JAPAN: Long Dated Yield Surge Continues, With Election Driving Uncertain Outlook

As Japan's upper house elections approach (held July 20), focus remains on the relentless rise in longer-dated JGB yields. The 30yr is up a further +4bps today, last around 3.21%. This is a fresh high on record (since it was debuted in 1999, per BBG). The 10yr JGB yield was last near 1.60% with the 20yr around 2.64%. Concerns around fiscal slippage is a factor in the JGB sell-off. The 2/30yr JGB curve is at +241bps, just off recent highs and near multi-decade highs

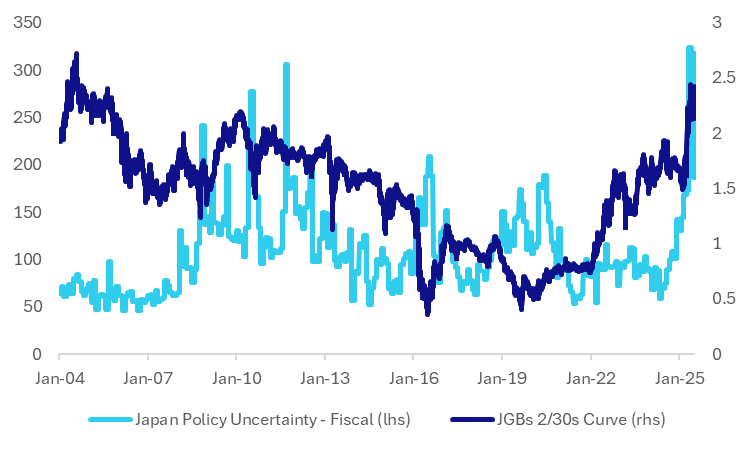

- The chart below plots the JGBs 2/30s curve against a policy uncertainty index, related to fiscal policy. June saw fiscal policy uncertainty edge down per this metric (which is a monthly indicator), but it remains elevated by historical standards. The index ticker on BBG is EPUCJNFP <Index>.

- To be sure, there are lots of episodes where the JGB curve has been steep, whilst fiscal policy uncertainty is low. However, at the moment, the correlations between the two series are running at close to 80% (using the last 12 months as a sample window).

- A number of onshore media outlet are reporting that the ruling coalition is at risk of losing its majority with the upper house elections, helping fuel fiscal policy uncertainty, but with a skew towards a stronger fiscal impulse going forward.

- Rtrs adds: "All three of the leading opposition parties espouse some form of consumption tax cuts, with the populist, right-wing Sanseito party proposing a phasing out of VAT altogether. The policy has gained sway with the public as well: a recent poll by the Asahi newspaper showed 68% of voters thought a sales tax cut was the best way to cushion the blow from rising living costs."

- It quotes analysis from Barclays: "Barclays calculates that the rise in 30yr yields currently factors in about a three percentage-point cut to Japan's 10% consumption tax rate. "Even if the ruling parties retain their majority in the upper house, they would still be unable to pass budget bills, including the upcoming supplementary budget, without the cooperation of the opposition parties."

- Japan PM Ishiba has favoured cash handouts to provide cost-of-living relief so far, but it remains to be seen if this is sustained post the election result.

- Note on July 23rd we have 40y debt auction, as potentially the first litmus test after the election result.

Fig 1: JGBs 2/30yr Curve & Fiscal Policy Uncertainty Index

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US FISCAL: Available Extraordinary Measures Pick Up Ahead Of Tax Date

Treasury had $144B in "extraordinary measures" available to keep the government financed as of June 11 per a release Friday. That is up from $84B a week earlier and the highest since April 28.

- However, TGA cash continues to fall, to $309B latest (lowest since early April) Combined with a pullback in Treasury cash ($376B), keeping the total resources available to avert an "x-date" in the summer at around $450B .

- There will be another uptick in Treasury cash in the coming days, and it's likely Treasury allowed some of the extraordinary measures to be rebuilt (ie not exercised) in anticipation of more cash coming in.

- This is likely to be the last major uplift before the summer at which point x-date speculation will pick up if Congress hasn't passed a debt limit increase by then.

FED: Two Cuts Priced This Year Headed Into FOMC Week

As we head into the June Fed meeting week, market pricing is reflective of the FOMC’s messaging (that we describe in our preview):

- The next cut is only fully priced by the October FOMC meeting, with September seeing a roughly 80% implied probability of bringing the next 25bp reduction.

- Exactly 50bp of cuts are priced through end-2025, implying two Q4 cuts.

- That’s a shift from just after the May meeting, after which the next cut was fully priced by September, and there were closer to three cuts priced for the rest of the year.

- Overall cuts are seen backloaded this year (after 15bp in September, 29bp of cuts priced in Q4 - Oct/Dec combined), but falls off in Q1 (just 21bp cuts priced, 9bp of cuts priced for January and 12bp for March)

FED: Summary Of Economic Projections: Higher 2025 Inflation, Weaker Growth

The MNI Markets Team’s expectations for the updated Economic Projections are below.

- As of the May meeting, the Federal Reserve staff – whose outlook tends to be broadly shared by the median Committee member – revised their forecasts for growth weaker in 2025 and 2026, “as announced trade policies implied a larger drag on real activity relative to the policies that the staff had assumed in their previous forecast. Trade policies were also expected to lead to slower productivity growth and therefore to reduce potential GDP growth over the next few years. With the drag on demand expected to start earlier and to be larger than the supply response, the output gap was projected to widen significantly over the forecast period. The labor market was expected to weaken substantially, with the unemployment rate forecast moving above the staff's estimate of its natural rate by the end of this year and remaining above the natural rate through 2027."

- On inflation, "The staff's inflation projection was higher than the one prepared for the March meeting. Tariffs were expected to boost inflation markedly this year and to provide a smaller boost in 2026; after that, inflation was projected to decline to 2 percent by 2027."

- Our expectations for these changes fall somewhere in between those projections and the March SEP – a slightly higher unemployment rate, substantially higher inflation in 2025 but to a lesser extent in 2026, and weaker GDP growth this year. Longer-run variables should be unchanged.

MNI Markets Team Expectations For June 2025 Summary Of Economic Projections Medians