MNI ASIA MARKETS ANALYSIS: Chip Makers Weighing on Equities

HIGHLIGHTS

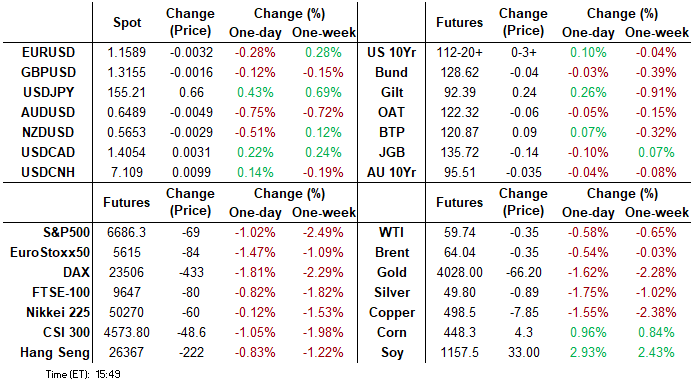

- Treasuries look to finish modestly higher, inside Monday's narrow range, decent volumes (TYZ5 over 1.3M) partially driven by quarterly futures roll with Mar'26 taking lead Friday.

- Federal Reserve Governor Christopher Waller said Monday the central bank should cut interest rates again next month because the labor market continues to deteriorate, while the inflationary effect of tariffs will be temporary.

- Canada's PM Mark Carney is expected to narrowly win this evening's vote on the 2026 federal budget, viewed as a confidence vote and risking a snap election if the gov't falls short of a majority.

- PM Sanae Takaichi is due to hold a meeting with Bank of Japan Governor Kazuo Ueda Tuesday, the first in-person meeting since Takaichi came to office.

US TSYS

MNI US TSYS: Gov Generated Data Gradually Resuming, Chip Makers Under Pressure

- Treasuries look to finish modestly higher Monday - inside a relatively narrow session range after scaling back from pre-NY open highs, backlogged economic data gradually starting to flow.

- Currently, the Dec'25 10Y contract trades +4 at 112-21 (112-15.5 low / 112-24.5 high), Treasuries last week challenged resistance at the 113-02 level, an area of congestion since Nov 5. This hurdle remains intact, however, a clear move above it would be a bullish signal and shift focus on resistance at 113-18+, the Oct 28 high. A break would also cancel a short-term bearish theme. For bears, attention is on 112-10, the 100-DMA and 112-06, the Sep 25 low.

- August construction data - whose Oct. 1 release was delayed 6 weeks due to the federal government shutdown - showed a 0.2% M/M rise in spending (-0.1% expected, 0.2% prior rev from -0.1%). The NY Fed's Empire State Manufacturing Survey impressed in November, with the current General Business Conditions index rising 8 points to a 1-year high 18.7 (well above the 5.8 expected).

- Fed Vice Chair Jefferson said he's likely one of the 9 FOMC members who anticipated cutting rates in Sep, Oct and Dec (in his September Dot Plot) and if forced to guess we would think he is still marginally in favor of a December cut and here he again highlights "increased downside risks to employment compared to the upside risks to inflation, which have likely declined somewhat recently".

- Stocks hit hard Monday, Chip makers continue to lead late session declines followed by Financial names. Note, Nvidia is expected to release Q3 earnings this Wednesday.

- Tuesday data schedule is light, with markets gearing for the now much-delayed September NFP print due this Thursday. Fed speak: Fed's Barkin is due to comment on the economic outlook having not commented directly on policy since the last Fed decision. Barkin had previously seen less caution around the jobs market given the unlikely circumstance of broad layoffs given such a slow pace of hiring in recent years.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.95% (-0.05), volume: $3.195T

- Broad General Collateral Rate (BGCR): 3.92% (-0.05), volume: $1.265T

- Tri-Party General Collateral Rate (TCR): 3.92% (-0.05), volume: $1.231T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.88% (+0.00), volume: $72B

- Daily Overnight Bank Funding Rate: 3.88% (+0.01), volume: $157B

FED Reverse Repo Operation

RRP usage rises to $3.172B with 7 counterparties this afternoon from last Friday's $1.559B - lowest level since mid-March 2021. Compares to this years highest excess liquidity measure off $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Treasury & SOFR option volumes were rather light Monday, underlying futures firmer - but off early session highs. Projected rate cut pricing appears steady to mixed vs late Friday levels (*): Dec'25 at -10.2bp (-10.8bp), Jan'26 at -20.1bp (-20.9bp), Mar'26 at -30.9bp (-30.8bp), Apr'26 at -37.6bp (-37.4bp).

SOFR Options:

+20,000 SFRZ5 96.18/96.25/96.31 call flys, 0.5 vs. 96.19/0.05%

4,000 SFRZ5 96.31/96.43 call spds

Block 2,500 2QH6 97.12 calls, 8.0 vs. 96.755

5,000 SFRZ5 96.18/96.25/96.31 put flys ref 96.183

2,000 SFRZ5 96.18/96.31 call spds vs. 0QZ5 97.00/97.12 call spds

1,125 SFRZ5 96.00/96.06/96.12 put flys ref 96.183

Treasury Options:

+40,000 wk4 US 106 puts, cab-7

16,800 TUZ5 104 puts, 2.5 ref 104-03

2,000 USF6 111/116 2x1 put spds

7,100 TYZ5 113/113.5 call spds

5,300 TYF6 113/114/115 1x3x2 call spds

10,300 TYZ5 113/TYF6 113.5 call spds, 17 net/Jan over

2,100 USF6/USG6 116 put spds ref 116-19

1,600 FVF6 108/108.75 put spds ref 109-09.25

3,500 TYF6 110/112 put spds ref 112-20

1,700 TYF6 114.5/115.5 call spds ref 112-18

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Regain Some Ground Vs Steady Bunds

Gilts handily outperformed Bunds Monday, following last week's fiscal-related underperformance.

- After significant bear steepening late last week on UK Chancellor Reeves's reported decision not to raise income tax rates, Gilts initially maintained their weakness relative to Bunds on Monday with little in the way of fresh drivers.

- However Gilts would regain some ground through the cash close, tracking gains in US Treasuries, with Bunds conversely failing to benefit, trading in a relatively narrow range throughout the session.

- That allowed Gilts to outperform on the day though the overall underperformance since last Thursday remains intact (10Y spread/Bund still 7bp wider).

- Periphery/semi-core EGB spreads closed mixed. Greek spreads fell 1.5bp following Friday's not-entirely-unexpected upgrade to BBB from Fitch, though BTPs outperformed overall; OAT spreads closed a little wider.

- Tuesday's calendar includes no tier-one European data, though there will be commentary by ECB's Dolenc and Pereira, and BOE's Pill and Dhingra; the focus of the week is Wednesday's UK CPI release.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.6bps at 2.042%, 5-Yr is down 0.4bps at 2.308%, 10-Yr is down 0.8bps at 2.712%, and 30-Yr is down 0.9bps at 3.31%.

- UK: The 2-Yr yield is down 4.6bps at 3.8%, 5-Yr is down 4.7bps at 3.964%, 10-Yr is down 3.9bps at 4.535%, and 30-Yr is down 4.5bps at 5.35%.

- Italian BTP spread down 1.7bps at 73.6bps / Greek down 1.5bps at 61.8bps

MNI EGB OPTIONS: Some Exiting Of Upside Leaning, Though Overall Upside Bias Remains

Monday's Europe rates/bond options flow included:

- RXZ5 129.50/129/128.50/128p condor (+1/-1.7/+0.4/+0.3), sold at 16.5 in 10

- RXG6 129.50/131.00/131.50/134.50 broken c condor vs 127.50/126.50ps, bought the condor for 4.5 and 5 in 7.5k

- ERM6 98.25/98.43/98.50/98.68 call condor vs 97.87 put. Buys back puts/sells call condor, paying 1.75 and 2 in 10k. Recall this was bought for example for 1.5 (bought condor vs put) in 10k on Oct 22

- ERM6 97.8125/98.3125RR, bought the Call for 0.75 in 8k

- ERM6 98.12/98.37cs, bought for 4 in 5k

- 0RH6 98.00^ bought in 4k vs 0RH6 96.68/98.18^^ sold in 6k Paid 13.25 and 13.5

MNI FOREX: USDJPY Takes Out Key Resistance; Broadens Upside Range

- PM Sanae Takaichi is due to hold a meeting with Bank of Japan Governor Kazuo Ueda Tuesday. This will be the first in-person meeting since Takaichi came to office, and comes as tensions have surfaced between Takaichi’s government and the BoJ. Any perceived pressure being put on the BoJ will be closely scrutinised by markets. This applies especially as further JPY weakness would increase the likelihood for a December BoJ hike which may act counter to Takaichi's dovish fiscal stance.

- The minutes of the RBA's November policy meeting are due - at which comments concerning the labour market will be very closely watched. October employment change data more than doubled median expectations, with a shift to fulltime employment particularly notable - any acknowledgement that a stronger jobs markets could limit RBA easing ahead could have trigger AUD strength. Into the minutes release, AUDUSD is holding above the 0.65 handle, underpinned by the 200-dma support longer-term, last crossing at 0.6457.

- Resultantly, the JPY is the poorest performing currency Monday, while GBP and NOK trade more favourably. EURGBP trades either side of the 0.88 handle, erasing a small part of the recent rally up to 0.8865.

- Tuesday data schedule is light, with markets gearing for the now much-delayed September NFP print due this Thursday. The central bank slate is busier: ECB's Pereira & Dolenc are set to make appearances as well as BoE's Pill & Dhingra. Lastly, Fed's Barkin is due to comment on the economic outlook having not commented directly on policy since the last Fed decision. Barkin had previously seen less caution around the jobs market given the unlikely circumstance of broad layoffs given such a slow pace of hiring in recent years.

MNI FX OPTIONS: Expiries for Nov18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-05(E915mln), $1.1675(E1.4bln), $1.1700(E1.0bln

- USD/JPY: Y153.00($1.3bln)

MNI US STOCKS: Late Equities Roundup: Technology Shares Underperforming

- Major equity indexes are extending late session lows Monday - following a couple of large program sales, one appr 1,470 names - largest since late October. Currently, the DJIA trades down 632.13 points (-1.34%) at 46515.95, S&P E-Minis down 86.5 points (-1.28%) at 6669.5, Nasdaq down 312 points (-1.4%) at 22590.45.

- Chip makers continue to lead late session declines followed by Financial names. Note, Nvidia is expected to release Q3 earnings this Wednesday.

- Dell Technologies -9.57%, Hewlett Packard Enterprise -8.48%, Super Micro Computer -6.89%, Arista Networks -4.14% and Skyworks Solutions -3.99%.

- Coinbase Global -8.59%, Robinhood Markets -7.81%, Capital One Financial -4.61% and Apollo Global Management -4.58%.

- Meanwhile, Health Care and Communication Services sector shares continued to lead late session advances:

- Alphabet +3.01%, Omnicom Group +0.71%, Interpublic Group +0.61% and T-Mobile +0.58%.

- Centene Corp +2.47%, Johnson & Johnson +1.89%, Regeneron Pharmaceuticals +1.83% and Amgen +1.59%.

- Larger names yet to announce earnings this week include: Aramark, Home Depot, Target Corp, Valvoline Inc, Lowe's Cos, Williams-Sonoma, TJX Cos, NVIDIA, Palo Alto Networks, Jacobs Solutions, Bath & Body Works, Walmart, Copart, Gap, Intuit, Ross Stores and BJ's Wholesale Club.

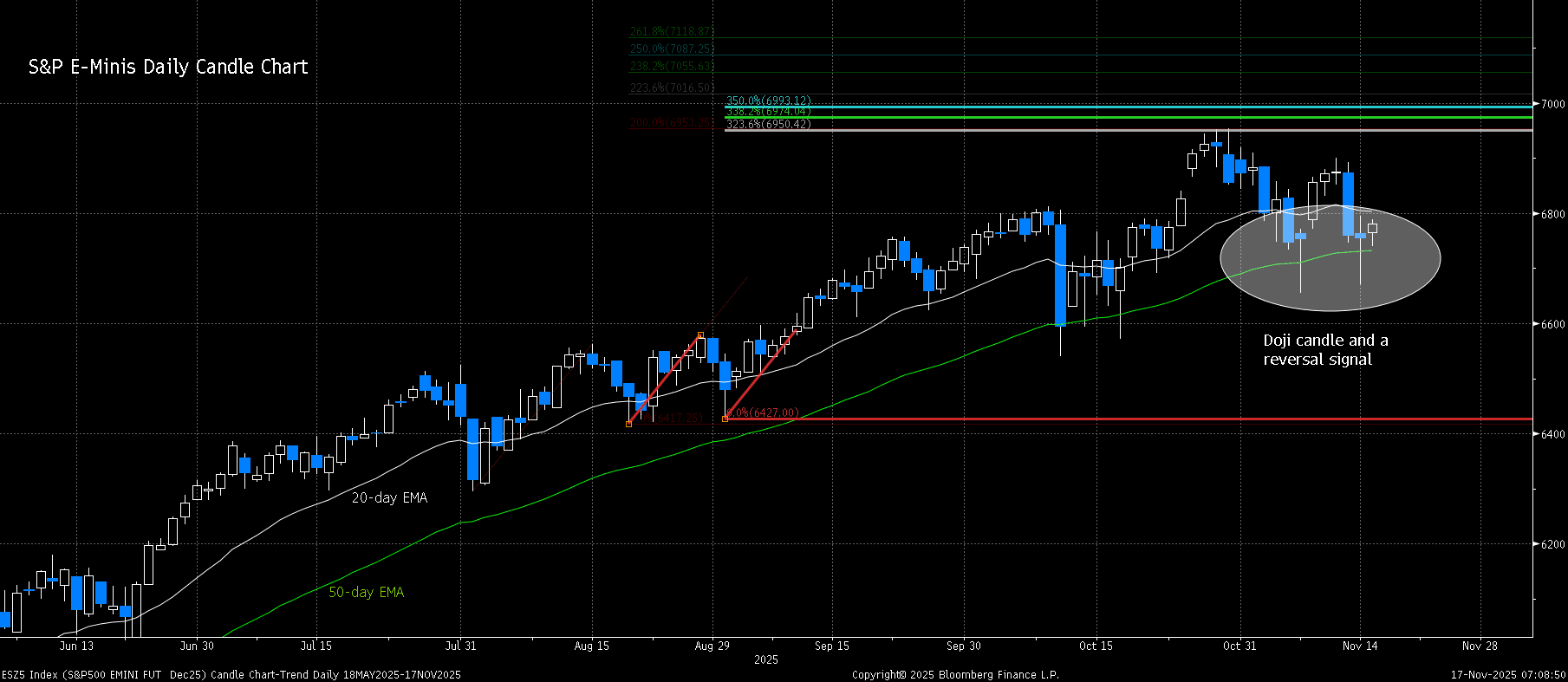

MNI EQUITY TECHS: E-MINI S&P: (Z5) Doji Reversal Candle

- RES 4: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6900.50 High Nov 12

- RES 1: 6804.35 20-day EMA

- PRICE: 6750.00 @ 14:35 GMT Nov 17

- SUP 1: 6670.50 Low Nov 14

- SUP 2: 6655.50 Low Nov 7 & key short-term support

- SUP 3: 6571.25 Low Oct 17

- SUP 4: 6540.25 Low Oct 10 and a key support

The trend condition in S&P E-Minis remains bullish and the latest selloff appears corrective - for now. Support at the 50-day EMA, at 6730.32, has been pierced, however, price is once again trading above the average. The next key support to watch is 6655.50, the Nov 7 low. Friday’s price pattern is a doji candle - a reversal signal. Initial firm resistance to watch is 6900.50, the Nov 12 high. A breach of this level would be bullish.

COMMODITIES

Oil End of Day Summary: WTI Falls Slightly

WTI has ticked down slightly today, with pressure from a resumption in loadings at Russia’s Novorossiysk following drone strikes Nov. 14.

- WTI DEC 25 down 0.3% at 59.93$/bbl

- Novorossiysk port resumed oil loadings on Sunday after a two-day suspension, according to Reuters sources and LSEG data.

- US congressman Linsey Graham said on X that Trump has given his blessing to a proposed bill which would slap tariffs of up to 500% on buyers of Russian oil.

- Ukraine claimed a new strike on the Novokuybyshevsk refinery in Russia’s Samara region on Nov. 16 as well as the Ryazan refinery on Nov. 15, damaging two primary processing units.

- The price of Russian Urals crude dropped to as low as $36.61/bbl on Thursday, the lowest since March 2023, ahead of US sanctions Nov. 21.

- Kazakhstan's government is not holding talks with Russia’s Lukoil regarding the purchase of the company's assets in Kazakhstan: Energy Minister

- Iraq’s government is discussing seeking a six-month sanctions waiver from the US Treasury for Lukoil.

- Almost two thirds of analysts and brokers surveyed by Bloomberg do not expect OPEC+ to cut output next year.

- Unsold cargoes in the Middle East at the start of November from the prior trading cycle found buyers in Asia eventually: Bloomberg.

- UBS expects Brent prices to remain within a $60-$70/bbl trading range, with a year-end target of $62/bbl, according to a note cited by Reuters.

- For 2026, Brent and WTI are seen averaging $56/b and $52/b respectively, compared to the current forward curves of $63/b and $60/b: Goldman Sachs

- Canada’s oil sands sector is undergoing a marked revival after years of lagging behind US shale, Bloomberg said.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/11/2025 | 1000/1100 | ECB Elderson at Banking Supervision Press Conference | ||

| 18/11/2025 | 1300/1300 | BOE Pill Fireside Chat on MonPol | ||

| 18/11/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 18/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/11/2025 | 1415/0915 | *** | Industrial Production | |

| 18/11/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1530/1030 | Fed Governor Michael Barr | ||

| 18/11/2025 | 1600/1100 | Richmond Fed's Tom Barkin | ||

| 18/11/2025 | 1700/1700 | BOE Dhingra on Income Growth and Consumption | ||

| 18/11/2025 | 2100/1600 | ** | TICS | |

| 18/11/2025 | 2300/1800 | Dallas Fed's Lorie Logan | ||

| 19/11/2025 | 2350/0850 | * | Machinery orders | |

| 19/11/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 19/11/2025 | 0030/1130 | *** | Quarterly wage price index |