CANADA DATA: Manufacturing Sales Fall Again In November Advance

Dec-24 14:40

Unusually released after monthly GDP data, the advance estimate for manufacturing sales points to another sizeable decline in November as it unwinds September strength, although with that prior strength still seeing solid momentum.

- Manufacturing sales are indicated to have slipped another -1.1% M/M in November according to the StatCan advance release, after -1.0% in Oct and 3.6% in Sep (all nominal figures).

- The press release notes that the “largest decreases were in the transportation equipment and food subsectors."

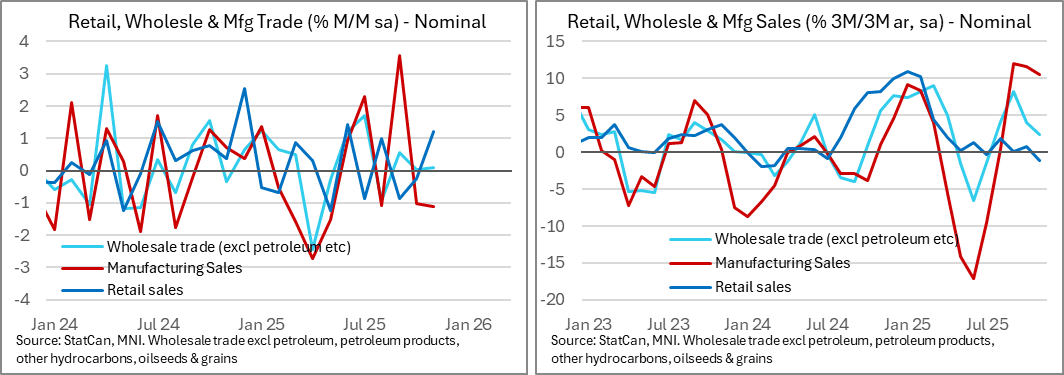

- Previous strong monthly increases still see the trend 3m/3m run rate at 10.5% annualized having peaked at 12% in September. Sales are recovering after sliding -17% annualized in June on the hit from US tariffs.

- This advance was calculated with a weighted response rate of 69%, typical for recent months (68.5% in Oct, 67.7% Sep, 68.2% Aug and 70% Jul). The average final response rate over the past twelve months has been 93%.

- It leaves manufacturing lagging other sales estimates specifically for November, with retail at a strong 1.2% M/M after a disappointing -0.2% in Oct and core wholesale at 0.1% M/M after an equally subdued 0.0%. It is however also running at a stronger recent trend but that’s after a period of heightened volatility – see charts.

- Yesterday’s monthly GDP report pointed to a somewhat tepid 0.1% M/M bounce in November after -0.3% in October (in real terms). StatCan had noted that downside in Nov came from “mining, quarrying, and oil and gas extraction and manufacturing”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: US Cash Opening Calls

Nov-24 14:25

SPX: 6,649.0 (+0.7%); DJIA: 46,383 (+0.3%/+137pts); NDX: 24,484.8 (+1.0%).

SOFR: Goldman Sachs Recommend SFRZ6/Z7 Steepener

Nov-24 14:23

Goldman Sachs think that the SFRZ6/Z7 spread offers attractive asymmetry and recommended initiating steepeners at 6.0 on Friday, targeting a move to 20.0, with a stop set at 0.0.

- They believe that “the widely anticipated September payrolls print did not offer the definitive answer that market participants were likely looking for. The lack of another NFP release before the December FOMC meeting leaves something on the table for both the doves and hawks on the committee, although we still view risks to the very front-end - including December - as skewed dovish versus current pricing given the continued softening in labor market slack measures and recent wobbles in risk sentiment”.

- Goldman note that “amid the lack of clarity, terminal rate pricing has remained steady around 3%, with forward gaps beyond 2026 at historically flat levels. weaker labor market activity could front-load cuts and take terminal rate pricing more firmly below 3% but keep forwards relatively stickier, while signs of reacceleration in underlying activity could see the market open up the right tail on forward rates”.

EGB OPTIONS: Bund upside Call Spread

Nov-24 14:21

RXH6 133/134.50cs, bought for 9.5 in 3k.