JAPAN DATA: Local Investors Buy Offshore Equities & Bonds

Japan outbound investment flows were positive in the week ending Sep 5. We saw a second consecutive week of net buying in the offshore bond space, albeit at a more modest pace compared to the previous week. This is consistent with rising global bond returns, aided by rising Fed easing expectations amid softer data outcomes. Local investors also purchased offshore equities for the second straight week and in bigger size compared to the prior week. Again, similar factors may be in play, with global equity returns on the improve in recent weeks.

- In terms of inflows into Japan bonds/equities, offshore investors purchased a modest amount of local stocks. This ends a two week run of outflows in this space (which came after a long period of inflows).

- On the bond side, offshore investors sold local bonds. Rising yields, amid fiscal outlook concerns, may be tempering return expectations for offshore investors in this space.

Table 1: Japan Offshore Weekly Investment Flows

| Billion Yen | Week ending Sep 5 | Prior Week |

| Foreign Buying Japan Stocks | 108.6 | -785.7 |

| Foreign Buying Japan Bonds | -604.5 | 397.2 |

| Japan Buying Foreign Bonds | 245.1 | 1419.9 |

| Japan Buying Foreign Stocks | 891.1 | 481.8 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Malaysian Consecutive Outflow Days Stretch Back To July 25

Equity inflow momentum was mixed yesterday, with tech sensitive markets offering contrasting viewpoints. South Korea saw positive momentum, but Taiwan saw outflows. For Taiwan this followed very strong inflow momentum last Thursday, but since then momentum has stalled somewhat, albeit remaining positive for the 5-day rolling sum period. The Taiex looks to be establishing itself above the 24000 level. Recent data outcomes have been positive in terms of export growth for July up 42%y/y. The local authorities did note yesterday that if the current 20% tariff rate is maintained that growth could be cut by 0.1-0.36%.

- In South Korea, yesterday's inflows ended a run of two consecutive days of outflows. The past 5-days of inflows are running at a more modest +$500mn. Onshore media reported on stocks capital gain tax: "The official at Lee’s office told DongA that the current 5b won threshold is likely to be maintained as ruling party has stated its position" (see this link, via BBG for more details).

- Indian inflows returned at the end of last week but not enough to shift the 5-day rolling sum into positive territory.

- Indonesian inflows remained positive. In contrast, Malaysia saw further outflows, which now stretch back to July 25th in terms of consecutive outflow days seen. Still, the local Malaysian bourse has tracked higher since the start of August.

- Thailand markets were closed yesterday and return tomorrow.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 196 | 510 | -4859 |

| Taiwan (USDmn) | -153 | 1408 | 4419 |

| India (USDmn)* | 323 | -855 | -12028 |

| Indonesia (USDmn) | 52 | 122 | -3693 |

| Thailand (USDmn)* | 3 | 122 | -1696 |

| Malaysia (USDmn) | -24 | -243 | -3220 |

| Philippines (USDmn) | 7 | 12 | -617 |

| Total (USDmn) | 405 | 1075 | -21695 |

| * Data Up To Aug 8 |

Source: Bloomberg Finance L.P./MNI

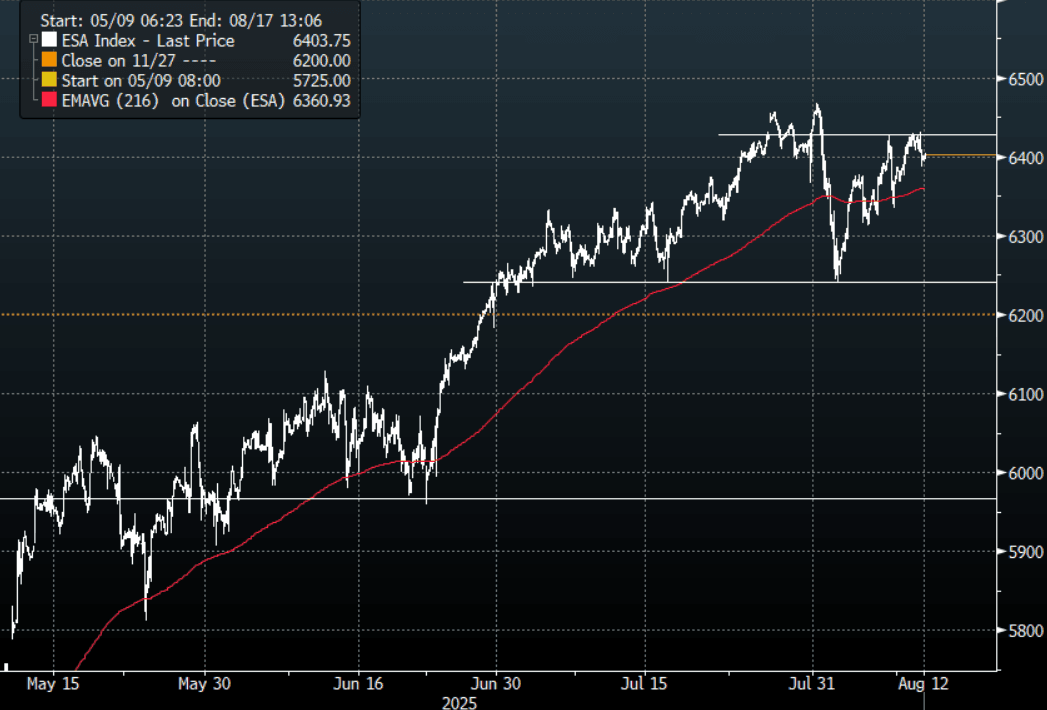

US STOCKS: S&P(ESU5) - Stalls Above 6400, Eyes CPI Tonight

The ESU5 overnight range was 6387.50 - 6431.50, Asia is currently trading around 6400. The ESU5 contract stalled around 6430 and drifted lower in the N/Y session as some risk was pared back going into the US CPI. This morning US futures have opened pretty muted, ESU5 +0.05%, NQU5 +0.06%. Price bounced strongly off its first support around 6200/6250, depending on what your view is I suspect bounces back towards 6450 should now find sellers initially as we enter a poor period based on seasonality. A break below 6200 is needed to potentially signal a deeper correction back to the 5900/6000 area. The price action in stocks continues to be bullish ignoring the headwinds that point to any possible retracement, let's see what CPI holds tonight.

- Guy Berger on X: “I’ll die on this hill: the net benefit (or cost) of the tariffs is more negative than you would get from naively applying a basic trade model because we are taxing imports of capital goods and other inputs into production (eg aluminum, steel, copper, etc). The “optimal tariff” argument and the “we need to produce key production inputs here” argument are at cross purposes with each other. The more you pursue one the more you will undermine the other.”

- Bloomberg - “CFRA’s Angelo Zino acknowledges the revenue tax on the chips(Nvidia & AMD) will have a negative impact on profit margins relating to China sales; re-entry into the market could be worth the cost. “We think the news opens up a host of other issues, as geopolitical uncertainty could change plans in place amid trade discussions and raises questions about whether it potentially creates a new precedent with other industries/trade partners,” Zino said.”

- Bloomberg - The dual force of Fed balance sheet runoff and the rebuilding of the Treasury’s general account is extracting liquidity from the financial system through multiple, compounding channels — and this will increasingly be a headwind to risk appetite

Fig 1: SPX(ESU5) 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Cash Open

TYU5 is trading 111-24+, down 0-04 from its close.

- The US 2-year yield opens around 3.766%.

- The US 10-year yield opens around 4.285%.

- MNI US CPI Preview: High Early Bar To September Fed Hold. The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- (Bloomberg) -- Treasuries snapped a three-day losing streak as investors prepare for fresh US inflation data that may help determine the Federal Reserve’s next move on interest-rate cuts.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- Data/Events: NFIB Small Business Optimism, CPI, Federal Budget Balance