MNI ASIA MARKETS ANALYSIS: Coupon Size Increase Contemplated

HIGHLIGHTS

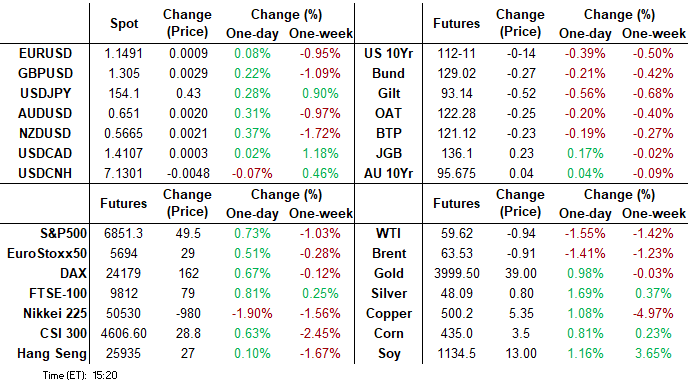

- Treasuries look to finish broadly lower following mildly better than expected ADP jobs gain and the Tsy contemplating coupon size increase and no discussion of ramping up bills.

- Conservative Supreme Court justices Amy Coney Barrett, Neil Gorsuch, and Chief Justice John Roberts all appeared sceptical of President Donald Trump’s reciprocal tariffs.

- USD index is holding at unchanged levels on the day, as a recovery for major equity indices today offsets the most recent greenback enthusiasm.

- Information Technology sector shares led gainers on the day, rebounding after opinions of the tech sector tied to AI has been overbought dissipated.

US TSYS

US TSYS: ADP Payrolls Growth Stabilized, Tsy Contemplates Coupon Size Inc

- Tsys initially retreated after larger than expected ADP jobs gain - then extended lows after in-line refunding annc - while coupon sizes expected to remain stable for "at least the next several quarters" - Tsy contemplating coupon size increase and no discussion of ramping up bills in lieu adding to bear curve steepening.

- Tsys tracked German Bunds lower with no obvious headline of Block driver, unlikely that comment from Fed Miran adding to the decline: "DATA SUGGEST RATES CAN BE A LITTLE LOWER THAN THEY ARE" while "KEEPING POLICY THAT RESTRICTIVE RUNS UNNECESSARY RISKS," Bbg.

- Currently, the Dec'25 10Y contract trades -15 at 112-10 vs. 112-09.5 low, nearing the reversal trigger at 112-06. The weakness was triggered by the clean break below the 50-day EMA, currently at 112-26+, and highlights potential for a deeper retracement near-term. 10Y yield +.0720 at 4.1571%. Curves bear steepen: 2s10s +1.637 at 52.366, 5s30s +.412 at 97.121.

- Conservative Supreme Court justices Amy Coney Barrett, Neil Gorsuch, and Chief Justice John Roberts all appeared sceptical of President Donald Trump’s reciprocal tariffs, during questions to Trump’s lawyer during today’s hearing. The implied probability of Trump winning the case has dropped to 20%, per Polymarket.

- Due to the ongoing, weekly Jobless Claims, Non-Farm Productivity / Unit Labor Costs and Wholesale Inventories / Sales has been suspended. That leaves: Challenger Job Cuts (0730ET), Revelio Public Labor Statistics and Chicago Fed Labor Market Indicator (both 0830ET).

- Myriad Fed speakers on tap tomorrow: NY Fed Williams lecture at Goethe Univ. Frankfurt (1100ET), Fed Gov Barr moderated discussion community development (1100ET), Cleveland Fed Hammack Economic Club of NY (1200ET), Fed Gov Waller CB & Payments panel (1530ET), Philly Fed Paulson Consumer Finance Inst (1630ET), StL Fed Musalem fireside chat on policy (1730ET).

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.00% (-0.13), volume: $3.147T

- Broad General Collateral Rate (BGCR): 3.98% (-0.11), volume: $1.183T

- Tri-Party General Collateral Rate (TCR): 3.98% (-0.11), volume: $1.156T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.87% (+0.00), volume: $94B

- Daily Overnight Bank Funding Rate: 3.87% (+0.00), volume: $165B

FED Reverse Repo Operation

RRP usage slips to $12.700B with 12 counterparties this afternoon - from $16.893B Tuesday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Chunky SOFR/Treasury option flow remained mixed Wednesday, SOFR seeing better low delta call interest fading the underlying decline, Treasury options saw decent two-way trade in 10Y puts. After a firmer open, underlying futures retreated after extended lows after in-line refunding annc - Tsy contemplating coupon size increase and no discussion of ramping up bills in lieu adding to bear curve steepening. Rates held weaker as SCOTUS appeared skeptical over tariff defense. Projected rate cut pricing gains slightly vs. late Tuesday levels (*): Dec'25 at -17.8bp (-17.2bp), Jan'26 at -26.9bp (-26.4bp), Mar'26 at -35.4bp (-34.9bp), Apr'26 at -41.5bp (-41.4bp).

SOFR Options:

+25,000 SFRH6 96.62/96.81 call spds, 2.75 ref 96.395

+10,000 SFRF6 96.25/96.37/96.50/96.62 call condors, 4.25 ref 96.395

+4,000 SFRH6 96.37/96.62 call spds, 4.75 over 96.12 puts

-5,000 0QM6/2QM6 97.00/97.50 call spd spd, 3.0

+5,000 SFRF6 96.31/96.37/96.50 broken put trees, 0.25

+2,000 3QM6 96.87/97.00 call strip

+4,500 SFRZ5 96.37/96.50/96.62/96.68 broken call condors, 1.0

1,600 SFRZ5 96.31/96.43 call spds vs. SFRG5 96.37/96.50 call spds, 2.5 net

-12,000 SFRX5 96.18/96.25/96.31 put trees, 3.25 ref 96.255

+2,200 0QX5 96.37 calls, 5.0

+3,000 SFRH6 96.50/96.62 call spds vs. 96.12/96.25 put spds, 0.5 net

Block, 3,000 0QZ5 97.37 calls, 2.0 vs. 96.935/0.10%

2,000 SFRZ5 96.18/96.25/96.37 broken call trees ref 96.26

2,300 SFRZ5 96.31/96.37 call spds ref 96.26

2,400 SFRZ5 96.18/96.25 put spds ref 96.265

7,500 SFRX5 96.25 straddles, 6.0

Treasury Options:

4,000 TYF6 112/112.5 strangles, 120 ref 112-08.5

2,000 USF6 115/116/117 put flys

3,200 TYZ5 113.5 straddles 117

Block, -13,800 TYZ5 112.5 straddles, 52 ref 112-19.5

+47,000 TYZ5 112 puts, 11 last, total volume over 57.2k

-25,000 TYZ5 112.5 puts, 22 last at 27

+18,000 TUZ5 104/104.125/104.5/104.75 iron condor vs 4,500 104.25 straddles, 2 net/condor over

over 11,900 TYZ5 113 calls, 25 ref 112-28 to -26

+/-8,000 FVZ5 109.25 calls, 19-20 vs. 109-08.25/0.53%

over 11,900 TYZ5 113 calls, 25 ref 112-28 to -26

+5,000 TYZ5 113 calls, 19 vs. 112-21.5/0.42%

3,800 TUZ 103.87 puts ref 104-06.38 to -08.25

+5,000 TUF6 103.75/104/104.12/104.25 put condors, 0.5 ref 104-11.88

+5,000 TYZ5 112 puts, 7

+5,000 TYZ5 111.5/112.25 put spds, 8 ref 112-30

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Ahead Of BOE

European yields rose Wednesday. with Gilts underperforming.

- Core EGBs and Gilts traded flat in the European morning, with some downward bias as Services PMIs were revised up from flash in the final for the UK, France and Germany (with Italy and Spain coming in above-expected) and anticipation grew of a nearer-term resolution to the US federal government shutdown.

- Yields rose through the afternoon led by US Treasuries, following stronger than expected US data (ISM Services, ADP private payrolls).

- In other data, the ECB's latest forward-looking wage tracker was revised up marginally, while German September factory orders were a little stronger than expected.

- On the day both the German and UK curves bear steepened, with Gilts underperforming ahead of Thursday's BOE decision announcement.

- Periphery/semi-core EGB spreads widened slightly.

- The BOE is Thursday's market focus. MNI's preview is here - we characterise our view as 50/50 (when it comes to a cut or a hold), which is comfortably more dovish than current market pricing.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at 2.004%, 5-Yr is up 1.5bps at 2.27%, 10-Yr is up 1.9bps at 2.673%, and 30-Yr is up 2.2bps at 3.259%.

- UK: The 2-Yr yield is up 2bps at 3.804%, 5-Yr is up 3.1bps at 3.93%, 10-Yr is up 3.8bps at 4.463%, and 30-Yr is up 4.5bps at 5.249%.

- Italian BTP spread up 0.5bps at 75.1bps / French OAT up 0.3bps at 78.5bps

MNI OPTIONS: Extremely Busy Session Includes Large Outright Euribor Call Trades

Wednesday's Europe rates/bond options flow included:

- RXZ5 130.00/130.50cs, bought for 10 in 4.2k

- RXZ5 129/128.5/128p ladder vs 131c, bought the ladder for 5 in 3k

- RXG6 128.50/127.50ps vs 131.00/132.00cs, bought the ps for 2 in 1.5k

- ERH6 98.06/98.18/98.31c fly, bought for 1.5 in 10k

- ERH6 98.06/98.18cs, bought for 2.5 in 10k

- ERH6 98.1875 call, sold for 2 in 8k

- ERU6 98.50c, bought for 3.25 in 17.5k total

- SFIZ5 96.30/96.15/96.05 broken put fly paper paid 6 on 8K

- SFIG6 96.55/96.65/96.75 call fly paper paid 1.5 on 7.5K

- SFIH6 96.45/96.55/96.65/96.75c condor vs 96.25p, bought the condor for 0.25 in 2k

- SFIJ6 96.25/96.15 put spread 6K given at 1

- 0NU6 96.80/97.10cs vs 0NU6 96.30/96.00ps, bought the cs for -0.25 and flat in 7.5k

MNI FOREX: USDJPY Bounce Affirms Pullbacks are Technically Corrective

- Despite the impressive surge higher for US yields on Wednesday, the USD index is holding at unchanged levels on the day, as a recovery for major equity indices today offsets the most recent greenback enthusiasm. Despite this, the DXY did make fresh 5-month highs, with a firmer-than-expected ISM services PMI supportive.

- Most of the G10 currency action has been centered around the Yen once more, with USDJPY posting an impressive 140 pip range on Wednesday. Initial risk off during SPAC hours and a moderately hawkish set of BOJ minutes prompted USDJPY to extend its pullback to 152.96, however, the subsequent recovery has been very notable.

- The pair’s intraday bounce picked up pace in late European trade, printing a new daily high through the London close. A break above yesterday's 154.48 would mark a full reversal of the JPY strength tripped by Katayama's warnings on FX movements on Tuesday - and again shows that USDJPY is a key beneficiary in a higher US yields environment.

- Today's price action affirms the view that pullbacks are technically corrective in nature, and a break of 154.39/48 supports a rally toward 154.80, the Feb 12th high.

- The more stable risk sentiment has allowed AUD and NZD to outperform, rising around 0.3% against the greenback, although these advances are yet to erode the prior declines this week.

- USDCAD remains a touch higher on the day above 1.41, looking to extend its winning streak to five sessions. Importantly, the pair has held an important resistance for now, the top of the bull channel drawn from the Jul 23 low.

- Higher equities boosted EM FX significantly, with the likes of MXN, ZAR and BRL shrugging off the moves for US yields. USDMXN has now reversed over 1% from intra-day highs, helping the pair edge back below 18.60 in late trade.

- The Bank of England headlines the economic calendar on Thursday, and is potentially set to be a close call decision between a hold and a 25bp cut.

MNI OPTIONS: Expiries for Nov6 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E1.5bln), $1.1450(E560mln), $1.1500(E1.6bln), $1.1525(E604mln), $1.1550(E1.8bln), $1.1600(E1.6bln), $1.1715(E1.5bln)

- GBP/USD: $1.2900(Gbp2.0bln), $1.3100(Gbp1.0bln), $1.3350(Gbp770mln)

- USD/JPY: Y152.00($1.0bln), Y153.00-05($1.2bln), Y154.00-05($1.1bln), Y154.50-55($1.1bln), Y155.00($1.9bln), Y155.35($1.2bln)

- EUR/GBP: Gbp0.8800-10(E1.1bln)EUR/JPY: Y177.00-05(E561mln)

- AUD/USD: $0.6480-90(A$650mln)

MNI US STOCKS: Late Equities Roundup: Overbought Tech Sector Concerns Cool

- Stocks have recovered from the prior session's sell-off Wednesday, back to or near late Monday levels. Currently, the DJIA trades up 258.93 points (0.55%) at 47342.77, S&P E-Minis up 48.25 points (0.71%) at 6850.75, Nasdaq up 264.4 points (1.1%) at 23620.13.

- Information Technology sector shares led gainers on the day, rebounding after opinions of the tech sector tied to AI has been overbought dissipated: Seagate Technology +12.62%, Micron Technology +8.69%, Western Digital +7.88%, First Solar +6.30% and Teradyne +6.26%.

- Communication Services and Consumer Discretionary sector shares followed: Match Group +6.69%, Paramount Skydance +2.83%, Charter Communications +2.33% and Meta Platforms +2.22% buoyed the Communication sector while the Discretionary sector was supported by Lululemon Athletica +5.12%, Wynn Resorts +4.17%, Marriott International +4.00%, Ford Motor +3.64% and Tesla +3.53%.

- Second half declines were led by a mix of Consumer Staples, Health Care and Utilities: Zimmer Biomet Holdings -14.38%, Live Nation Entertainment -7.95%, Charles River Laboratories -7.82%, Humana -7.63%, Axon Enterprise -7.61% and Archer-Daniels-Midland -4.81%.

- Earnings expected after today's close include: Albemarle Corp, McKesson Corp, Fortinet Inc, APA Corp, Duolingo Inc, Lucid Group Inc, DoorDash Inc, Snap Inc, AppLovin Corp, Robinhood Market, Lyft Inc, Enovix Corp, QUALCOMM Inc, Dutch Bros Inc and Fair Isaac Corp.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Trades Through The 20-day EMA

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6953.75 High Oct 30 and the bull trigger

- PRICE: 6851.00 @ 1416 ET Nov 5

- SUP 1:6748.50 Intraday low

- SUP 2: 6702.18 50-day EMA

- SUP 3: 6690.75 Low Oct 22

- SUP 4: 6571.25 Low Oct 17

The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. Support at the 20-day EMA, at 6803.81, has been breached. A clear break of this average signals scope for a deeper retracement and exposes the 50-day EMA at 6702.18 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

MNI COMMODITIES: WTI Slides, Precious Metals Rebound

- WTI has drifted lower in US hours but continues to hold broadly within the range seen since Oct 23 as supply outlooks remain in focus. US crude stocks saw their largest weekly increase since July.

- WTI Dec 25 is down by 1.5% at $59.6/bbl.

- US crude inventories for the week to Oct 24 built by 5.2mbbl compared to a Bloomberg survey expectation of a 0.25mbbl draw, but roughly in line with the API build of 6.5mbbl.

- WTI futures remain in a corrective cycle for now. First key support and the bear trigger is unchanged at $55.96, the Oct 20 low.

- On the upside, a clear move through initial resistance at $62.59, the Oct 24 high, would expose key resistance at $65.77, the Sep 26 high.

- Elsewhere, precious metals have rebounded today, with spot gold rising by 1.4% to $3,987/oz and silver by 2.2% to $48.2/oz.

- From a technical standpoint, the retracement in gold since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3,871.9.

- Initial resistance is at $4,161.4, the Oct 22 high.

- For silver, trend signals remain bullish, with initial resistance at $49.456, the Oct 23 high.

- Support to watch lies at the 50-day EMA, at $46.171.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 06/11/2025 | 0700/0800 | ** | Industrial Production | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0800/0900 | ** | Industrial Production | |

| 06/11/2025 | 0800/0900 | ** | Unemployment | |

| 06/11/2025 | 0810/0910 | ECB Schnabel At ECB Money Market Conference | ||

| 06/11/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/11/2025 | 0830/0930 | ECB De Guindos On Natixis Webinar | ||

| 06/11/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 06/11/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/11/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1230/1230 | BOE Press Conference | ||

| 06/11/2025 | 1330/0830 | *** | *Jobless Claims - suspended | |

| 06/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export - suspended | |

| 06/11/2025 | 1330/0830 | ** | Preliminary Non-Farm Productivity - suspended | |

| 06/11/2025 | 1400/1400 | Decision Maker Panel Data | ||

| 06/11/2025 | 1500/1000 | * | Ivey PMI | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade - suspended | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade - suspended | |

| 06/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 06/11/2025 | 1530/1030 | BOC Governor Macklem testifies at Senate. | ||

| 06/11/2025 | 1600/1100 | NY Fed's John Williams | ||

| 06/11/2025 | 1600/1100 | Fed Governor Michael Barr | ||

| 06/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 06/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 06/11/2025 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 06/11/2025 | 1830/1930 | ECB Lane At IMF Conference | ||

| 06/11/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 06/11/2025 | 2030/1530 | Fed Governor Christopher Waller | ||

| 06/11/2025 | 2130/1630 | Philly Fed's Anna Paulson | ||

| 06/11/2025 | 2230/1730 | St. Louis Fed's Alberto Musalem | ||

| 07/11/2025 | 2330/0830 | ** | Household spending |