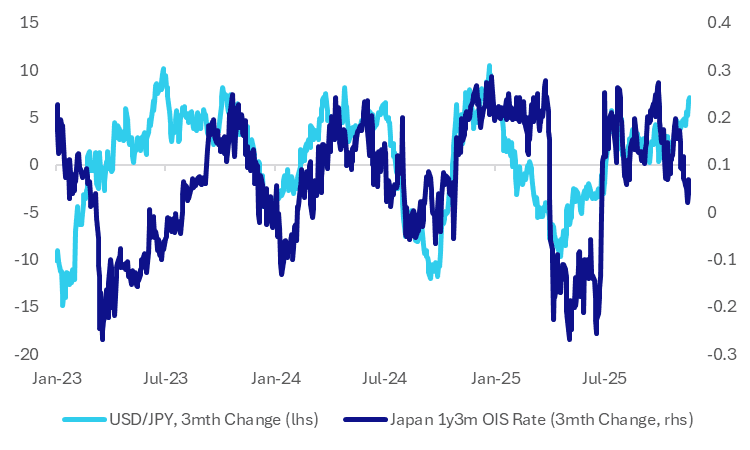

BOJ: Market BoJ Pricing Outlook & USD/JPY Gains Diverging

The weaker yen trend remains a key focus point for Japan policy makers. Earlier the FinMin stated that FX intervention was an option, a clear step up in rhetoric around yen weakness. BoJ Governor Ueda was also before parliament and warned that the weak yen could raise import costs and domestic prices, ultimately putting upward pressure on consumer prices. The chart below plots the 3 month rate of change in spot USD/JPY and the 3 month change in the 3 month OIS rate (1yr forward) as a proxy for the markets monetary policy outlook. The relationship has diverged somewhat recently, with little change in the 3mth rate of change in the policy proxy despite the break higher in USD/JPY. All else equal if USD/JPY continues to track higher risks, are likely to build around markets pricing in higher rates.

- There are a number of caveats of course. The new Takaichi regime is leaning against tighter BoJ expectations. The FinMin stated earlier that Japan is still halfway to achieving its sustainable, stable price goal (accompanied by wage gains). Katayama added that she understands the BOJ agrees with this assessment.

- Still, near term push back on BoJ rate hikes may drive the market to feel the central bank is at risk of falling further behind the curve. It may then price in more catch up later on.

- The other factor is that the market may not feel that policy rates are likely to go much beyond 1%. The 3mth rate 1yr forward OIS is currently 0.98% and this year we have spent little time above 1%.

- Such assessments could change though once we get a clearer picture of the new stimulus package the government is expected to announce soon. From late yesterday via BBG: Japanese Prime Minister Sanae Takaichi is set to unveil an economic package funded by an extra budget about 27% bigger than what was pledged in her predecessor’s spending plan a year ago, underscoring her commitment to an expansive fiscal policy.

Fig 1: Japan BoJ OIS Market Pricing Outlook & USD/JPY - 3 month Changes

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA PRESS: Trade Tension Market Volatility Could Give Investors An Entry Point

CHINA PRESS: China-EU Economic Leaders Hold Call, Discuss Rare Earths

China’s Minister of Commerce Wang Wentao told European Commissioner for Trade and Economic Security Maroš Šefčovič that China remains committed to safeguarding the security and stability of global supply chains and has consistently facilitated the rare earth approval processes for EU enterprises, according to a statement on the Ministry of Commerce website. During a video conference between the two officials, Wang reiterated China’s firm opposition to the broadening of the concept of “national security” in relation to the Nexperia case in The Netherlands. Both sides agreed to convene a session of the China-EU Export Control Dialogue Mechanism in Brussels as soon as possible.

CHINA PRESS: China Needs New QFLP Reforms - Expert

China should introduce new Qualified Foreign Limited Partner (QFLP) regulation given that the mechanism now extends to mezzanine financing, distressed assets and real estate, according to Zhao Bingyin, equity partner at Zhong Lun (Shanghai) Law Firm. Speaking at a Lujiazui Financial Salon focused on deepening QFLP pilot reforms in Shanghai, Zhao said regulators should ease entry requirements for traditional equity investment while maintaining higher thresholds for asset-heavy sectors such as infrastructure and non-performing loans (NPLs). He also called for better alignment between QFLP and emerging initiatives, including real estate private funds and asset securitisation pilots. These improvements, Zhao added, would help ensure that Shanghai remains at the forefront of QFLP innovation nationwide.