MEXICO: Minimal Changes Shown in Latest Citi Survey

"*MEXICO 2025 GDP GROWTH AT 0.4% VS PREVIOUS 0.5%

*MEXICO 2026 GDP GROWTH AT 1.3% VS PREVIOUS 1.4%

*MEXICO 2025 EXCHANGE RATE TO STAND AT MXN18.51/USD

*MEXICO 2026 CPI SEEN AT 3.95% VS PREVIOUS 3.91%

*MEXICO 2025 CPI SEEN AT 3.79% VS PREVIOUS 3.77%: CITI SURVEY" - Bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

COMMODITIES: WTI Slides, Precious Metals Rebound

- WTI has drifted lower in US hours but continues to hold broadly within the range seen since Oct 23 as supply outlooks remain in focus. US crude stocks saw their largest weekly increase since July.

- WTI Dec 25 is down by 1.5% at $59.6/bbl.

- US crude inventories for the week to Oct 24 built by 5.2mbbl compared to a Bloomberg survey expectation of a 0.25mbbl draw, but roughly in line with the API build of 6.5mbbl.

- WTI futures remain in a corrective cycle for now. First key support and the bear trigger is unchanged at $55.96, the Oct 20 low.

- On the upside, a clear move through initial resistance at $62.59, the Oct 24 high, would expose key resistance at $65.77, the Sep 26 high.

- Elsewhere, precious metals have rebounded today, with spot gold rising by 1.4% to $3,987/oz and silver by 2.2% to $48.2/oz.

- From a technical standpoint, the retracement in gold since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3,871.9.

- Initial resistance is at $4,161.4, the Oct 22 high.

- For silver, trend signals remain bullish, with initial resistance at $49.456, the Oct 23 high.

- Support to watch lies at the 50-day EMA, at $46.171.

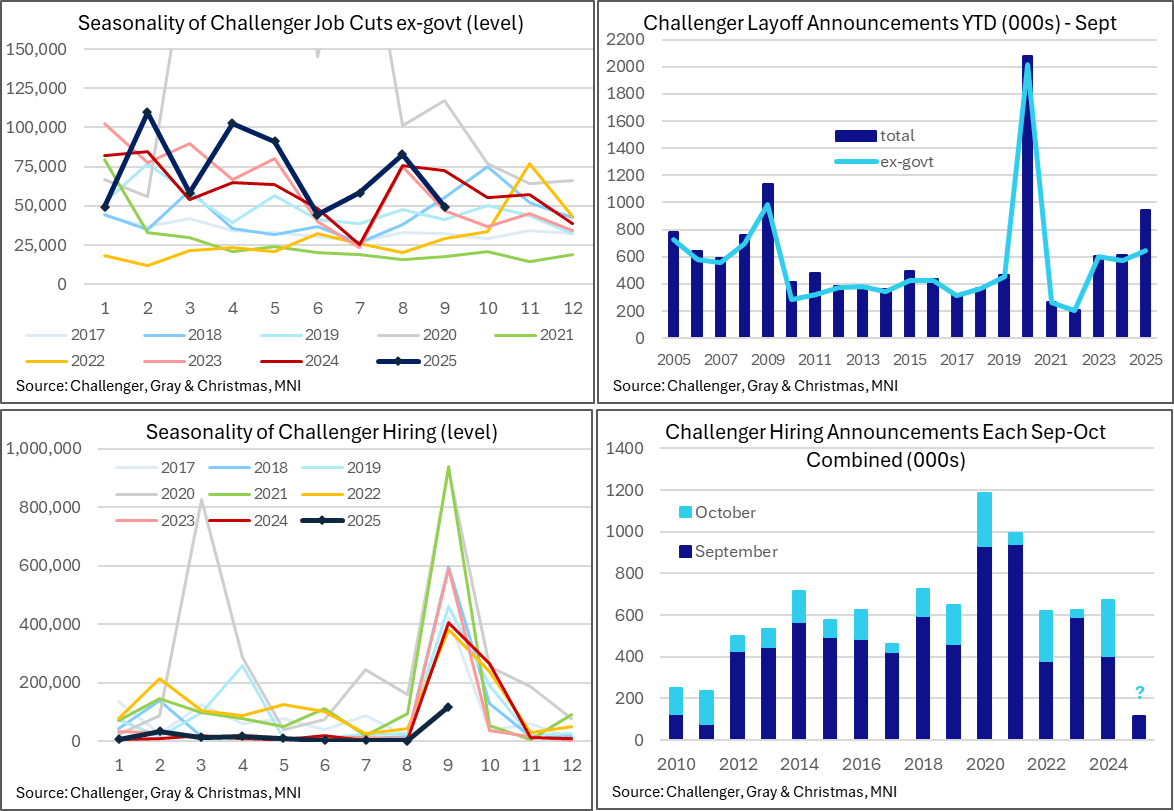

US PREVIEW: Challenger (Oct): Both Layoffs and Weak Hiring Plans Watched Closely

Tomorrow’s Challenger report for October (released 0730ET) will likely see greater attention than usual, with its timely look at layoff announcements but also being a key month for assessing seasonal hiring plans after a particularly weak September.

- Layoffs encouragingly fell 26% Y/Y in last month’s report for September, the largest decline since January, albeit flattered by an unusually high Sep 2024.

- Looking in trend terms, layoffs have summed to 946k in the year to September, a 337k or 55% increase compared to a year ago although that is of course heavily driven by federal government layoffs under DOGE efforts earlier this year.

- Strip out government roles to get a better sense of underlying labor market trends and cumulative layoffs sum to 647k for a 75k or 13% increase after 572k in the 2024 period, or less so when compared to the 603k in the 2023 period.

- Hiring plans were extremely low however in the key September month, at just 117k vs 404k last year. There should be a 250k contribution from Amazon in tomorrow’s October data although that was also the case in Oct 2024, i.e. the timing of Amazon plans wasn’t behind September’s weak reading. Rather, anecdotal evidence points to broader hiring lethargy, with Target for instance in 2024 announcing 100k of seasonal workers (as has been the case since 2021) but this year it has in part instead offered additional hours to its current employees.

- Indeed, Challenger has warned that it projects retailers “may add under 500k positions in the last three months of 2024, marking the smallest seasonal gain in 16 years”. Retailers added 543k jobs in 4Q24, down nearly 4% from 2023.

- Chicago Fed’s Goolsbee, a ’25 voter typically at the dovish end of the FOMC spectrum but who has also been recently cautioning on still stubborn inflation, recently spoke on how there hasn’t been a big spike in layoffs but equally that it’s against a low hiring rate. “If you look over the last 12 months, the unemployment rate has not been going up. We haven't seen a big uptick in layoffs, which, if this were the beginning of recession or deterioration of the labor market, that was rapid, you would expect to see higher layoffs or firing and we haven't seen that. There's still concerns on that side. I'm not decided going into the next meeting. I want to see how things are playing out. I do think the public announcements of layoffs you would expect, if that is an immediate business cycle-driven matter that you would start to see an uptick in the official unemployment insurance statistics or the layoff statistics, or you would get WARN Act type data of that form that would give you a little bit of a heads up of what was coming in the job market. I do think the hiring rate is low. That's among the weakest things in the economy at the moment”.

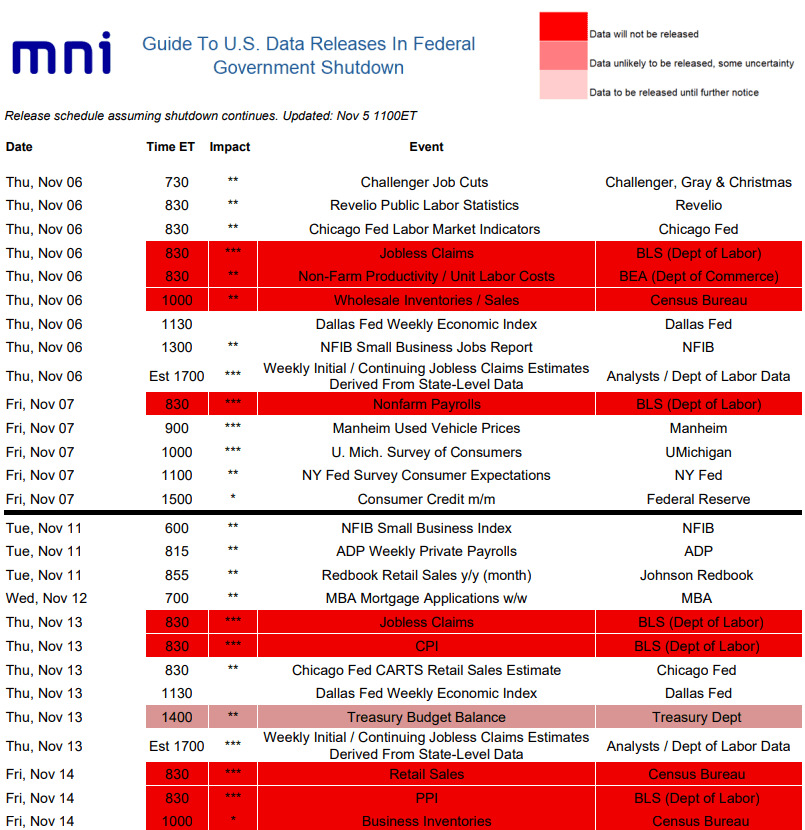

US DATA: MNI's Nov 6-21 Guide To US Data Releases In Federal Government Shutdown

With the federal government shutdown set as it stands to run at least into next week (about 65% implied probability per prediction markets that it will extend to at least Nov 12), here is MNI's updated guide to US data releases up through November 21:

- The near-term focus is clearly on labor market data, even with Friday's nonfarm payrolls report for October postponed indefinitely. We got ADP private payrolls today, with Thursday bringing Challenger Job Cuts, Revelio Public Labor Statistics, and the Chicago Fed's final estimate of October unemployment. Later in Thursday's session we should get the NFIB's small business jobs report, while we will as usual derive the national jobless claims numbers from the state-level data.

- Without Friday's payrolls data, the schedule includes largely consumer survey-focused reports: Manheim used vehicle prices, UMichigan prelim November survey, NY Fed consumer expectations, and the Fed's consumer credit data (for September).

- Next week's schedule includes CPI, Retail Sales, and PPI - but it's unclear whether these would be published on time (if at all) even if the federal government were to open imminently. That leaves a fairly thin data slate including the NFIB survey and Chicago Fed CARTS retail sales estimate (with possibility of a Treasury fiscal statement for October), as well as the usual weekly indicators (ADP, Redbook, MBA mortgage applications, Dallas Fed WEI, state jobless claims).