IRAN: Ministry Source Denies Iranian Intelligence Reached Out to CIA

"*IRAN DENIES INTELLIGENCE MINISTRY REACHED OUT TO CIA FOR TALKS" - bbg

- That's in response to earlier NYT piece that cited sources in reporting Iranian intelligence had reached out to the CIA "to discuss terms for an end to the conflict".

- We noted earlier today that markets are beginning to look through official messaging from top-level Iranian, Israeli and US officials for clues on the duration of a conflict, and may instead prioritise source and off-the-record reports for a more effective gauge of the trajectory of the Iran instability: https://www.mnimarkets.com/articles/markets-look-for-clues-on-conflict-duration-as-messaging-stays-firm-1772634911818

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US JAN FINAL MANUF PMI 52.4 (51.9 FLASH, 51.8 DEC)

- MNI: US JAN FINAL MANUF PMI 52.4 (51.9 FLASH, 51.8 DEC)

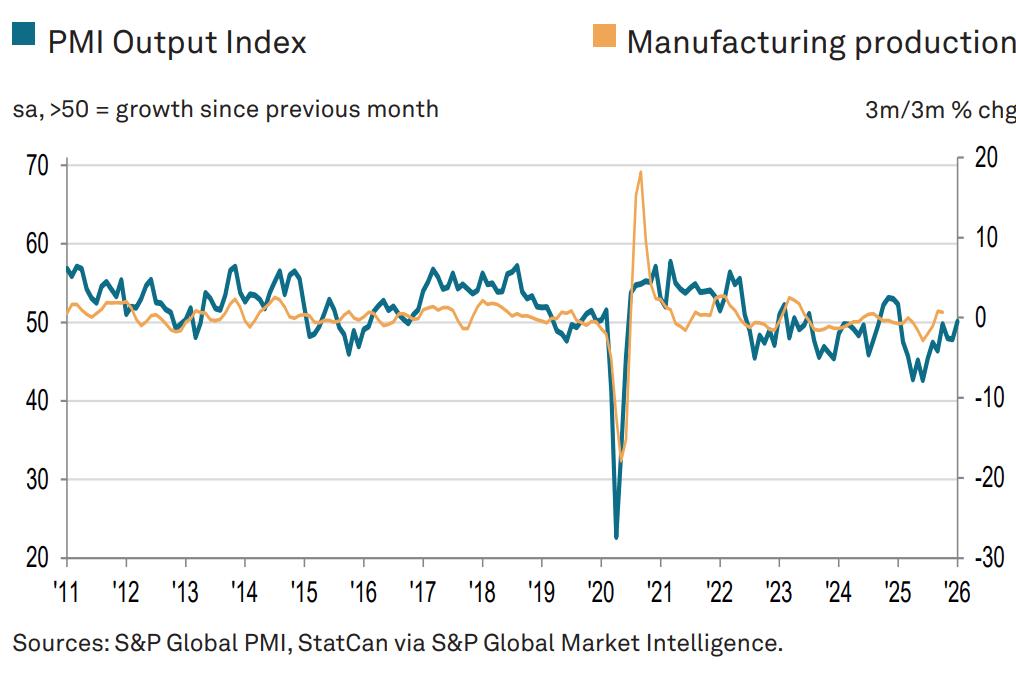

CANADA DATA: Best Manufacturing PMI In A Year Doesn't Dispel Stalling Narrative

Canadian manufacturing PMI jumped to 50.4 in January from 48.6 prior, in the strongest S&P Global report for the sector in a year. The signs under the surface weren't universally encouraging but at least the soft economic momentum evident in Q4 2025 doesn't look to have deteriorated at the start of 2026.

- Per the S&P Global report, trade tensions with the US and soft overall demand kept a lid on improvement: "Output stabilised and job numbers improved amid signs of an uplift in confidence amongst manufacturers about the future. Although new orders continued to fall, they did so only marginally and at the weakest rate in 12 months" though "exports fell again, especially to the neighbouring United States."

- On prices, while input costs accelerated to a 5-month high, passthrough effects appeared to be even more acute: "Tariffs ... underpinned a sharp rise in input costs and manufacturers responded to a further squeeze on margins by increasing their own charges to the greatest degree since March 2025."

- Overall economic expansion looks to have had weak momentum at the end of 2025, with the latest monthly GDP by industry data pointing to a Q4 contraction of 0.5% Q/Q SAAR which would be below the BOC's 0.0% estimate and down from 2.6% in Q3 (albeit the GDP by expenditure reading is lkely to be a little better).

- In any case there has been little evident momentum in the activity data and PMIs are pointing to flat output at best as opposed to a resurgence.

EQUITY TECHS: E-MINI S&P: (H6) Candle Patterns Highlight A Short-Term Bear Cycle

- RES 4: 7141.7 1.236 proj of the Dec 18 - Jan 13 - 21 price swing

- RES 3: 7100.00 Round number resistance

- RES 2: 7080.92 0.764 proj of the Nov 21 - Dec 11 - 18 price swing

- RES 1: 6965.75/7043.00 Intraday high / High Jan 28 and bull trigger

- PRICE: 6945.50 @ 14:25 GMT Feb 2

- SUP 1: 6864.50 Intraday low

- SUP 2: 6814.50 Low Jan 21 and the bear trigger

- SUP 3: 6771.50 Low Dec 18 and a key support

- SUP 4: 6684.50 Low Nov 24

The trend in S&P E-Minis is bullish and the pullback from last week’s high is considered corrective. However, note that a doji candle pattern on Jan 28 and a hammer candle on Jan 29, continues to signal scope for a deeper retracement near-term. Today’s initial move down reinforces the importance of these two patterns. A continuation lower would expose key S/T support at 6814.50, the Jan 21 low. The bull trigger is at 7043.00, the Jan 28 high.