MNI ASIA MARKETS ANALYSIS: Cautious Risk On Ahead Tariff Annc

HIGHLIGHTS

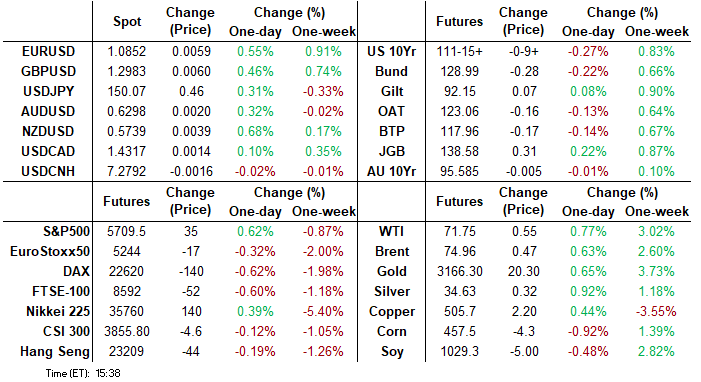

- Treasuries rallied after this morning's higher than expected ADP private jobs gain but retreated in steps off midmorning highs as stocks staged a modest rally off lows.

- A cautious risk-on tone ensued amid ongoing speculation over this afternoon's reciprocal tariff announcement from the White House Rose Garden while Senate votes on blocking Canadian tariffs this evening.

- Rates extended lows, stocks extended modest gains after Politico headlines announce that Elon Musk will step back from "governing partner" role in the next few weeks.

MNI US TSYS: Tsy Yields Higher Ahead Tariff Annc, ADP Gains Ahead NFP

- Treasury futures are trading weaker but off lows after the bell, main focus on this afternoon's reciprocal tariff announcement from the White House, scheduled for 1600ET. Much speculation through the day from ending tariffs on cheap (under $800) China imports to a 3-tier plan first mentioned by the WSJ on March 18.

- Treasuries rallied after this morning's higher than expected ADP private jobs gain but retreated in steps off midmorning highs as stocks staged a modest rally off lows. ADP employment growth was stronger than expected in March at 155k (cons 120k) after a marginally upward revised 84k (initial 77k) in February.

- Treasurys extended session lows after Politico headlines announce that Elon Musk will step back from "governing partner" role in the next few weeks. Several new outlets have announced over the last couple days that Musk would be stepping down from DOGE by the end of May.

- Treasuries Jun'25 10Y contract currently trades 111-17 (-8) vs. 111-09 low, technical support below at 110-26.5 (20-day EMA), compares to morning high of 112-02.5 with technical resistance above at 112-13 (1.500 proj of the Jan 13 - Feb 7 - Feb 12 price swing). Curves are mildly flatter, off early week highs: 2s10s -.127 at 28.245, 5s30s -1.002 at 58.799.

- Cross asset update: stocks bounce (SPX eminis +18.5 at 5693.00), Bbg US$ index -2.59 at 1270.69, Gold higher at 1325.93, crude firmer (WTI +.61 at 71.81).

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00034 to 4.31930 (-0.00435/wk)

- 3M -0.00364 to 4.27734 (-0.02027/wk)

- 6M -0.00244 to 4.16448 (-0.05113/wk)

- 12M -0.00869 to 3.95120 (-0.10166/wk)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (-0.02), volume: $2.589T

- Broad General Collateral Rate (BGCR): 4.35% (-0.01), volume: $972B

- Tri-Party General Collateral Rate (TCR): 4.35% (-0.01), volume: $936B

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $112B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $264B

FED Reverse Repo Operation

RRP usage inches up to $233.488B this afternoon from $230.063B on Tuesday. Usage had surged to the highest level since December 31, 2024 this past Monday: $399.167B. Compares to $58.770B (lowest level since mid-April 2021) on February 14. The number of counterparties at 41.

US SOFR/TREASURY OPTION SUMMARY

Uncertainty over this afternoon's reciprocal tariff announcement spurred heavy SOFR option volumes Wednesday, mixed flow wing outpacing Treasury options as underlying futures retreated from morning highs. Projected rate cuts through mid-2025 have receded vs. morning levels (*) as follows: May'25 at -3.4bp (-4.7bp), Jun'25 at -17.9bp (-21.2bp), Jul'25 at -33.1bp (-37.1bp), Sep'25 -49.6bp (-53.9bp).

SOFR Options:

+15,000 0QK5 96.12/96.25/96.37 put flys, 1.75 ref 96.54

+5,000 0QKJ5 96.12/96.25/96.37 put flys, 1.25 ref 96.56

Block, 6,000 SFRM5 96.12/96.50 call spds, 3.5 ref 95.915, adds to earlier Block at 3.75

+10,000 2QK5 96.00/96.25/96.50 1x3x2 put flys, 2.0 ref 96.62

+6,000 SFRZ5/0QZ5 97.00/98.00 call spd spd, 8.0 net conditional flattener

5,000 SFRZ5 95.12/95.62 put spds ref 96.415

10,000 SFRK5 96.37/96.87 call spds vs 2,500 95.87 puts, 0.0 net vs. 95.925/0.78%

-4,000 SFRU5 96.75/97.25 call spds, 4.5 ref 96.22

Block/screen, 33,000 SFRU5 95.25/95.75 put spds, 2.5 ref 96.22

Block/screen, 29,000 0QM5 96.81/97.00 call spds, 5.0 ref 96.615

26,000 0QU5 95.50 puts ref 96.635

3,500 0QM5 97.50 calls ref 96.62

2,000 SFRK5 95.62/95.75/95.81/95.87 broken put condors ref 95.93

8,000 SFRM5 95.62/95.68/95.87/95.93 put condors ref 95.92

13,700 SFRM5 95.68/95.75/95.81/95.87 put condors ref 95.92

1,500 SFRM5 96.00/96.25/96.37 broken call flys ref 95.92

2,000 SFRN5 96.12/96.25/96.37 call flys ref 96.205

2,100 2QM5 96.56/96.81 call spds vs. 95.68/95.81 put spds ref 96.555

6,000 0QM5 96.75/97.00 call spds ref 96.595 to -.59

+8,000 SFRM5 95.62/95.68/95.87/95.93 put condors, 3.5 vs. 95.895/0.05%

Block/screen +13,000 SFRM5 96.12/96.50 call spds 3.75 ref 95.92

Treasury Options:

2,000 FVM5 107/109.5 strangles, 41.5 ref 108-06.25

-3,750 TYN5 111.5 straddles, 240-238 ref 111-26.5

-15,000 TYK5 111 puts, 25 ref 111-26

12,900 wk2 TY 111.25/112 put spds, 22 ref 111-31.5 (exp Apr 11)

3,000 TYM5 109.5/110.5 put spds, 15 ref 111-30 to -30.5

+10,000 FVK5 107.5 puts, 8.5 ref 108-17.5, total volume over 12.5k

1,600 TYM5 112/113 call spds ref 111-26.5

1,100 FVK5 108.5/109/109.25/109.5 broken call condors

over 6,000 TYK5 111.5 calls, 55 ref 111-22.5

1,350 TYM5 112/114 call spds vs. 110 puts ref 111-21.5

-10,000 TYK5 113.25 calls, 17 ref 111-25

over 3,300 TYK5 114.5 calls ref 111-21.5

-5,000 Wed wkly 10Y 111.75/112 put spds, 13 ref 111-16.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Underperform Ahead Of US Tariff Announcement

Bunds underperformed in the European government FI space Wednesday in anticipation of the US tariff announcement after the cash close.

- Global core FI started the session on a positive note, with a risk-off tone with US tariff policy in focus.

- But Bunds and Gilts reversed sharply lower in afternoon trade following a Bloomberg sources piece saying the European Commission is mulling emergency measures to cushion the EU economy from the impact of US tariffs.

- On the day, the UK curve twist steepened, with Germany's bear steepening.

- Periphery/semi-core EGB spreads narrowed slightly, aided by the aforementioned headlines on EU measures.

- The US tariff announcement comes at 2100BST, with any European response closely eyed in the aftermath.

- Thursday's schedule includes Spanish and Italian March Services PMI (and finals elsewhere) and Eurozone PPI, along with appearances by ECB's Guindos and Schnabel and the accounts of the March ECB meeting.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.6bps at 2.038%, 5-Yr is up 2.4bps at 2.328%, 10-Yr is up 3.4bps at 2.721%, and 30-Yr is up 4.2bps at 3.072%.

- UK: The 2-Yr yield is down 0.5bps at 4.169%, 5-Yr is up 0.3bps at 4.257%, 10-Yr is up 0.6bps at 4.64%, and 30-Yr is up 0.3bps at 5.25%.

- Italian BTP spread down 0.7bps at 109.5bps / Spanish down 0.4bps at 62.4bps

MNI OPTIONS: Mix Of Call Spread Buying And Selling Wednesday

Wednesday's Europe rates/bond options flow included:

- OEK5 118.00/118.50cs sold at 22.5 in 10k

- ERJ5 with ERK5 97.75/97.6875ps vs 98.00c, bought the ps strip for half in 2k

- SFIZ5 96.75/97.25cs, bought for 3.75 in 2k

- SFIZ5 96.20/96.30cs vs 95.75/95.65ps, bought the cs for 2 in 2.5k

MNI FOREX: EURJPY Sharply Higher as Tariff Announcements Awaited

- A combination of EUR strength and USD weakness continues to play out across the US trading session, as the clocks ticks down headed into Trump's Rose Garden appearance at 1600ET/2100BST. The original EUR buying phase followed the Bloomberg report that the EU are planning emergency measures to guard the economy against Trump's tariffs, possibly bolstered by the rally through 1.0850 resistance and the weekly high.

- That report, twinned with headlines that Canada and Mexico are working to enhance their trade deal goes to show that tariffed countries are seemingly looking to take sharp action to both combat Trump's tariffs, as well as enhance cooperation to dampen the blow to economic growth that could follow the immediate installation of reciprocal tariffs today.

- Risk in general has also been significantly supported in anticipation of the tariff event, spurred on by reports suggesting that President Donald Trump has told his inner circle that Elon Musk will be stepping back in the coming weeks. Major US benchmarks latched on to the potential for a less strict regime at DOGE, and rallied over 2% from the lows in sympathy.

- This dynamic also weighed heavily on the Japanese yen, prompting USDJPY to rally back above 150.00 and EURJPY extend session gains to around 1%.

- For EURJPY, the trend structure in remains bullish and recent weakness appears corrective. The pullback has allowed an overbought condition to unwind. On the topside, attention is on 164.08, the Jan 24 high. A clear break of this hurdle would strengthen a bullish condition and open 164.90, the Dec 30 ‘24 high.

- Despite the softer USD and the renewed optimism for equities, the Mexican peso has underperformed since the US cash open, now 0.40% lower against the greenback. Standing out is the move for EURMXN, where the 1.4% advance (at peak) saw us breach the March highs, placing the cross at the highest level since November 06.

MNI FX OPTIONS: Expiries for Apr03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0800(E3.5bln), $1.0850(E1.1bln), $1.0875(E1.6bln), $1.0900(E863mln)

- USD/JPY: Y147.00($1.8bln), Y148.00($1.8bln), Y148.25-35($1.3bln), Y150.00($1.2bln)

- GBP/USD: $1.2840-50(Gbp868mln)

- EUR/JPY: Y165.90(E549mln)

- AUD/USD: $0.6290-00(A$920mln), $0.6320(A$566mln), $0.6400-10(A$1.8bln)

- NZD/USD: $0.5715-20(N$520mln)

- USD/CAD: C$1.4280($660mln), C$1.4370-75($1.2bln)

MNI US STOCKS: Late Equities Roundup: Midrange Ahead Tariff Announcement

- Stocks are holding modestly higher levels in late trade, near mid-range for the session as markets await Pres Trump's reciprocal tariff announcement scheduled for 1600ET.

- Though several news outlets announced over the last couple days that Elon Musk would be stepping down from DOGE by the end of May, stocks extended gains through midday after Politico reported that Musk will step back from "governing partner" role in the next few weeks.

- Currently, the DJIA trades up 125.99 points (0.3%) at 42114.26, S&P E-Minis up 20.25 points (0.36%) at 5695.75, Nasdaq up 89.3 points (0.5%) at 17539.26.

- Consumer Discretionary and Financial sectors outperformed in the second half, Caesars Entertainment +4.91%, , Tesla +4.40%, CarMax +4.17% and DoorDash +3.62% buoyed the Consumer Discretionary sector.

- Banks and services supported the Financial's sector with Discover Financial Services +3.28%, Invesco +2.86%, Synchrony Financial +2.80%, Blackstone +2.61% and Capital One Financial +2.23%.

- Consumer Staples and Communication Services sectors underperformed in late trade with Altria Group -4.29%, Mondelez International -2.65%, Hershey -2.54% and Philip Morris International -1.75% weighing on the former.

- Meanwhile, telecom stocks weighed on the Communication Services sector: T-Mobile -1.89%, Verizon Communications -1.59%, AT&T -1.18% and Comcast Corp -1.08%.

MNI EQUITY TECHS: E-MINI S&P: (M5) MA Studies Highlight A Dominant Downtrend

- RES 4: 5878.53 50-day EMA

- RES 3: 5837.25 High Mar 25 and a key resistance

- RES 2: 5757.95 20-day EMA

- RES 1: 5694.75 High Apr 1

- PRICE: 5683.00 @ 1500 ET Apr 2

- SUP 1: 5559.75/33.75 Low Mar 13 and the bear trigger / Low Mar 31

- SUP 2: 5500.00 Round number support

- SUP 3: 5483.50 2.00 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

- SUP 4: 5396.00 2.236 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

S&P E-Minis maintain a softer tone. Sights are on key support and the bear trigger at 5559.75, the Mar 13 low. It has been pierced, a clear break of it would confirm a resumption of the downtrend that started Feb 19, and open 5483.30, a Fibonacci projection. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. Key short-term resistance has been defined at 5837.25, the Mar 25 high.

MNI COMMODITIES: Crude Gains, Gold Edges Up As Tariff Announcement Awaited

- WTI Crude is higher on the day ahead of details on US reciprocal tariffs due to be announced at 2100BST/1600ET. The potential impact on global demand from increased trade protectionism and rising OPEC+ supply is weighed against the potential for tougher sanctions on Iran and US tariffs on buyers of Russian oil.

- WTI May 25 is up by 0.8% at $71.8/bbl.

- President Trump has said that the tariffs will take effect immediately, while Treasury Secretary Bessent stated that there will be a “cap” and that countries can negotiate to reduce the tariff they face below this. There could be a tiered tariff structure along with specific reciprocal taxes, according to Bloomberg.

- The sharp rally in WTI futures earlier this week undermines the medium-term bearish condition and signals scope for a continuation higher near-term, exposing the next key resistance at $72.91, the Feb 11 high.

- Meanwhile, spot gold has consolidated below yesterday’s record high, as the market awaits Trump’s tariff announcement, with the yellow metal edging up by 0.3% to $3,123/oz.

- Analysts at Mizuho Securities said that those invested in gold as a safe haven are not likely to sell quickly even if the reciprocal tariff announcement is a non-event. They expect safe haven flows to ride out the storm.

- From a technical perspective, the trend condition in gold remains bullish, with sights on $3,151.5 next, a Fibonacci projection.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/04/2025 | 0630/0830 | *** | CPI | |

| 03/04/2025 | 0700/0300 | * | Turkey CPI | |

| 03/04/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/04/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/04/2025 | 0720/0920 | ECB's De Guindos On "Financial Stability In Uncertain Times" | ||

| 03/04/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/04/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/04/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/04/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/04/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/04/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/04/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/04/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/04/2025 | 0830/0930 | Decision Maker Panel data | ||

| 03/04/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/04/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/04/2025 | 0900/1100 | ** | PPI | |

| 03/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/04/2025 | 1000/1200 | ECB's Schnabel At OECD Seminar | ||

| 03/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 03/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 03/04/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 03/04/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 03/04/2025 | 1230/0830 | ** | Trade Balance | |

| 03/04/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/04/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/04/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 03/04/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 03/04/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 03/04/2025 | 1630/1230 | Fed Vice Chair Philip Jefferson | ||

| 03/04/2025 | 1830/1430 | Fed Governor Lisa Cook | ||

| 04/04/2025 | 2330/0830 | ** | Household spending |