IRAN: Markets Look for Clues on Conflict Duration as Messaging Stays Firm

Markets saw only a brief reaction to today's NYT piece that quoted sources in saying Iran had used back channels to offer to discuss terms for an end to the conflict - and public-facing messaging from all sides have strongly played down the odds of any near-term resolution. Even with this combative messaging, markets will be looking for any softer tones or further source reports to gauge the duration of the conflict (and thereby the persistence of high energy prices), rather than headlines

Official comments on conflict duration:

- US Sec. of War Hegseth (Weds): More, larger waves are coming, the US is just getting started. Will take all the time [we] need. It could take 4 weeks, it could take 8 or 3.

- US President Trump (Mon): We haven't even started hitting them hard, the big waves haven't even happened. The big one is coming soon.

- Senior Israeli IDF sources (Weds): Two more weeks of bombings across Iran ahead of us, with the plan being to attack thousands of targets

- Iran IRGC spokesman (Weds): Attacks will intensify in the coming days, will strike US and Israeli assets with "greater intensity" in the coming days

- US General Caine (Weds): Operation is complex, dangerous and "far from over"

Unofficial comments on conflict duration:

- NYT sources: US officials either Trump or Iran ready for offramp - at least in short-term. Offer raises questions about whether any Iranian officials could put in place a ceasefire with Tehran gov so unstable

- BBG sources: UAE, Qatar privately lobbying allies for help persuading Trump to reach an offramp, keeping military operations short

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: E-minis Off Lows Ahead Of Wall St. Open, Tech Eyed

E-minis comfortably off lows into the open as wider risk appetite recovers from Asia-Pac lows, tech still lags.

- S&P 500 e-minis: -0.30%

- NASDAQ 100 e-minis: -0.55%

- DJIA e-minis: +0.05%

- Note that bears were unable to test the bear trigger at the Jan 21 low in S&P 500 e-minis (6,814.50) before the bounce,

- Initial pre-market weakness for Oracle has more than reversed (last indicated over 3% higher). Initial weakness came after the company announced that it plans to raise $45-50bln via a mix of debt and equity as it looks to expand its cloud infrastructure business in a bid to strengthen its AI offering. Phased nature of any equity offering (may sell up to $20bln of common stock from “time to time”) may have helped the space off lows, along with indications of solid demand for the debt financing portion.

- Elsewhere, reaction to Nvidia CEO Huang noting that the company’s proposed $100 billion investment in OpenAI was “never a commitment” and that Nvidia would consider any funding rounds “one at a time” will be eyed. Nvidia indicated 1.6% lower pre-market.

- Tech name Palantir will report after hours.

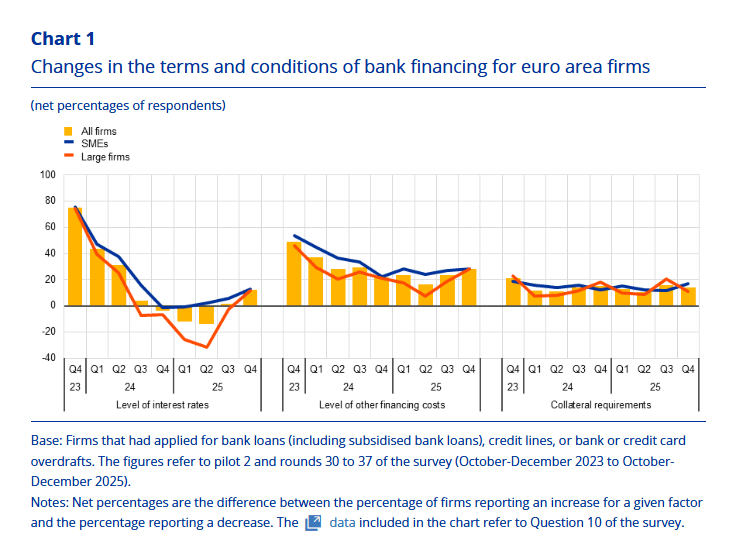

EUROZONE DATA: SAFE Indicates A Net Tightening Of Financing Conditions In Q4

The ECB’s Q4 Survey on the Access to Finance of Enterprises (SAFE) indicated a perceived net tightening of financing conditions from the perspective of Euro area firms. The results will need to be interpreted alongside tomorrow’s Bank Lending Survey, which will provide an update on lending conditions from the perspective of banks.

- These surveys help inform the ECB’s assessment of the effectiveness of policy transmission, alongside providing credit-based growth signals. See our latest review of monthly credit data here

The SAFE press release noted that “euro area firms reported a net increase in interest rates on bank loans (net 12%, compared with 2% in the previous quarter….”a net 28% of firms (up from 23% in the previous quarter) observed increases in both other financing costs (i.e. charges, fees and commissions) and collateral requirements (net 14%, compared with 16% in the third quarter of 2025)”

- “In this survey round, firms reported a modest rise in their need for bank loans (net 3%, up from 0% in the third quarter of 2025), accompanied by a small perceived decline in availability (net -2%, compared with -1% in the third quarter)”.

- “Firms continued to perceive the general economic outlook to be the main factor constraining the availability of external financing (net 20%, compared with 19% in the previous survey round) and indicated a slight improvement in banks’ willingness to lend (net 4%, up from 2%).”

Summarising non-credit focused questions from the survey:

- “Firms’ expected their selling prices to rise by 2.9% on average over the next 12 months (similar to the previous survey round), while the corresponding figure for wages was 3.1% (up from 3% in the previous round)”

- “Firms’ inflation expectations were broadly unchanged over all horizons”…“For the five-year horizon, most firms continued to indicate that risks to the inflation outlook were tilted to the upside (net 56%, up from 53% in the previous round).”

- "In this survey round, firms were asked about their use of artificial intelligence (AI). Results show that 27% of euro area firms do not use AI, 33% use it very infrequently, 31% moderately and 7% significantly"

US TSY FUTURES: BLOCK, Mar'26 10Y Sale

- -5,000 TYH6 111-25. sell through 111-26.5 post time bid at 0858:00ET, DV01 $328,000.

- the 10Y contract trades 111-24.5 last (-2).