MNI ASIA MARKETS ANALYSIS: Dow Off Record High, Nasdaq Sags

HIGHTLIGHTS

- Treasuries looked to finish mostly weaker Friday, curves twisting steeper with the short end outperforming (2s10s steepened to the highest level since January 2022) as Fed speakers leaned toward less dovish forward guidance.

- KC Fed President Jeff Schmid said Friday he dissented against a quarter-point rate cut this week for the same reasons that he did so in October: inflation remains too high and the labor market is still in balance.

- Despite a sharp move lower for major equity indices late Friday, impact on the DXY has been moderate, and is currently registering a 0.55% decline on the week.

- Tech heavy Nasdaq dragged the DJIA off new record highs (48,886.86) as ongoing AI-valuations concerns weighed heavily on semiconductor makers.

US TSYS

MNI US TSYS: Fed Returns From Blackout, Curves Bear Steepen, 2s10s Near 4Y Highs

- Treasuries look to finish weaker Friday, near lows after rates retreat to Wednesday's pre-FOMC rate cut level (TYH6 -8.5 at 112-06), curves steepened (2s10s +4.932 to 66.436, highest since Jan 2022), and Fed speakers returned from Blackout.

- Federal Reserve Bank of Kansas City President Jeff Schmid said Friday he dissented against a quarter-point rate cut this week for the same reasons that he did so in October: inflation remains too high and the labor market is still in balance.

- Federal Reserve Bank of Cleveland President Beth Hammack on Friday said inflation has been too high, and noted the importance of achieving price stability over the longer term in a way that will support the labor market.

- Chicago Federal Reserve Bank President Austan Goolsbee said Friday he dissented against this week's FOMC decision to lower interest rates by a quarter percentage point because he is seeking more confirmation that inflation is easing.

- Tech heavy Nasdaq dragged the DJIA off new record highs (48,886.86) as ongoing AI-valuations concerns weighed heavily on semiconductor makers.

- Focus turns to next week's November employment report on Tuesday.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.66% (-0.24), volume: $3.299T

- Broad General Collateral Rate (BGCR): 3.62% (-0.25), volume: $1.338T

- Tri-Party General Collateral Rate (TCR): 3.62% (-0.25), volume: $1.304T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (-0.25), volume: $99B

- Daily Overnight Bank Funding Rate: 3.64% (-0.25), volume: $184B

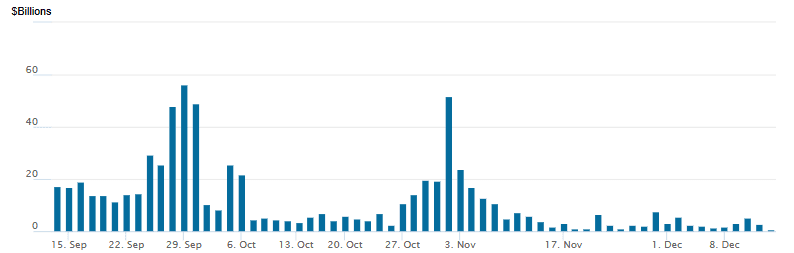

FED Reverse Repo Operation: Nearly Drained

RRP usage retreats to new low: $0.838B (lowest level since mid-March 2021) with 6 counterparties this afternoon from $2.874B Thursday. Compares to prior low on November 18 low: $0.905B; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow segued from downside put structures to calls, fading the curve steepening decline in underlying futures, modest overall volumes. Projected rate cut pricing hold steady to mildly firmer vs. late Thursday levels (*): Jan'26 steady at -6.1bp, Mar'26 at -14bp (-13.2bp), Apr'26 at -20.6bp (-19.6bp), Jun'26 at -33.3bp (-33.3bp).

SOFR Options:

-4,000 SFRH6 96.37/96.50/96.62/96.75 call condors, 3.75

Pit/screen +30,000 SFRH6 96.37/96.50/96.62/96.75 call condors, 3.5

+20,000 SFRH6 96.12 puts, 0.5

+10,000 SFRH6 96.25 puts, 0.75

+10,000 SFRH7 97.25 calls, 19.0 ref 96.835

+5,000 SFRM6 97.00/97.50 call spds, 4.5

6,600 SFRH6 96.37/96.43/96.50 put trees ref 96.455 to -.45

-2,000 SFRG6 96.43/96.56 1x2 call spds, 0.5 vs. 96.455/0.08%

1,250 SFRZ5 96.12/96.18/96.25/96.31 call condors ref 96.29

8,455 SFRF6 96.37/96.43 2x1 put spds, 1.0 ref 96.455

1,000 0QG6 96.43/96.68/96.93/97.06 broken put condors ref 96.835

2,000 SFRG6 96.25/96.37/96.43/96.50 broken put condors, 1.0 ref 96.46

2,000 SFRG6 96.18/96.43/96.56/96.68 broken put condors, 4.0 ref 96.46

Treasury Options:

-2,500 USH6 113/115 2x1 put spds, 20

1,300 FVH6 108 puts ref 109-04.75

-4,000 TYF6 113 calls, 9-10

over 6,900 TYF6 112.75 calls, 17 last

over 5,600 USH6 113 puts, 102 ref 115-04

-2,800 FVH6 109.5/110 call spds, 10.5 ref 109-05.75

MNI BONDS: EGBs-GILTS CASH CLOSE: Curves Twist Steepen Ahead Of Busy Week

Yields picked up Friday, with long-end Gilts underperforming. The German and UK curves both twist steepened on the day.

- Gilts led the way at the short end, following softer-than-expected UK GDP data driving dovish BOE repricing ahead of next week's meeting, with long end yields picking up on concerns that weaker growth could exacerbate fiscal pressures.

- EGBs/Gilts saw some additional modest weakness in the early European afternoon alongside Global FI on a hawkish Bloomberg sources piece on the Bank of Japan.

- Periphery/semi-core EGB spreads widened toward the cash close, mirroring a pullback in equities.

- Otherwise, developments were limited. Final November inflation readings for Germany, France, and Spain brought no significant surprises.

- For the week, the UK curve twist steepened (2Y yield -3.4bp, 10y +4.1bp) with Germany's ending flat (2Y and 10Y both +5.9bp).

- Next week's schedule is packed, with the final BOE and ECB decisions of the year, as well as flash PMIs and UK CPI and labour market reports.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at 2.154%, 5-Yr is up 0.4bps at 2.468%, 10-Yr is up 1.4bps at 2.857%, and 30-Yr is up 2.9bps at 3.481%.

- UK: The 2-Yr yield is down 2.4bps at 3.747%, 5-Yr is down 0.4bps at 3.955%, 10-Yr is up 3.3bps at 4.517%, and 30-Yr is up 6.1bps at 5.268%.

- Italian BTP spread up 0.7bps at 69.1bps / French OAT up 1.1bps at 72.4bps

MNI OPTIONS: Call Spreads Favoured In Euribor, Puts In Bunds

Friday's Europe rates/bond options flow included:

- DUG6 106.70/106.80/106.90/107.00c condor, bought for 3 in 4k.

- DUH6 106.80/107.00/107.20c fly, bought for 3.5 in 5k

- RXG6 126.50/124.50 put spread paper paid 30 vs. 127.48/49 on 6K

- RXG6 119p, bought for 1 and 1.25 in 5k.

- ERH6/J6 97.87p calendar spread, sold the April at 1.5 in 5.5k

- ERU6 98.06/98.25 call spread & 98.12/98.50 call spread vs. 97.895 (30% delta) paper paid 7.0 on 4K

- ERZ6 97.87/98.25 1x1.5 call spread vs. 97.50 puts vs. 97.84 (40% delta) paper paid 1.0 on 4K

MNI FOREX: Moderate USD Boost Friday, DXY Broadly Consolidates Weekly Decline

- Having held resistance well across November, the USD’s turn lower gathered downside momentum this week, assisted by a not so hawkish cut from the Fed. This prompted the USD index to briefly extend its three-week pullback to ~2.25% on Thursday, before a partial reprieve across Friday’s session.

- Despite a sharp move lower for major equity indices late Friday, impact on the DXY has been moderate, and is currently registering a 0.55% decline on the week. The late selloff has weighed on the likes of AUD (-0.39%) and NZD (-0.28%), while GBP has suffered following the weaker-than-expected October GDP, bolstering the likelihood of a BOE cut next week.

- The worst performing currencies are both the NOK and SEK today, with limited newsflow to explain the moves. Some may point to a potentially delayed reaction to waning oil prices across the week as contributing to the 0.75% move higher for EURNOK, which has risen to the highest level since late August.

- USDCAD weakness has been one of the most notable developments in G10 FX over the last week, with spot extending lower following an impressive technical breakdown. Friday’s Canadian dollar relative resilience emphasises this narrative and downside targets for USDCAD include 1.3682, the 76.4% retracement of the Jun 16 - Nov 6 bull cycle and 1.3637, the Jul 25 low.

- Tier-one data from the US returns next week, with employment and inflation data headlining. Rate decisions from the BOE, ECB, BOJ, Riksbank and Norges are all scheduled.

MNI FX OPTIONS: Expiries for Dec15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E2.3bln), $1.1650(E1.2bln), $1.1680(E1.1bln), $1.1700(E1.7bln)

- USD/JPY: Y156.00($788mln), Y156.50($1.2bln)

- GBP/USD: $1.3400(Gbp543mln)

- AUD/USD: $0.6630-50(A$1.5bln)

- AUD/NZD: N$1.1450(A$754mln)

- USD/CAD: C$1.4000-20($1.1bln)

MNI US STOCKS: Late Equities Roundup: Tech Stocks Lead Declines

- Stocks remain weaker late Friday amid ongoing AI-valuations concern, the tech-heavy Nasdaq pulling the DJIA off new record highs in early trade (48,886.86). Currently, the DJIA trades down 206.77 points (-0.42%) at 48495.36, S&P E-Mini Futures down 71 points (-1.03%) at 6836, Nasdaq down 349.9 points (-1.5%) at 23242.06.

- Selling accelerated after Oracle headlines reported OpenAI data center buildout delay from 2027 to 2028 saw the tech company fall over 6%. Oracle pared losses to -4.5% after denying the report, adding there were "no delays to contractual commitments" for OpenAI.

- While Oracle grabbed midmorning headlines, shares of Sandisk Corp and Broadcom led tech-sector decline since the open: Sandisk Corp -13.98%, Broadcom -11.48%. Other laggers included: Corning -7.58%, Arista Networks-7.21%, Seagate Technology -6.76%, Qnity Electronics -6.52% and Amphenol Corp -6.45%.

- Industrials and Energy sector shares also underperformed in late trade:

- Quanta Services -5.53%, Eaton Corp -4.42%, Generac Holdings -3.97%, GE Vernova -3.72% and EMCOR Group -3.23%.

- Texas Pacific Land -4.95%, Valero Energy -2.77%, SLB Ltd -2.50%, Halliburton -2.30% and Williams Cos -1.75%.

- On the positive side, Consumer Staples and Materials sector shares outperformed:

- Hormel Foods +1.60%, Coca-Cola +1.50%, Monster Beverage +1.49% and McCormick & Co +1.35%.

- Mosaic Co +3.53%, Linde PLC +3.34%, Ball Corp +2.80% and Avery Dennison +0.73%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Corrective Pullback

- RES 4: 7000.00 Psychological round number

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6918.50 High Oct 31

- RES 1: 6908.00 High Dec 10

- PRICE: 6831.50 @ 1448 ET Dec 12

- SUP 1: 6805.00 Intra-day low

- SUP 2: 6767.95 50-day EMA

- SUP 3: 6674.50 Low Nov 25

- SUP 4: 6525.00 Low Nov 21 and a key support

A bull cycle in S&P E-Minis remains intact and a fresh short-term cycle high yesterday strengthens the bull theme. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. Sights are on the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support to watch is at 6823.86, the 20-day EMA.

COMMODITIES

MNI OIL: US OIL: December 12 - Americas End of Day Oil Summary: Crude Steady

WTI Crude prices ended slightly lower and on track for a net decline on the week with focus on geopolitical risks, including Russia-Ukraine peace talks, and oversupply concerns. US equity markets have sold off due to weakness in tech companies though it hasn’t impacted energy markets thus far

- Baker Hughes reports US oil rig count rose by 1 to 414.

- Zelenskiy floated the prospect of putting the issue of territorial control of the Donbas to a referendum amid pressure to end the war. Nevertheless, Zelenskiy has publicly maintained his position that Ukraine won’t consider surrendering territory to the Kremlin.

- Brazilian oil output is coming back online from issues that took out over 300kb/d last month, increasing the probability of an oversupply in 2026.

- Recent attacks by Ukraine on one of the primary export terminals for Kazakh oil has limited output by an estimated 270kb/d since Nov. 29.

- Russia increased oil production in November m/m and is gradually achieving OPEC+ quotas, Deputy PM Alexander Novak said on Friday to Tass.

- The seizure of the Venezuelan oil tanker by US military could put up to 30% of Venezuela's oil exports at risk, according to Rapidan cited by Bloomberg.

- WTI Jan futures were down 0.3% at $57.44

- WTI Feb futures were down 0.4% at $57.23

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 15/12/2025 | 1000/0500 | * | CREA Existing Home Sales | |

| 15/12/2025 | 1000/1100 | ** | EZ Industrial Production | |

| 15/12/2025 | 1315/0815 | ** | CMHC Housing Starts | |

| 15/12/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 15/12/2025 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 15/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 15/12/2025 | 1330/0830 | *** | CPI | |

| 15/12/2025 | 1430/0930 | Fed Governor Stephen Miran | ||

| 15/12/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 15/12/2025 | 1530/1030 | New York Fed's John Williams | ||

| 15/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/12/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 16/12/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI |