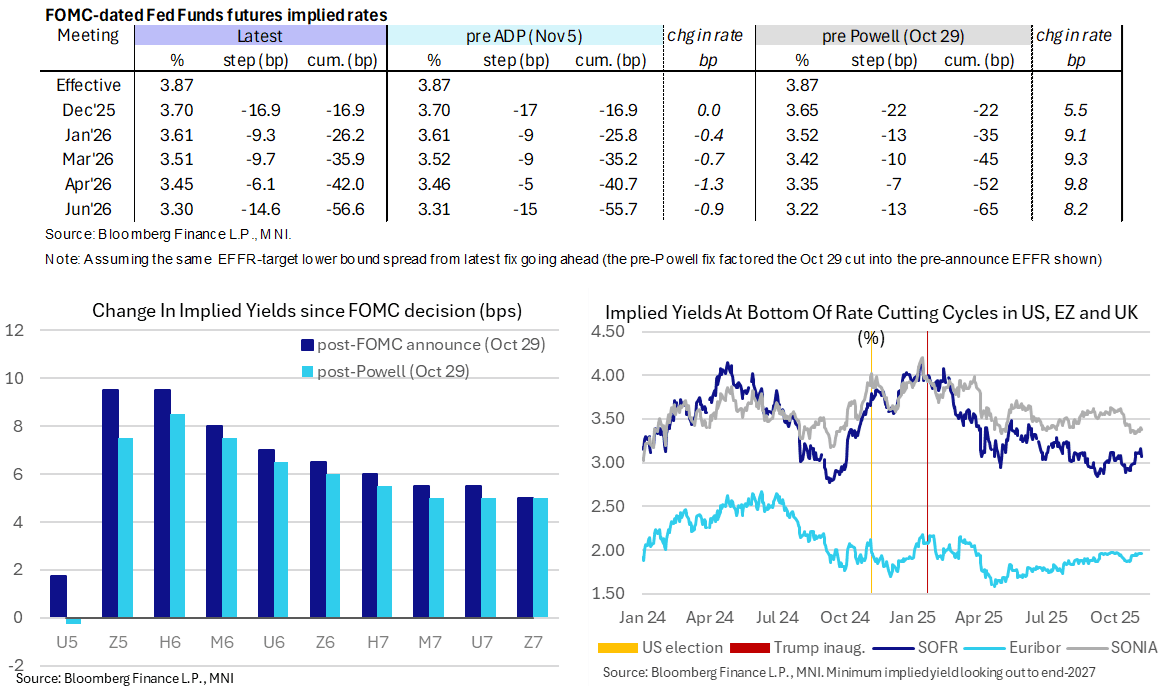

STIR: Lower Tier Labor Data Reverse Hawkish Shift on ADP and ISM Services

- US rates hold their sizeable rally on today’s softer labor data from Revelio Labs, Challenger and the Chicago Fed’s unemployment rate nowcast, in order of impact.

- Fed Funds implied rates are 2bp lower on the day for the Dec FOMC and up to 6bp lower for the Jun 2026 FOMC, fully reversing a hawkish shift yesterday on stronger than expected releases for ADP employment and more notably ISM Services- see below table.

- That said, the Dec FOMC still points to 5bp fewer cuts than priced prior to Powell last week and 8-10bp fewer cuts out to mid-2026.

- Cumulative cuts from 3.87% effective: 17bp Dec, 26bp Jan, 36bp Mar, 42bp Apr and 56.5bp Jun.

- SOFR futures have also reversed yesterday decline, ranging from +0.035 for the Z5 through to +0.085 for the Z7.

- The terminal yield of 3.075% (H7) is 8.5bp lower after a 6bp increase yesterday to 3.16% saw the highest close since late July.

- Still to come today, state-level jobless claims data later this afternoon (~1700ET), with the jump in layoffs in today’s Challenger jobs report for October dialling up sensitivity to increases in jobless claims figures. See: https://www.mnimarkets.com/articles/challenger-to-boost-sensitivity-to-jobless-claims-increases-1762426142486

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Bull Cycle Remains In Play

- RES 4: 0.6763 1.382 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 2: 0.6660/6707 High Sep 18 / 17 and key resistance

- RES 1: 0.6629 High Sep 30 & Oct 01

- PRICE: 0.6591 @ 16:45 BST Oct 7

- SUP 1: 0.6527/21 61.8% of the Aug 21 - Sep 17 bull leg / Low Sep 26

- SUP 2: 0.6484 76.4% retracement of the Aug 21 - Sep 17 bull leg

- SUP 3: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

The AUDUSD uptrend remains intact and the pair continues to trade closer to its recent highs. Support to watch lies at the 50-day EMA, at 0.6562. A clear break of this average would signal scope for a deeper retracement and expose 0.6527 once again, a Fibonacci retracement. For bulls, a stronger reversal higher would refocus attention on 0.6707, the Sep 17 high. Initial resistance to watch is 0.6629, the Sep 30 and Oct 1 high.

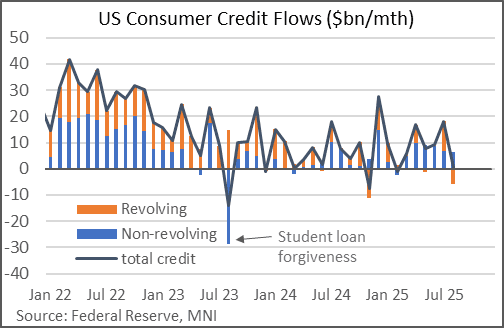

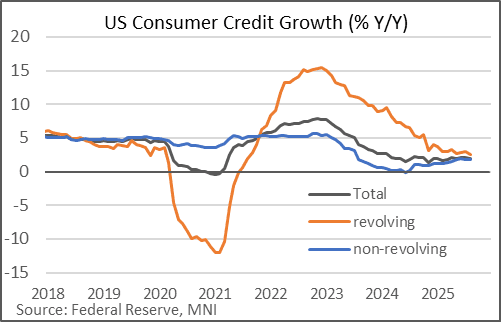

US DATA: Consumer Borrowing Slows, Not Major Tailwind For Consumption

The Fed's latest consumer credit report shows a sharp slowdown in the growth of total credit, to a 6-month low of $363M M/M (or 0.1% M/M). It was well below the $14.0B expected and follows July's $18.0B rise (4.3% M/M) gain, which was upwardly revised from $16.0B.

- The pullback was driven by a $6.0B drop in revolving credit outstanding, the biggest decline in 9 months, partially reversing a $11.2B rise in July. Non-revolving credit continued to rise steadily, by $2.3B (slowest in 4 months but around the prior 6-month average of $1.9B). Recall that revolving makes up 25% of overall consumer credit, largely made up of credit cards; nonrevolving credit is basically made up of student and auto loans.

- The month-to-month readings continue to be volatile but overall consumer credit is showing signs of steadying out, with Y/Y of 2.0% basically the same pace as the prior 4 months, albeit this belies a notable slowdown in revolving credit (2.6% in August weakest since Q3 2021).

- We wouldn't rush to conclusions from these data though overall it continues to appear that credit is not a strong tailwind to consumption.

- On a 3M/3M annualized basis, credit growth is running at 2.2%, which is not particularly impressive compared with nominal GDP rising roughly 6% in the quarter. It suggests a fairly limited credit impulse in terms of contribution to overall activity, versus a solidly positive set of readings in Q2.

US TSYS: Late SOFR/Treasury Option Roundup: Rate Cut Pricing Gains Slightly

Option desks report light SOFR/Treasury call option trade overnight, leaning towards low delta puts as the US Gov shutdown continues. Underlying Tsy futures firmer, off late session highs after climbing steadily off this morning's lows (TYZ5 112-09 low, September 28 level). Projected rate cut pricing has gained slightly vs. early morning levels (*): Oct'25 at -23.7bp (-23.1bp), Dec'25 at -45.1bp (-44.2bp), Jan'26 at -55.7bp (-54.6bp), Mar'26 at -66.4bp (-65.4bp).

- SOFR Options:

- +10,000 SFRZ5 96.62/96.75 call spds 0.5 ref 96.32

- +15,000 SFRZ5 96.62/96.68 call spds, cab vs. 96.30/0.05%

- Update, +12,500 SFRZ5 96.43/96.50/96.56 call flys, 0.25

- +15,000 SFRZ5 96.50/96.62 call spds, 1.0

- 1,000 SFRZ5 96.18/96.37/96.56 2x3x1 put flys

- +1,500 0QV5 96.87/97.06 strangles, 1.5 vs. 96.91/0.20%

- 1,750 0QV5 96.62/96.75/96.87 put flys, 0.5 vs. 96.955/0.08%

- +3,000 SFRZ5 96.50/96.62 call spds, 1

- -4,100 SFRV5 96.31 puts, 1.25 ref 96.315

- Treasury Options:

- 4,400 USZ5 115 puts, 51 ref 116-26

- -15,000 FVX5 108.5/110 call over risk reversals, 0.5

- 10,000 USX5 109 puts, 2 ref 116-17

- 2,000 FVX5/FVZ5 110 put spds

- 7,500 FVX5 110 calls 3, ref 109-05.5

- 3,225 TYX5/TYZ5 111/111.5 put spd spd

- +5,000 TYX5 112.5/113.5 call spds 7 over 111.25 put vs. 112-05.5/0.41%

- -1,000 TYX5 111.25/113.5 strangles, 11 vs. 112-07/0.02%

- -2,000 TYX5 112.5 calls, 24 vs. 112-12.5/0.44%

- 4,000 Tue/wkly 10Y 111.5 puts ref 112-11 (exp 10/14)

- -5,500 wk2 US 115 puts, 4 ref 116-07

- +1,000 wk3 FV 109.25/109.75 4x5 call spds, 27 vs. 109-04/0.92%

- -5,400 TYZ5 109.5 puts, 4 ref 112-14 to -14.5