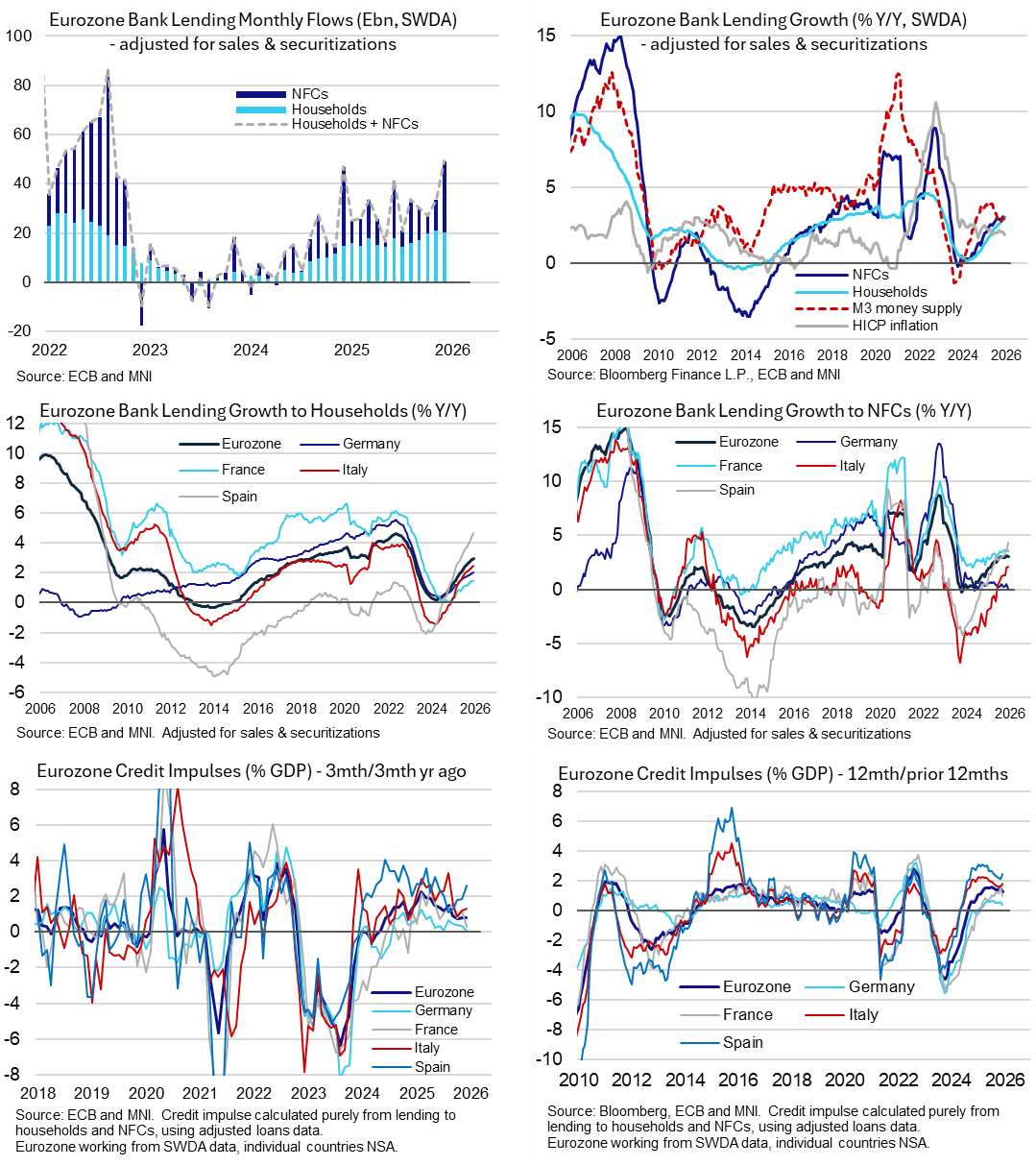

EUROZONE DATA: Strong Monthly Credit Flows In Dec Don’t Alter Credit Impulse

Jan-29 16:41

Eurozone lending to the private sector saw strong monthly flows in December although it didn’t materially credit impulse metrics which have stabilized in recent months after cooling from early 2025. Y/Y growth rates were similar to last month but that includes a further push higher to recent highs for household lending. Country discrepancies remain wide, especially for NFCs with Spain at 4.3% Y/Y and Germany at just 0.1% Y/Y.

- Lending flows to Eurozone households and non-financial corporates were strong in December, rising E49.3bn in working day and seasonally adjusted terms and also adjusting for sales & securitization.

- It follows an upward revised E33.6bn in Nov and is the largest admittedly nominal monthly increase since mid-2022.

- Flows to NFCs were strong (E29.2bn, highest since Dec 2024, after E12.7bn in Nov) whilst households were solid at E20.0bn after E20.9bn in Nov.

- Despite the strong monthly flows, annual growth rates were little changed, with NFCs at 3.0% after 3.1% Y/Y, households at 3.0% after 2.9% Y/Y and the combination unchanged at 3.0% Y/Y at its fastest since Apr 2023.

- Credit impulse metrics meanwhile were slightly softer to unchanged. The slow-moving 12 months on 12 months dipped to 1.3% GDP after 1.5% in Nov for its slowest since Feb 2025. Our preferred 3mths on 3mths a year ago held at 0.8% GDP, having broadly plateaued since September after cooling from a high of ~2% GDP in 1Q25.

- Lending Y/Y growth rates by country, for NFCs: Spain 4.3% after 3.5% (highest since early 2021), France 3.5% after 3.7%, Italy 2.1% after 2.0% and Germany 0.1% after 0.5% (lowest since mid-2024).

- For households: Spain 4.6% after 4.4% (highest since late 2008), Italy 2.5% after 2.3% (highest since early 2023), Germany 2.0% after 1.9% (technically highest since mid-2023), France 1.5% after 1.4% (highest since late 2023).

- Finally, M3 money supply growth has softer than expected in December at 2.8% Y/Y (cons 3.0) as it reversed a two-tenths increase in Nov. It averaged 2.9% Y/Y through 2H25 after 3.8% in 1H25, 3.2% in 2H24 and 1.1% in 1H24.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Mar'26 10Y Buy

Dec-30 16:33

- +10,000 TYH6 112-21, DV01 $670,100.

- The 10Y contract trades 112-23 last (+0.0+ vs. 112-25.5 early overnight high

US TSY FUTURES: BLOCK: Large Mar'26 5Y Sale

Dec-30 16:20

- -25,000 FVH6 109-12.5, sell through 109-12.75 post time bid at 1041:01ET, DV01 $1,099,000.

- The 5Y contract has since rebounded, trades 109-14.5 last.

FED: Permanent FOMC Voters Lean More Dovish (2/2)

Dec-30 16:09

As for the 8 permanent voting members of the FOMC, we haven't heard from many of them since the December meeting (just 3) but we continue to believe they are the driving force behind signaling further cuts.

- Gov Waller, currently one of the most dovish FOMC members, said on Dec 17 that his 2026 rate dot submission was below the FOMC median (of 3.4%) at "about three", saying "maybe we're 50 to 100 basis points off of neutral. We still got some room" to ease. But "We're not seeing a dramatic decline of labor market going off a cliff...I don't think we have to do anything dramatic. If you have to do something dramatic, it's too late."

- After dissenting in favor of 50bp cuts at each of the last 3 meetings, Gov Miran said on Dec 22 he hasn't decided on whether to push for a 25bp or 50bp cut at the January meeting - he "could see voting for" 25 given that with rates having come down 75bp at the last 3 meetings "the need for me to dissent for 50 becomes less", but "I do think it's important we continue steadily reducing the policy rate". Of course, that could be Miran's last meeting if he is replaced after his term ends at the end of January.

- NY Fed Pres Williams - who recall reignited December rate cut pricing in a speech he gave in November signalling unusually clearly that he saw room for a further cut in the "near term" - said on Dec 19 that “I don’t personally have a sense of urgency to need to act further on monetary policy right now because I think the cuts we’ve made have positioned us really well."

- The latest major data reports have been downplayed as factors driving monetary policy thinking, with Williams noting that the latest soft CPI print as well as the tickup in the unemployment rate in November were distorted by technical factors.

- We haven't heard since the December meeting from Chair Powell, Gov Barr, Gov Bowman, Gov Cook, or Gov Jefferson. Four of those five (Barr being the exception) are more dovish leaning than the Committee as a whole.

- We use the term "permanent" to describe these 8 voters only in terms of their positions: three may not be voting too much longer including Powell (term as Chair ends in May, after which he may resign from the Board), Cook (Supreme Court hearing on Jan 21 over the White House's attempt to fire her), and Gov Miran.