MNI ASIA MARKETS ANALYSIS: Budget Bill Vote Stalls In House

HIGHLIGHTS

- Treasuries reversed early knee-jerk gain after the unexpected ADP private jobs loss for June (-33k vs. +98k est), markets eying June jobs data scheduled tomorrow ahead of Friday's Independence Day holiday closure.

- US President Donald Trump posted on Truth Social: "I just made a Trade Deal with Vietnam", stocks gained on the news.

- A House vote on rule to progress the OBBB did not look imminent in late trade.

US TSYS

MNI US TSYS: Surprise ADP Jobs Loss Ahead Thursday's June NFP Report

- Treasuries look to finish weaker Wednesday, well off early session highs after a brief knee-jerk reaction to an unexpected ADP private jobs loss rather than an expected gain. Focus turned to trade talk and Thursday's jam-packed data session that includes June NFP as markets are closed Friday for the 4th of July Holiday.

- Punchbowl's Jake Sherman suggests that a House vote on the "rule" to advance toward a debate and full vote on the "One Big Beautiful Bill" is not imminent, due to insufficient Republican votes at this stage.

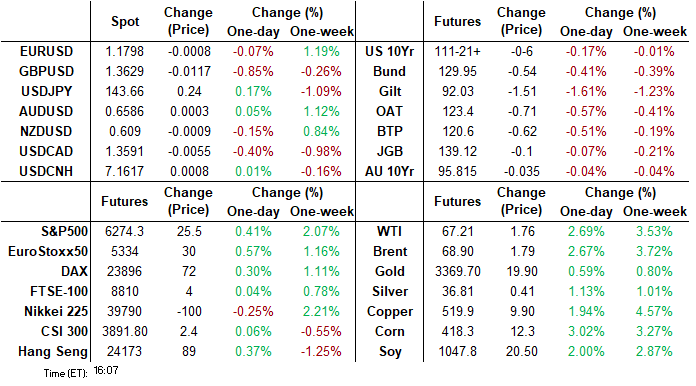

- The Sep'25 10Y contract trades -6 at 111-21.5 vs. session and 1W low of 111-16.5. First key support to watch is 111.07.5, the 20-day EMA. Curves remain steeper but off highs: 2s10s +2.691 at 49.404 (52.814H), 5s30s +1,844 at 94.608 (98.661H).

- ADP private sector employment was much weaker than expected in June as it fell -33k (sa, cons 98k) along with last month’s soft print confirmed with a downward revision to 29k vs the initial 37k. The decline was led by professional & business services (-56k after -13k, its sharpest decline since Feb 2023) and education & health services (-52k after -16k, its sharpest decline since Jul 2020).

- Pres Trump announced a trade deal with Vietnam. "The Terms are that Vietnam will pay the United States a 20% Tariff on any and all goods sent into our Territory, and a 40% Tariff on any Transshipping. In return, Vietnam will do something that they have never done before, give the United States of America TOTAL ACCESS to their Markets for Trade. In other words, they will “OPEN THEIR MARKET TO THE UNITED STATES,” meaning that, we will be able to sell our product into Vietnam at ZERO Tariff."

- Political uncertainty in the UK heavily weighed on sterling Wednesday, as markets speculated that Rachel Reeves’ term as Chancellor of the Exchequer might be coming to an end. Prime Minister Sir Keir Starmer refused to publicly back his Chancellor, in a testing session of PMQs in the House of Commons, heightening the market’s fiscal concerns.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.44% (-0.01), volume: $2.920T

- Broad General Collateral Rate (BGCR): 4.39% (+0.00), volume: $1.114T

- Tri-Party General Collateral Rate (TCR): 4.39% (+0.00), volume: $1.084T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $133B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $264B

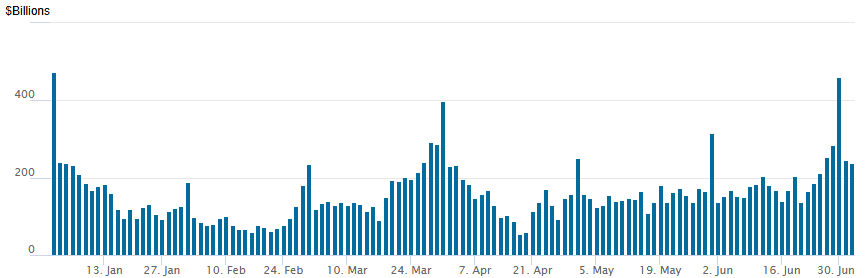

FED Reverse Repo Operation:

RRP usage slips to $237.307B this afternoon from $245.530B yesterday, total number of counterparties at 45. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow remained mixed in late trade, SOFR options shifted toward low calls structures with underlying futures trading weaker, curves bear steepening ahead of tomorrow's heavy data dump that includes June NFP ahead Fri's holiday closure.. That said, projected rate cut pricing firmed slightly vs. morning (*) levels: Jul'25 at -5.8bp (-4.8bp), Sep'25 at -29.4bp (-28.1bp), Oct'25 at -45.6bp (-44.3bp), Dec'25 at -64.7bp (-63.5bp).

SOFR Options:

10,000 SFRH6 96.75/97.00 call spds 16.5 vs. 96.565/0.24%

over 10,700 SFRZ5 96.37/96.43/96.50/96.56 call condors ref 96.325

-5,000 SFRN5 95.75/95.93/96.00/96.18 call condors, 13.25 - more offered

-5,000 SFRN5 96.00 calls, 4.5-4.25 ref 95.99

+5,000 SFRU6 98.00/99.00 2x3 call spds, 8.0 ref 96.86

+5,000 SFRU5 96.00/96.25/96.50 1x3x2 call flys, 2 ref 96.00

2,500 3QQ5 96.37/96.50 2x1 put spds ref 96.55

-2,000 SFRN5 95.75/95.87/96.00 put flys, 3.5

Block, 5,938 SFRU5 96.00/96.25/96.50 call flys, 4.0 vs. 95.985/0.15%

Block, 5,750 0QN5 97.18 calls, 1.5 ref 96.90

+2,000 SFRQ5 96.00/96.18 call spds, 4.25 ref 95.98

+2,000 SFRN5 95.87/95.93 3x2 put spd, 2.75 ref 95.98

+8,000 SFRZ5 95.75/95.87/96.25/96.37 put condors, 6.0 vs. 96.225/0.05

+2,000 SFRU5 96.12/96.25/96.37 call flys, 1.5 ref 95.975

Block/screen -5,000 SFRU5 96.00/96.31 call spds, 6.0 ref 95.975

Treasury Options:

4,000 TYU5 114/115 call spds ref 111-18

6,000 USU5 104/107 2x1 put spds, 0.0 ref 114-23

2,000 USQ5 110 puts, 7

1,800 TYQ5 111.5/112.5 call spds, 25 ref 111-21

+1,500 110/111 2x1 put spds, 8 vs. 111-18.5/0.05%

3,000 TUQ5 103.25/103.5/103.62/103.75 broken put condors ref 103-27.88

over 7,700 TYQ5 110 puts, ref 111-22.5

over 6,700 TYQ5 110.5 puts, ref 111-21

+2,000 FVQ5 109/109.75 1x2 call spds, 4 vs 108-22.75/0.08%

+2,500 TYU5 109/110/111 put trees, 9 vs. 111-17/0.03%

MNI EGB BONDS: EGBs-GILTS CASH CLOSE: Gilts Sell Off On Fiscal Concerns

Gilt yields soared Wednesday on renewed concerns over the UK's fiscal outlook.

- Gilts weakened sharply in early afternoon trade amid speculation that UK Chancellor Reeves could leave her post after the government was forced to water down its welfare reform bill. EGBs weakened in tandem.

- UK yields later edged off their highs after PM Starmer expressed his "full support" for Reeves but the damage was done, in one of the worst sessions for the long end in the last 2+ years including a 20+bp rise for the 30Y at one point.

- In some constructive developments for bonds, BoE MPC member Taylor elicited a dovish short-end reaction after saying 5 cuts might be needed; while there was a brief Treasury-led rally after US private payrolls unexpectedly contracted. Also, Italian/Eurozone unemployment came in higher than expected.

- Both the German and UK curves bear steepened on the day, with Gilts of course underperforming Bunds. Periphery/semi-core EGB spreads tightened, led by Spain.

- Thursday's calendar includes final Services PMIs and the account of the June ECB policy meeting. Global attention will be on US pre-holiday data, including the nonfarm payrolls report, with some attention also paid to Swiss inflation.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.4bps at 1.863%, 5-Yr is up 3.5bps at 2.183%, 10-Yr is up 9bps at 2.664%, and 30-Yr is up 6.4bps at 3.117%.

- UK: The 2-Yr yield is up 5.4bps at 3.881%, 5-Yr is up 10.6bps at 4.042%, 10-Yr is up 15.8bps at 4.612%, and 30-Yr is up 19.1bps at 5.42%.

- Italian BTP spread down 2.5bps at 85bps / Spanish down 2.8bps at 61.2bps

MNI OPTIONS: UK Rate Selloff Meets With Upside Plays

Wednesday's Europe rates/bond options flow included:

- ERQ5 98.125/98.25cs 1x2, bought the 1 for 2 in 5k

- ERQ5 98.125/98.1875/98.25c ladder, bought for 1.25 in 4k

- SFIZ5 96.40/96.50cs, bought for 3.5 in 8k

- SFIZ5 96.60c, bought for 5.5 in 7.5k

- SFIZ5 96.50/96.75/97.00c fly, bought for 3 in 6k

MNI FOREX: GBP Under Significant Pressure as Political Uncertainty Ramps Up

- Political uncertainty in the UK heavily weighed on sterling Wednesday, as markets speculated that Rachel Reeves’ term as Chancellor of the Exchequer might be coming to an end. Prime Minister Sir Keir Starmer refused to publicly back his Chancellor, in a testing session of PMQs in the House of Commons, heightening the market’s fiscal concerns.

- GBPUSD remains roughly 1% lower on the session as we approach the APAC crossover, having traded as low as 1.3563 amid the tumult, during which the 30-yr gilt yield rose as much as 22bps at its extreme. 20-day EMA support was pierced below 1.3586 and a sustained break of this average would signal scope for a more pronounced corrective pullback. The 50-day, which has supported dips well in recent months, intersects at 1.3439.

- For EURGBP, this week’s gains are reinforcing current bullish conditions. 0.8592, 61.8% of the Apr 11 - May 29 downleg, has been broken, as well as 0.8624, the Apr 21 high. Above here, the next significant targets are 0.8694 and 0.8738, the Apr 14 & 11 highs respectively. GBPJPY is also extending towards an important area, located around 195.00.

- Elsewhere, the dollar index trades on a slightly firmer footing, up around 0.25% on the session as markets await the significant US employment report on Thursday. Two key factors have helped stabilise the greenback: the reversal higher for US yields from dovish extremes and an important technical support holding for the DXY, a trendline drawn across the 2011 and 2021 lows.

- Aside from the GBP weakness, NZD moderately underperforms its G10 peers, down 0.40% and consolidating back below 0.6100. Despite the moderate losses for both Aussie and Kiwi today, the medium-term bullish trends for both AUDUSD and NZDUSD have been bolstered this week ahead of RBA and RNBZ central bank decisions next week. For AUD, sights remain on key resistance at 0.6688, the US election related highs.

- US employment report and ISM services headline a packed US calendar on Thursday.

MNI FOREX OPTIONS: Expiries for Jul03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E2.1bln), $1.1600(E3.8bln), $1.1625(E1.2bln), $1.1650-60(E1.8bln), $1.1700(E2.7bln), $1.1720-25(E1.2bln), $1.1750(E1.1bln), $1.1775(E2.2bln), $1.1800(E5.1bln), $1.1825(E1.2bln), $1.1850(E880mln), $1.1900(E1.2bln)

- USD/JPY: Y142.00($1.1bln), Y143.95-00($1.0bln), Y144.50($540mln), Y145.00-10($1.2bln)

- EUR/GBP: Gbp0.8640-50(E787mln)

- AUD/USD: $0.6500(A$802mln), $0.6600(A$958mln)

- AUD/NZD: N$1.0775(A$597mln)

- USD/CAD: C$1.3600($1.7bln), C$1.3640-45($505mln), C$1.3690-10($736mln)

- USD/CNY: Cny7.4000($3.0bln)

MNI US STOCKS: Late Equities Roundup: IT & Materials Continue to Outperform

- Stocks are inching higher in late Wednesday trade, Dow Jones Industrials still mildly weaker vs. decent gains in Nasdaq with tech stocks bouncing. Currently, the DJIA trades down 19.36 points (-0.04%) at 44475.64, S&P E-Minis up 22.5 points (0.36%) at 6271.25, Nasdaq up 168.1 points (0.8%) at 20371.28.

- Helping support equities earlier - Pres Trump announced a trade deal with Vietnam. "The Terms are that Vietnam will pay the United States a 20% Tariff on any and all goods sent into our Territory, and a 40% Tariff on any Transshipping. In return, Vietnam will do something that they have never done before, give the United States of America TOTAL ACCESS to their Markets for Trade. In other words, they will “OPEN THEIR MARKET TO THE UNITED STATES,” meaning that, we will be able to sell our product into Vietnam at ZERO Tariff."

- Leading gainers in the Information Technology sector included: First Solar +7.70%, NXP Semiconductors +4.81%, Seagate Technology +4.38%, ON Semiconductor +4.18%, Applied Materials +3.38% and Super Micro Computer +2.80%. The Materials sector followed with miners, chemicals and steel producers remained elevated in late trade: Albemarle Corp +8.16%, Freeport-McMoRan +3.29%, Nucor +2.62%, Dow Inc +2.53% and The Mosaic Co +2.34%.

- Health Care sectors continued to weigh on major averages in the second half, care and services providers weighed on the former with Centene hammered -39.44% after withdrawing earnings guidance for 2025. Following suit, Molina Healthcare fell -20%, Elevance Health -9.41%, UnitedHealth Group -4.03%, Cigna Group -2.81% and Humana -2.74%.

- The Wall Street Journal reported “Centene's move comes after industry bellwether UnitedHealth pulled its guidance for the year and replaced its chief executive. It is likely to add to investors' nervousness about the entire insurance sector, which has felt the effect of higher-than-expected medical costs. Humana and CVS Health's Aetna struggled last year, with CVS also bringing on a new CEO."

MNI EQUITY TECHS: E-MINI S&P: (U5) Approaching Key Resistance

- RES 4: 6300.00 Round number resistance

- RES 3: 6281.12 1.618 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6277.50 High Feb 19 and a bull trigger

- RES 1: 6270.75 Intraday high

- PRICE: 6266.75 @ 1400 ET Jul 3

- SUP 1: 6102.47/5975.80 20- and 50-day EMA values

- SUP 2: 5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract has continued to appreciate, this week. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has recently been breached. The clear break confirms a resumption of the uptrend that started Apr 7. The 6200.00 handle has been cleared too, this opens 6277.50, the Feb 21 high and bull trigger. Key support is at the 50-day EMA - at 5975.80.

MNI COMMODITIES: Crude Extends Gains, Copper At Three-Month High

- WTI has extended gains, with the market weighing improved economic prospects ahead of expected US trade deals. The market seems to have already priced in expectations of another large OPEC+ output hike in August.

- WTI Aug 25 is by 3.1% at $67.5/bbl.

- Goldman Sachs sees no major market reaction from OPEC+ production hikes as consensus already shifts to a further increase on Sunday.

- Meanwhile, President Trump has vowed to replenish the US emergency oil reserve, taking advantage of low crude prices.

- For WTI futures, initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range.

- Elsewhere, spot gold has traded in a tight range ahead of tomorrow’s US payrolls data, with the yellow metal edging up by 0.4% to $3,352/oz.

- Gold’s recovery from Monday’s low highlights a possible false trendline break earlier this week. Stronger gains would refocus attention on $3,451.3, the June 16 high.

- Copper has rallied by 2.1% today to new three-month highs at $521/lb.

- Analysts at Julius Baer said that the move reflects the impact of trade tariffs, with a surge in US imports leaving supply looking tight.

- Copper futures remain in a bull cycle, with price piercing resistance at $514.43. A clear break would pave the way for a climb towards $546.15, the Mar 26 high and a key resistance.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/07/2025 | 0630/0830 | *** | CPI | |

| 03/07/2025 | 0700/0300 | * | Turkey CPI | |

| 03/07/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0830/0930 | Decision Maker Panel data | ||

| 03/07/2025 | 0830/0930 | BOE Credit Conditions Survey | ||

| 03/07/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/07/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 03/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 03/07/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 03/07/2025 | 1230/0830 | *** | Employment Report | |

| 03/07/2025 | 1230/0830 | ** | Trade Balance | |

| 03/07/2025 | 1230/0830 | ** | Trade Balance | |

| 03/07/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/07/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/07/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/07/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/07/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/07/2025 | 1400/1000 | * | US Bill 08 Week Treasury Auction Result | |

| 03/07/2025 | 1400/1000 | ** | US Bill 04 Week Treasury Auction Result | |

| 03/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 03/07/2025 | 1500/1100 | Atlanta Fed's Raphael Bostic | ||

| 03/07/2025 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill | |

| 03/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 04/07/2025 | 2330/0830 | ** | Household spending |