MNI ASIA MARKETS ANALYSIS: Anticipating Hawkish Fed Cut?

HIGHLIGHTS

- Treasuries look to finish moderately lower despite massive buy/blocks crossed in Mar'26 5- and 10Y futures, sentiment cautiously positive following this morning's mixed data.

- Next week focus on the FOMC decision, widely expected to deliver a third consecutive 25bp cut after NY Fed Williams’ uncharacteristic guidance following the delayed September payrolls report.

- Two-way swings left the USD index close to unchanged on Friday, but importantly the index is consolidating a solid 0.5% decline this week, as a short-term bearish bias dominates the narrative.

US TSYS

MNI US TSYS: Ylds Rise Ahead Expected 25Bp Cut from Fed, Potential Hawkish Messaging

- US treasuries look to finish moderately weaker Friday, near midday lows despite heavy buy blocks in Mar'26 5- and 10Y futures (+97k and +80k respectively).

- Currently, the TYH6 contract trades -6 at 112-17 vs. 112-15 low. Price traded through the 50-day EMA at 112-27 earlier in week. A clear breach of this average undermines a recent bull theme and signals scope for a deeper retracement, potentially towards 112-07, the Nov 5 high and a bear trigger.

- Sentiment was cautiously positive ahead of an expected 25bp rate cut from the Fed next week (potential for hawkish messaging), while the morning's mixed data spurred some position squaring.

- U.Mich consumer sentiment was higher than expected in the preliminary December release, as better expectations offset disappointing current conditions. It was supported by lower inflation expectations but we continue to caution reading too much into these preliminary results.

- The delayed personal income and outlays report for September saw a decline in goods spending offset more-of-the-same for services consumption. It still left real spending up a solid 2.7% in Q3 whilst the savings rate saw a second month at its lowest since December.

- Next week is dominated by the FOMC decision, widely expected to deliver a third consecutive 25bp cut after NY Fed Williams’ uncharacteristic guidance following the delayed September payrolls report. It’s likely to be a contentious meeting though with many FOMC members preferring to have paused.

- Being a SEP meeting, the dot plot distribution will be watched keenly whilst we expect the economic projections to show an upward revision for GDP growth and downward revision for core PCE inflation.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.92% (-0.03), volume: $3.300T

- Broad General Collateral Rate (BGCR): 3.87% (-0.03), volume: $1.320T

- Tri-Party General Collateral Rate (TCR): 3.87% (-0.03), volume: $1.298T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $87B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $173B

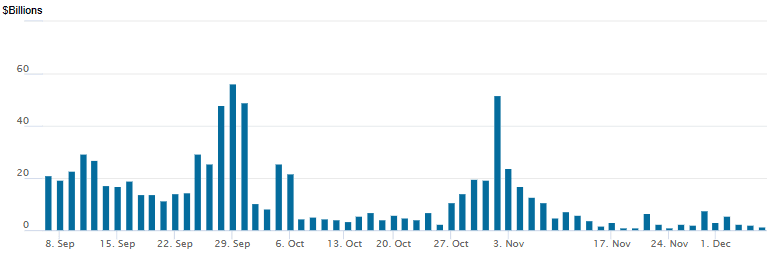

FED Reverse Repo Operation

RRP usage slips to $1.485B with 8 counterparties this afternoon from $2.233B Thursday. Compares to last Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Very light SOFR & Treasury option volumes Friday, accounts squared and pared as they ply the sidelines ahead of next week's FOMC policy annc. Likely to be a contentious meeting though with many FOMC members preferring to have paused. Underlying futures moderately lower, curves mixed (2s10s +0.110 at 57.452, 5s30s -.114 at 107.902). Projected rate cut pricing steady vs early morning levels (*): Dec'25 at -23.8bp, Jan'26 at -31.0bp, Mar'26 at -38.7bp, Apr'26 at -45bp (-45.5bp).

SOFR Options: (Dec SOFR options expire next Friday)

4,600 SFRH6 96.62/96.87 call spds

14,000 SFRZ5 96.25/96.37 box ref 96.2675

2,500 SFRM6 98.00 calls ref 96.665

2,000 SFRZ5 96.18/96.25/96.31 call flys ref 96.27

2,000 0QG6 97.00/97.25 1x2 call spds ref 96.915

10,250 SFRH6 96.31/96.37/96.50/96.56 put condors, 1.25 ref 96.45

Treasury Options:

1,800 TYF6 114.5 calls, 4

+2,300 FVF6 111 calls, 2

2,300 TYF6 111.5 puts, 6

EGBS

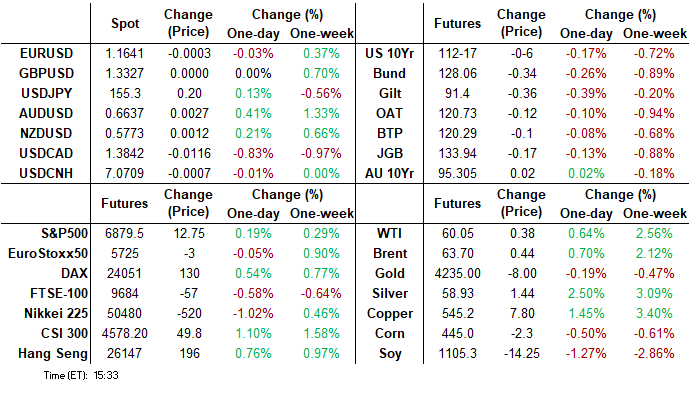

| Futures | Change (Price) | Change (%) | ||

| One-day | One-week | |||

| Bund | 128.44 | -0.18 | -0.14% | -0.73% |

| Gilt | 91.76 | 0.08 | 0.09% | 0.28% |

| OAT | 120.84 | -0.26 | -0.21% | -0.88% |

| BTP | 120.39 | -0.24 | -0.20% | -0.60% |

| AU 10Yr | 95.285 | -0.06 | -0.06% | -0.22% |

MNI FOREX: DXY Consolidates Weekly Decline, CAD Soars Post Employment Report

- Two-way swings left the USD index close to unchanged on Friday, but importantly the index is consolidating a solid 0.5% decline this week, as a short-term bearish bias dominates the narrative. Fed easing expectations and associated risk-on dynamics continue to weigh on the greenback.

- There has been an impressive 0.9% selloff for USDCAD on Friday following the impressive employment report for November, where the unemployment rate dipped to the 6.5%, the lowest level since July 2024.

- Tepid trade talk optimism and technical breaks have exacerbated the USDCAD declines. Both the breach of the bull channel around 1.3940, and the clean break of key 1.3888 support significantly bolster the renewed bearish theme, placing 1.3812 and 1.3727 as the next chart points of note. As a reminder, we have both the BOC and FOMC rate decisions next week, likely to keep the spotlight on USDCAD in coming sessions.

- Elsewhere, AUDUSD traded further above the late October highs of 0.6618 to reach a session peak of 0.6649, the highest level since mid-September. The pair has now posted 10 consecutive sessions of higher highs, as the bullish impulsive wave extends. With a number of resistance points being cleared, targets on the topside are now found at 0.6660 (Sep 18 high) and 0.6723, the Oct 21 2024 high.

- In emerging markets, the Brazilian real came under significant pressure on Friday as reports were confirmed that Ex-President Jair Bolsonaro will throw his support behind his son Flavio for next year’s presidential candidate. USDBRL rose over 2% on the sharp increase in potential political uncertainty ahead.

MNI OPTIONS: Expiries for Dec08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E831mln), $1.1670(E587mln), $1.1800(E1.8bln), $1.2140(E2.9bln)

- USD/JPY: Y155.00($1.2bln), Y156.00($1.5bln)

- AUD/USD: $0.6475-80(A$1.0bln)

- USD/CAD: C$1.3940($841mln)

MNI US STOCKS: Late Equities Roundup: Health Care, Discretionary Shares Outperform

- Stocks continue to hold modest gains late Friday, inside session ranges after climbing to the best levels since late October (SPX eminis) to early November (DJIA) this morning. Currently, the DJIA trades up 149.04 points (0.31%) at 48000.02, S&P E-Mini Futures up 11.75 points (0.17%) at 6878.75, Nasdaq up 45.3 points (0.2%) at 23551.49.

- Sentiment was cautiously positive ahead of an expected 25bp rate cut from the Fed next week (potential for hawkish messaging), while the morning's mixed data spurred some position squaring.

- U.Mich consumer sentiment was higher than expected in the preliminary December release, as better expectations offset disappointing current conditions. It was supported by lower inflation expectations but we continue to caution reading too much into these preliminary results.

- The delayed personal income and outlays report for September saw a decline in goods spending offset more-of-the-same for services consumption. It still left real spending up a solid 2.7% in Q3 whilst the savings rate saw a second month at its lowest since December.

- A mix of Materials, Health Care and Consumer Discretionary sector shares led advances in the first half: Ulta Beauty +12.92% after beating Q3 earnings estimates, Dollar Tree +8.07%, Moderna +7.45%, Cooper Cos Inc +7.41%, Dollar General +7.11%, Sandisk Corp +6.68%, Southwest Airlines +6.28% and Albemarle Corp +6.26%.

- Meanwhile, leading decliners included: Paramount Skydance -7.66% (after Netflix struck a $82.7B deal to buy Warner Bros), W R Berkley -5.02%, Vistra Corp -4.20%, Robinhood Markets -3.74%, Insulet Corp -3.73%, Huntington Ingalls Ind -3.62% and Netflix -3.53%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bullish Theme

- RES 4: 7000.00 Psychological round number

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6900.50 High Nov 12

- RES 1: 6886.25 Intraday high

- PRICE: 6872.50 @ 14:23 GMT Dec 5

- SUP 1: 6788.55 20-day EMA

- SUP 2: 6674.50/6525.00 Low Nov 25 / 21

- SUP 3: 6500.00 Round number support

- SUP 4: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

A bullish theme in S&P E-Minis is intact and the contract continues to appreciate. Price remains above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6788.55, the 20-day EMA.

COMMODITIES

MNI AMERICAS OIL: US OIL: December 5 - Americas End of Day Oil Summary: Crude Higher

WTI Crude has risen slightly higher and is now on track for a small net gain on the week amid stalled Ukraine peace talks, further potential EU/G7 actions against Russia, and geopolitical risks in Venezuela, outweighing concerns for a market surplus heading into 2026. US consumer sentiment was higher in the December reading.

- The US total oil and gas rig count was up 5 rigs on the week at 549 rigs, according to Baker Hughes. This puts total US oil and gas rigs down 40, or 6.8% on the year. Oil: 413 (6) - down 69 rigs, or 14.3% on the year. Canada: 191 (+3) - down 3 rigs, or 1.5% on the year.

- The G7 and European Union are in talks to scrap the oil price cap on Russia and instead impose a full ban on Russia accessing maritime services in order to disrupt its oil exports, sources told Reuters. Russia exports over a third of its oil in Western tankers.

- Ukraine and Russia talks appeared stalled, with Putin emphasizing that several points in the US backed peace plan were unacceptable. Talks between Umerov and Witkoff will take place in Miami today.

- OPEC’s oil output edged lower in November despite higher quotas due to outages in some member countries, according to a Reuters and Bloomberg surveys.

- WTI Jan futures were up 0.7% at $60.08

- WTI Feb futures were up 0.8% at $59.78

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/12/2025 | 0700/0800 | ** | Industrial Production | |

| 08/12/2025 | - | *** | Trade | |

| 08/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 08/12/2025 | 1430/1430 | BOE Taylor Panel on Growth/Wealth/Debt | ||

| 08/12/2025 | 1500/1600 | ECB Cipollone Lecture at Frankfurt School of Finance & Management | ||

| 08/12/2025 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 08/12/2025 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/12/2025 | 1830/1830 | BOE Lombardelli Panel on Women in Economics | ||

| 08/12/2025 | - | FOMC Meetings with S.E.P. | ||

| 09/12/2025 | 0001/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 09/12/2025 | 0330/1430 | *** | RBA Rate Decision |