.

- This week's uptick in EGB supply, and the impending pricing of the EFSF syndication, provide headwinds for regional bonds.

- Gilts led losses in European hours meanwhile, with 10Y yields closing +3bps.

- Slightly softer-than-flash final manufacturing PMI data did little for the market, but probably helped prevent a breach of early London lows.

- Futures last -26 at 90.26 off lows of 90.20 (both early on and again at 1612BST), breaching initial support (90.22) but leaving key support at late May lows (90.11) untested. Bears remain in technical control.

EUROPEAN INFLATION: Analysts See Limited Risks To August EZ HICP Consensus

Comments after Friday's national-level August HICP data suggest analyst consensus for headline Y/Y stands somewhere between 2.0% and 2.1% (2.1% prior to national-level data) for tomorrow's EZ-wide release. Key highlights below:

- Barclays: "we track EA flash headline HICP inflation at 0.19% m/m NSA and 2.08% y/y (Barclays initial forecast 2.05% y/y) [...] EA flash core HICP inflation at 0.31% m/m NSA and 2.29% y/y (Barclays initial forecast 2.24% y/y)"

- Berenberg: "Overall Eurozone inflation will stick close to the target rate in August again – perhaps ticking up to 2.1% yoy in August [...] We maintain our call that [the ECB] will keep the deposit rate steady at 2%"

- Commerzbank: "The national consumer price figures for August available so far do not indicate any major surprises in the figures for the eurozone due on Tuesday. Inflation remaining close to the ECB's target level is unlikely to prompt the ECB to consider changing its key interest rates, either upwards or downwards."

- Goldman Sachs: "We upgrade our Euro area headline inflation forecast for August to 2.02%yoy, from 2.0%yoy previously, and revise up our Euro area core inflation forecast by 1bp to 2.21%yoy. This would imply seasonally adjusted sequential core inflation of 0.18%mom in August on our estimates"

- Morgan Stanley: "We confirm our forecast for euro area headline HICP inflation at 2.1%Y in August and core HICP at 2.2%Y [...] we stress some downside risks from rounding down, in particular for headline HICP inflation, which, with some variation across remaining countries, could land at 2.0%Y."

- ING: "We think that it is still too early to rule out a September cut [...] the ECB doves have been very silent since the end of the summer break, and it has been the traditional ECB hawks trying to shape the policy debate [...] there is a growing awareness among eurozone policymakers in general that the trade framework agreement between the US and the EU is anything but set in stone [...] a too-hawkish stance could eventually backfire and increase the risk of inflation undershooting"

- JP Morgan: "We expected Euro area core inflation to decline by 0.2%-pt to 2.1%oya. Based on country-level information released today, we now expect Euro area core inflation to be down a tenth to 2.2%oya. [...] We also raise our headline inflation forecast to 2.1%oya (or 0.2%m/m sa)"

FOREX: USD Index Tilts Modestly Lower, GBPJPY Rises 0.4%

- Early price action on Monday saw the USD index fall to a fresh one-month low of 97.54, briefly printing below the post Jackson Hole lows from Sep 22. This continues the theme from late last week where broadly resilient major equity benchmarks have allowed risk sentiment to stabilise, keeping the short-term path of least resistance lower for the US dollar.

- As expected, currency market momentum was lacking, owing to the US Labor Day holiday and the associated dampened liquidity and volumes. This helped the dollar off its worst levels as we approach the APAC crossover.

- Scandinavian FX performed strongly to start the week, clearly outperforming across the G10. USDSEK (-0.67) traded down to a fresh 3-year low of 9.3796 ahead of Thursday’s key inflation data. In similar vein, USDNOK (-0.66%) exhibited similar weakness but remains well shy of the 9.86 lows posted in June.

- Among the majors, GBPUSD rose 0.3% to edge back towards 1.3550. The moves come amid UK Prime Minister Keir Starmer announcing changes to his team to reset his government and give him more influence over economic policy. This helped propel GBPJPY back to 199.50, approaching a key psychological barrier of 200, which has provided pivotal significance over the last year.

- EURUSD had an early leg higher to 1.1736 but remained short of initial resistance at 1.1743 (Sep 22 high). Since then, the pair has edged back to the 1.17 mark as markets await the plethora of US data due this week, which culminates with the US employment report Friday. Key EURUSD resistance and the bull trigger remain at 1.1829, the Jul 1 high. Eurozone inflation data is scheduled tomorrow.

- The Japanese yen bucks the trend very slightly, weaker over the session and USDJPY back at 147.25. Overall, a bear threat in USDJPY remains present and the short-term bear trigger lies at 146.21, the Aug 14 low. US ISM manufacturing PMI data is due Tuesday.

EQUITY TECHS: E-MINI S&P: (U5) Trend Needle Points North

- S&P E-Minis bulls remain in the driver’s seat and the contract traded to a fresh cycle high last week. This maintains the bullish price sequence of higher highs and higher lows. Moving average studies are in a bull-mode position too, highlighting a clear uptrend and positive market sentiment. Attention is on 6543.75, a Fibonacci projection. Support to watch lies at 6332.47, the 50-day EMA. The latest pullback appears corrective.

COMMODITIES: Crude Rallies, Precious Metals Extend Gains

- Crude is trading higher on Monday, with Russian supply concerns and Indian buying in focus. Attention is also turning to the next OPEC+ meeting, scheduled for Sept 7.

- WTI Oct 25 is up by 1.1% at $64.7/bbl.

- Overall, Russian crude exports face pressure, running at a four-week low. However, Indian demand remains firm despite US threats and tariffs.

- From a technical perspective, a bear cycle in WTI futures remains intact and the latest recovery appears corrective.

- Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $66.56, the Aug 4 high.

- Meanwhile, spot gold has risen by 0.8% today to $3,476/oz, amid ongoing questions surrounding Fed independence and focus on the potential for a round of Fed easing.

- Initial US dollar weakness helped the yellow metal rise to a high of $3,490 earlier in the session, before bullion moved away from best levels amid a stabilisation in the greenback.

- The primary trend direction for gold remains up, and sights are on key resistance and the bull trigger at $3,500.1, the Apr 22 all-time high. Clearance of this hurdle would confirm a resumption of the uptrend and open $3,547.9, a Fibonacci projection.

- Elsewhere, silver has outperformed today, with the precious metal up by 2.4% at $40.68/oz.

- Trend signals in silver remain bullish, with sights on $41.064 next, a Fibonacci projection.

| Date | GMT/Local | Impact | Country | Event |

| 02/09/2025 | 0130/1130 | Balance of Payments: Current Account | ||

| 02/09/2025 | 0900/1100 | ** | PPI | |

| 02/09/2025 | 0900/1100 | *** | EZ HICP Flash | |

| 02/09/2025 | 1130/1330 | ECB Elderson and Machado Panel at ECB Legal Conference | ||

| 02/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/09/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 52 Week Bill |