MNI US Inflation Insight: Core Goods Spike Fails To Emerge

Aug-12 17:57By: Tim Cooper and 1 more...

Inflation+ 1

Download Full Report Here

Executive Summary

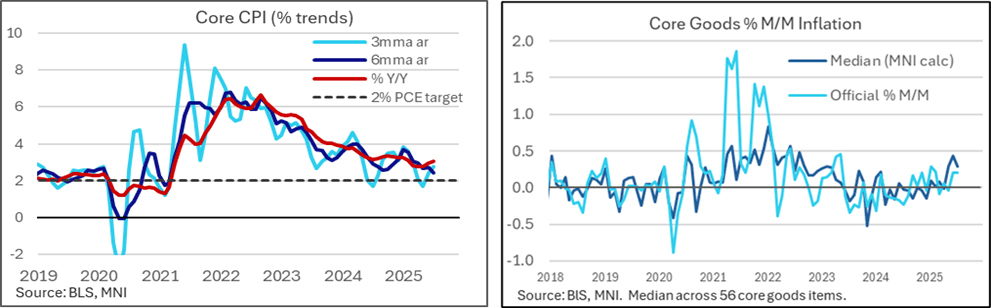

The July CPI report saw further acceleration in monthly core inflation but it was driven by the volatile supercore category. Instead, core goods inflation, an area of focus for tariff passthrough clues, was surprisingly soft. This category only maintained the still-solid monthly clip seen in June, whilst median core goods inflation moderated after a strong increase in June.

- Core CPI inflation was exactly in line with the median unrounded analyst estimate we had seen for July at 0.32% M/M, accelerating from 0.23% in June and 0.13% in May for its strongest month since January.

- The breakdown relative to expectation was dovish however, as core goods underwhelmed (0.21% M/M vs average expectations closer to 0.4%) in a month that was expected to show increasing signs of tariff passthrough ahead of perhaps the largest monthly increases in the fall months. It follows a very similar 0.20% M/M in Jun after a weak -0.04% M/M in May.

- The offsetting factor was core services (0.36% M/M vs average expectations around 0.30%), driven by the volatile “supercore” category at 0.48% M/M whilst rental inflation was exactly as expected.

- Airfares played a large role here and as always won’t feed into PCE. Some notable PCE inputs meanwhile saw partly offsetting large moves from booming dental services and further declines in lodging.

- The report saw a firming up of 25bp cut expectations for the next FOMC decision on Sept 17, with 24bp priced vs 21bp prior, and 61bp of cuts to year-end. The path nears dovish extremes seen after the surprisingly weak July nonfarm payrolls report on Aug 1.

- Eyes will firmly be on Powell at Jackson Hole next week but we still get Aug NFP/CPI data before Sept 17.

- Ahead of Thursday’s PPI release, core PCE tracking looks to be around 0.25% M/M after 0.26% in June.