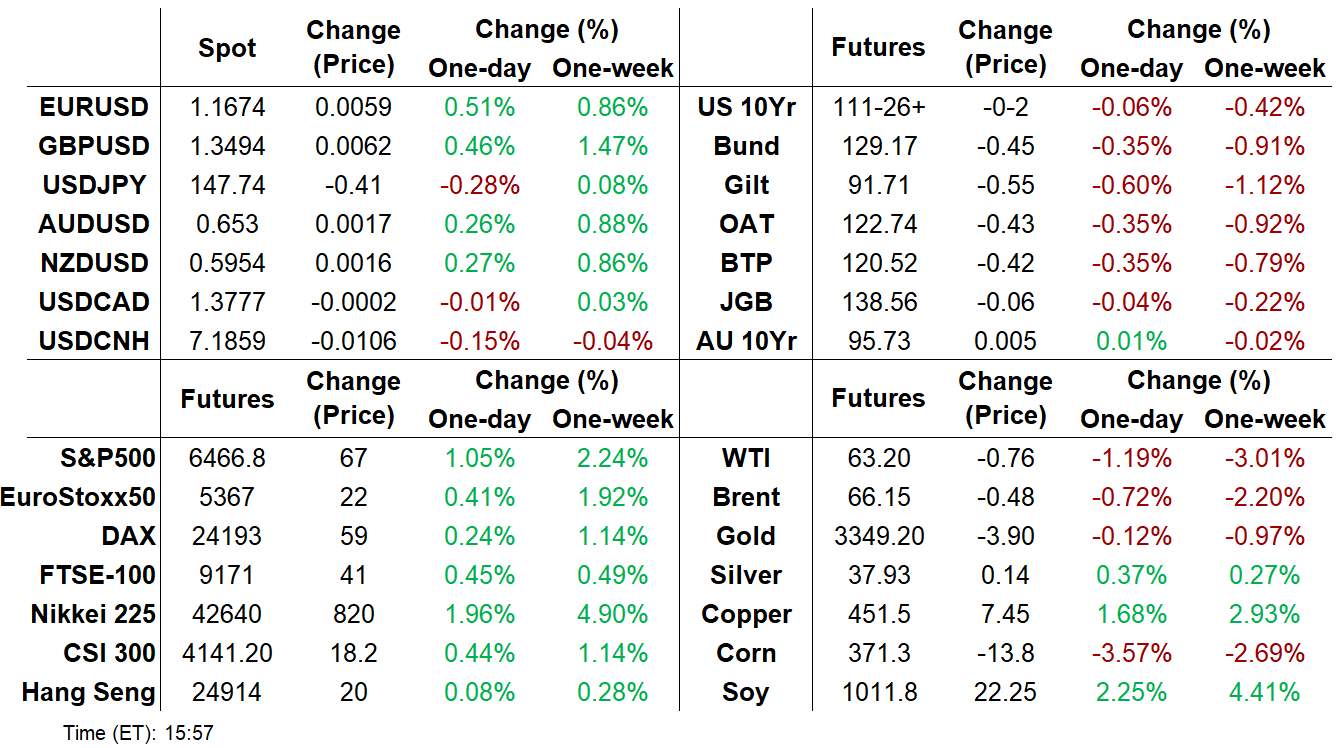

MNI ASIA MARKETS ANALYSIS: CPI Keeps Door Open To Fed Cuts

MNI (NEW YORK) -

HIGHLIGHTS:

- Softer-Than-Expected Core Goods CPI Data Opens Door Wider For September Fed Cut

- Treasury Curve Twist Steepens, With Global Long-End FI Under Pressure

- US Equity Indices Hit All-Time Highs, Dollar Retraces

US TSYS: Lack Of Core Goods CPI Acceleration Triggers Twist Steepening

The Treasury curve twist steepened Tuesday as the key details of the July CPI report came in softer than widely expected.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer. (MNI's Inflation Insight has more details, PDF here).

- The short-end saw a post-CPI rally, buoyed by deepening Fed cut expectations: a 25bp reduction in September is now 94% priced (up from about 88% Monday), with 60bp of cuts through end-2025 (up from 57bp Monday).

- This wasn't greatly dampened by Fed hawks Barkin and Schmid who expressed no urgency to cut rates in the near future.

- The long end, conversely, sold off after an initial rally. German Bunds appeared to lead the retracement, amid heavy volumes there albeit with little obvious catalyst. However some of the sell-off came after President Trump said on social media that he was considering a "major lawsuit" against Fed Chair Powell over Federal Reserve building renovation cost overruns.

- Latest cash levels: the 2-Yr yield is down 3.8bps at 3.7308%, 5-Yr is down 1.6bps at 3.8207%, 10-Yr is up 0.2bps at 4.2868%, and 30-Yr is up 2.1bps at 4.8736%. Sep 10-Yr futures (TY) down 2/32 at 111-26.5 (L: 111-19.5 / H: 112-06)

- Wednesday's data calendar is lighter (ahead of PPI and retail sales later in the week), with weekly MBA mortgage data in the morning, though we hear from a few FOMC participants including Barkin, Goolsbee, and Bostic.

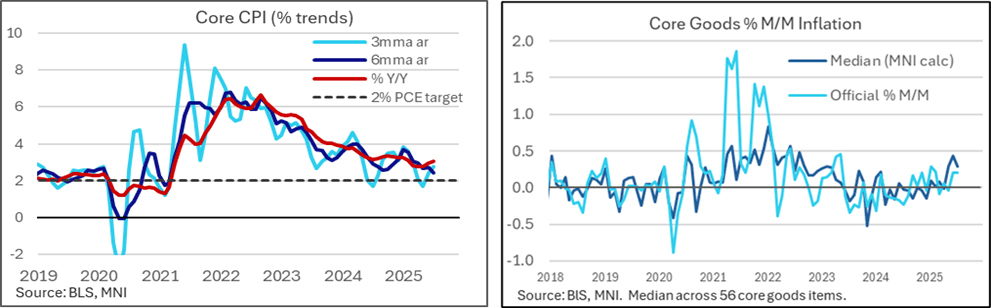

MNI US Inflation Insight: Core Goods Spike Fails To Emerge

The July CPI report saw further acceleration in monthly core inflation but it was driven by the volatile supercore category. Instead, core goods inflation, an area of focus for tariff passthrough clues, was surprisingly soft. This category only maintained the still-solid monthly clip seen in June, whilst median core goods inflation moderated after a strong increase in June.

- Core CPI inflation was exactly in line with the median unrounded analyst estimate we had seen for July at 0.32% M/M, accelerating from 0.23% in June and 0.13% in May for its strongest month since January.

- The breakdown relative to expectation was dovish however, as core goods underwhelmed (0.21% M/M vs average expectations closer to 0.4%) in a month that was expected to show increasing signs of tariff passthrough ahead of perhaps the largest monthly increases in the fall months. It follows a very similar 0.20% M/M in Jun after a weak -0.04% M/M in May.

- The offsetting factor was core services (0.36% M/M vs average expectations around 0.30%), driven by the volatile “supercore” category at 0.48% M/M whilst rental inflation was exactly as expected.

- Airfares played a large role here and as always won’t feed into PCE. Some notable PCE inputs meanwhile saw partly offsetting large moves from booming dental services and further declines in lodging.

- The report saw a firming up of 25bp cut expectations for the next FOMC decision on Sept 17, with 24bp priced vs 21bp prior, and 61bp of cuts to year-end. The path nears dovish extremes seen after the surprisingly weak July nonfarm payrolls report on Aug 1.

- Eyes will firmly be on Powell at Jackson Hole next week but we still get Aug NFP/CPI data before Sept 17.

- Ahead of Thursday’s PPI release, core PCE tracking looks to be around 0.25% M/M after 0.26% in June.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

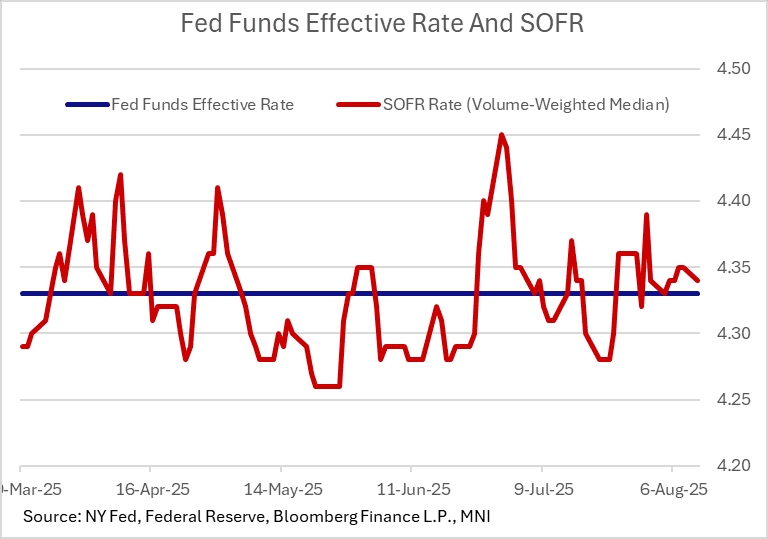

US TSYS/OVERNIGHT REPO: SOFR Softens Slightly, Potential Pickup Ahead

Secured rates were a little softer Monday as was broadly expected, with SOFR edging 1bp lower to 4.34%. Other major secured rates and effective Fed funds were unchanged.

- As we noted yesterday, pressure could pick up later in the week on Treasury auction settlements. These include $55B in net cash raised by bills today, and a further $42B on Thursday, followed by $35B in coupon settlements Friday.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.34%, -0.01%, $2796B

* Broad General Collateral Rate (BGCR): 4.33%, no change, $1173B

* Tri-Party General Collateral Rate (TGCR): 4.33%, no change, $1137B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $115B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $263B

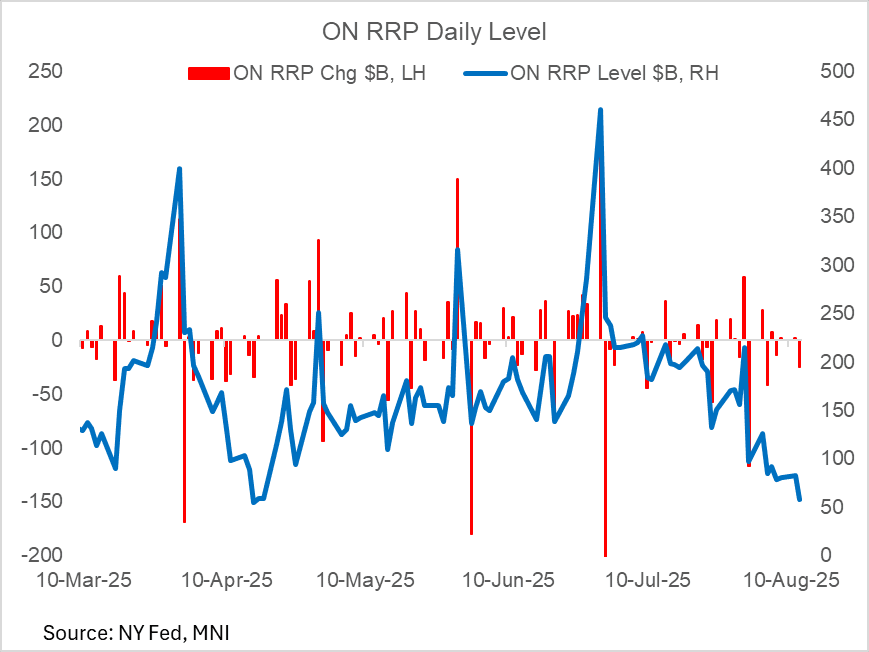

US TSYS/OVERNIGHT REPO: ON RRP Takeup At 4-Month Low

Takeup of the Fed's overnight reverse repo facility Tuesday fell to its lowest since April 16th (which was depressed by a major tax payment deadline).

- At $57.5B, down $24.7B from Monday, this is the 7th session in the last 8 that it's been below $100B. It hasn't so consistently been below that level since February.

- It comes amid continued buildup of the Treasury General Account amid bill sales, which appear to be diverting funds away from RRP.

- At least one analyst (Citi) sees ON RRP takeup dropping to near-zero by month-end.

OPTIONS: US Options Roundup - Aug 12 2025

Tuesday's US rates/bond options flow included:

- SFRQ5 95.87/95.81ps, traded for 1.75 in 2k.

- SFRQ5 95.81/95.75ps 1x2, traded half in 4k.

- SFRU5 96.12/96.25cs, traded 1.5 in 5k.

- SFRU5 96.00/96.12/96.25c fly, traded for half in 2k.

- SFRU5 95.87/95.81/95.75p ladder, traded half in 3k.

- SFRU5 95.8125 put, bought for 3.75 in 12.5k

- SFRU5 95.75/95.68ps 1x3, traded 0.75 in 2k.

- SFRU5 96.125/96.25 call spread bought for 1.375 in 45k

SFRU5 95.75/95.62ps, traded 1.75 in 2k. - SFRU5 96.12c, bought for 2 in 4k

- SFRZ5 96.25/96.37/96.50/96.62c condor, bought for 3.5 in 5k.

- SFRM6 96.50p, bought for 21.5 in ~5k.

- SFRV5 96.1875/96.4375 call spread sold at 10s in 45.5k (block)

- 0QZ5 98.00c, bought for 2 in 11k

- TYX5 110.5 puts sold at 34 in ~9.8k (block)

EGBs-GILTS CASH CLOSE: Bear Steepening, With Gilts Underperforming

European curves bear steepened Tuesday.

- US CPI data in early afternoon was the session's global focus, and initially brought a positive reaction in core FI as it appeared to allay fears of upside pressure on goods prices from inflation.

- However the move swiftly reversed, with Bunds leading a global selloff. There was no identifiable trigger for the long-end German sell-off, which saw 30Y yields hit the highest since 2011 amid heavy volumes in futures. 10Y German yields stopped just shy of the July high of 2.769% (hitting 2.758%).

- There was some extension of the selloff in sympathy with long-end Treasuries as President Trump said on social media that he was considering allowing a "major lawsuit" against Fed Chair Powell to proceed.

- That said, Gilts underperformed Bunds on the day. The August UK labour market release was on balance stronger-than-expected, bringing a mildly hawkish market reaction, though private sector regular pay data remains consistent with slowing wage growth. Our review of the data is here.

- Both the German and UK curves bear steepened, with periphery/semi-core EGB spreads closing mixed.

- Wednesday's calendar is lighter, with final Spanish and German CPI readings on offer.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.3bps at 1.967%, 5-Yr is up 2.9bps at 2.318%, 10-Yr is up 4.8bps at 2.744%, and 30-Yr is up 7.3bps at 3.299%.

- UK: The 2-Yr yield is up 2.2bps at 3.885%, 5-Yr is up 3.9bps at 4.04%, 10-Yr is up 6.1bps at 4.626%, and 30-Yr is up 7.5bps at 5.467%.

- Italian BTP spread down 0.1bps at 78.8bps / French OAT up 0.5bps at 66.8bps

EUROPE OPTIONS: Buying Of Call Spreads In UK Rates, Put Structures In Bund

Tuesday's Europe rates/bond options flow included:

- RXV5 127/125ps, bought for 27.5 in 1k.

- RXV5 126.50/125.50/125.00 broken put ladder, bought for 4 in 1k.

- SFIU5 96.10/96.25cs, bought for 1 in 1.5k.

- SFIM6 96.90/97.10cs vs 96.00/95.85ps, bought the cs for 1.25 in 5k.

FOREX: USD Slides as CPI Clears Way for Sept Fed Cut

- The USD slid against all others Tuesday as the July CPI print cleared the path for the Fed to resume rate cuts from the September meeting. Core goods inflation undershot expectations for a further acceleration in M/M terms, and while still a solid monthly clip compared to 2024 levels, there few sufficient signs of tariff-led inflation that could derail easing both in September, as well as further rate cuts before year-end.

- The resultant USD Index weakness pushed the price back below the 50-dma, testing last week's lows in the process. Medium-term, this clears markets for a test of the late July pullback lows of 97.109 - a level that should see firm support.

- EUR was the primary beneficiary of the USD pullback, and EUR/JPY extended gains above 172.50 for the first time since July - keeping momentum pointed higher and tilting focus toward the YTD highs of 173.97. In addition, GBP/USD saw support, with the CPI reaction prompting a new weekly high and a test at the 50-dma of 1.3502. Clearance above this level would further reverse the downleg off the late July high and put markets near 3% off the early August low.

- Despite the post-RBA weakness, AUDUSD is yet to challenge any meaningful support. The pair rallied well off the week's lowest levels last week on broad USD weakness - erasing any signs of a bearish breakout on the show through the 20- and 50-day EMAs. While support at 0.6455 the Jul 17 low, has been cleared, the recovery in prices keeps key resistance in focus at 0.6625 the Jul 24 high.

- Focus Wednesday shifts to Japanese PPI data, German final CPI and appearances from Fed's Barkin and Schmid.

FX OPTIONS: Expiries for Aug13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-20(E3.2bln), $1.1570-80(E1.1bln), $1.1600(E851mln), $1.1650(E693mln), $1.1700(E1.3bln)

- USD/JPY: Y146.75-85($1.4bln), Y147.00($1.1bln), Y147.40-50($515mln) Y150.25($1.5bln);

- AUD/USD: $0.6550(A$597mln), $0.6575(A$646mln)

- USD/CAD: C$1.3725($555mln), C$1.3835-55($724mln)

EQUITIES: All-Time High In S&P As CPI Keeps Door Open To Fed Cuts

The S&P 500 and Nasdaq were set for an all-time high close Tuesday with gains of around 1%. The catalyst for the move was a July CPI report that kept the door wide open to the Fed resuming rate cuts in September.

- All main S&P 500 sectors were flat/higher, with communications (+1.8%) and info tech (+1.3%) leading the way.

- Airlines (Delta and United up 9-10%) gained after airfare CPI was shown up an unexpectedly high 4+% M/M, with semiconductor firms also performing well as markets digested a report by The Information that Chinese regulators ordered tech companies to suspend Nvidia chip imports.

- Latest levels: Dow Jones mini up 436 pts or +0.99% at 44529, S&P 500 mini up 62.75 pts or +0.98% at 6452.5, NASDAQ mini up 283.25 pts or +1.2% at 23864.75.

COMMODITIES: WTI Falls, Gold Steady, Copper Bounces

- WTI has lost ground during US hours to be on track for its lowest close since early June. The EIA’s short-term energy outlook showed an upward revision in the expected supply surplus for 2025.

- The EIA now sees a supply surplus of 1.7m b/d this year, compared to a previous forecast for a 1.1m b/d surplus.

- WTI Sep 25 is down by 1.2% at $63.2/bbl.

- WTI futures remain below the 50-day EMA at $65.15, which keeps short-term momentum pointed lower. The clear break exposes $58.17, the May 30 low.

- Meanwhile, spot gold has edged up by 0.2% to $3,349/oz, with the yellow metal trading in a narrow range as US CPI data came in broadly in line with expectations.

- For now, a bull cycle in gold that started Jun 30 remains intact. Key near-term resistance is $3,439.0, the Jul 23 high.

- However, the yellow metal has previously traded through support at $3,334.0, the 50-day EMA. A clear break of this level would signal scope for a deeper retracement and expose the next key support at $3,248.7, the Jun 30 low.

- Elsewhere, copper has bounced by 1.9% to $452/lb, bringing the red metal to its highest level since July 31.

- However, copper remains well below the Jul 30 high, which cancels the recent bullish theme and instead highlights a bearish threat.

- A continuation lower would signal scope for a test of key support at $411.75, the Apr 7 low. Initial resistance to watch is at $497.25, the Jul 8 low.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 13/08/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 13/08/2025 | 0700/0900 | *** | HICP (f) | |

| 13/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 13/08/2025 | - | *** | Money Supply | |

| 13/08/2025 | - | *** | New Loans | |

| 13/08/2025 | - | *** | Social Financing | |

| 13/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 13/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 13/08/2025 | 1700/1300 | Chicago Fed's Austan Goolsbee | ||

| 13/08/2025 | 1730/1330 | Atlanta Fed's Raphael Bostic | ||

| 14/08/2025 | - | NorgesBank Meeting | ||

| 14/08/2025 | 0130/1130 | *** | Labor Force Survey |