EU CONSUMER CYCLICALS: Kering: a revisit to fundamentals

(KERFP; NR/BBB+ Neg)

With the two periphery concerns (those being Pinault/Artemis debt load and the Valentino acquisition) now going away we can shift focus back to what was - and still is - the core issue. To reiterate from 2Q earnings:

- There were no signs of a easing in sales falls for 3m to June. It said in July, Gucci improved slightly (Q2: -25%), Saint Laurent stayed similar (-10%) while Bottega (+1%) is expected to slow in 3Q ahead of launches planned instead in 4Q.

- The impressive part of the 1H results was the cost discipline with Opex down -11%. It is guiding up to HSD fall over the FY and is also keeping a lid on capex (at <€1b).

Still net of the above and accounting for other guidance (incl. gross margin) we see FY25:

- EBITDA -20% y/y

- continuing FCF (net of leases but before RE transactions) falling from €1.9b to €0.9b

- continuing FCF net of dividends at €0.15b

- Leverage moving from net 3.8x last year to 4.3x without any additional RE disposals

The offset for credit comes from large non-core property/RE disposals. It has done €1.3b already but is expecting another €1.7b in near future. If the additional €1.7b comes this year it will offset earnings pressure in full leaving leverage unch at 3.8x. This will still leave it above rating threshold of 3.5x, but S&P will likely give it breathing room if it shows signs of stabilising sales.

On RV, we see credit becoming complacent again (heading through non-cyclical BBB French names). A rally heading into earnings has historically not ended well and we are not sure if the 3Q - which will not see the impact of new Gucci Creative Director or tangible impacts from the new CEO - will deliver what credit is keen to price already. Please keep in mind it's room to take a third consecutive year of double digit revenue falls (in 2026) without FCF turning negative is limited.

Supporting credit is a +50% rally from lows in equities - at 40x earnings they are pricing growth ahead.

3Q results come in a month (23-Oct).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Aug14 $1.1590-00(E1.8bln), $1.1625-35(E898mln), $1.1645-50(E1.2bln), $1.1695-00(E4.5bln); Aug15 $1.1590-00(E1.1bln); Aug18 $1.1560(E1.1bln)

- USD/JPY: Aug14 Y147.00-20($1.2bln), Y148.15-30($945mln), Y155.00(Y1.6bln

- GBP/USD: Aug14 $1.2975-00(Gbp1.2bln)

- EUR/GBP: Aug14 Gbp0.8690-05(E1.1bln)

- AUD/USD: Aug14 $0.6600(A$1.3bln)

- USD/CNY: Aug15 Cny7.5000($1.7bln)

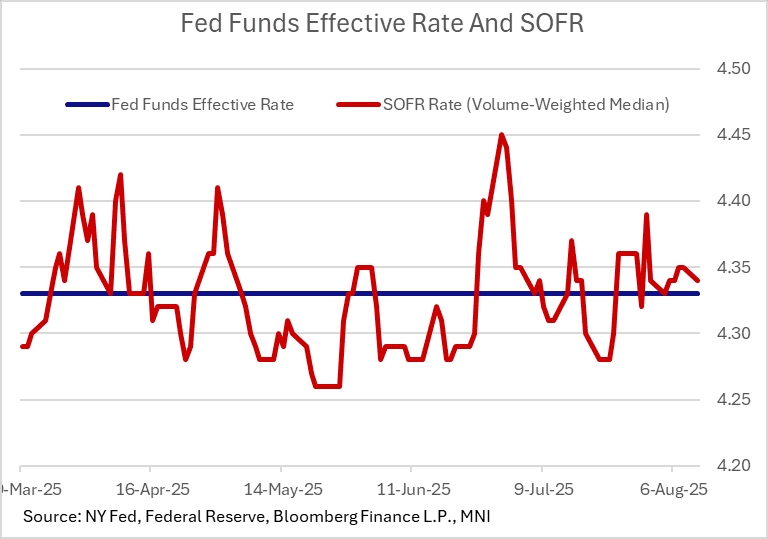

US TSYS/OVERNIGHT REPO: SOFR Softens Slightly, Potential Pickup Ahead

Secured rates were a little softer Monday as was broadly expected, with SOFR edging 1bp lower to 4.34%. Other major secured rates and effective Fed funds were unchanged.

- As we noted yesterday, pressure could pick up later in the week on Treasury auction settlements. These include $55B in net cash raised by bills today, and a further $42B on Thursday, followed by $35B in coupon settlements Friday.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.34%, -0.01%, $2796B

* Broad General Collateral Rate (BGCR): 4.33%, no change, $1173B

* Tri-Party General Collateral Rate (TGCR): 4.33%, no change, $1137B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $115B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $263B

US: BLS Commissioner Nominee Antoni Suggests Suspending Monthly Payrolls Report

Fox Business has published an interview with E.J. Antoni in which the White House's nominee as the next Bureau of Labor Statistics commissioner suggests that the monthly Employment Situation (ie nonfarm payrolls) report should be "suspended":

- "Until it is corrected, the BLS should suspend issuing the monthly job reports but keep publishing the more accurate, though less timely, quarterly data... Major decision-makers from Wall Street to D.C. rely on these numbers, and a lack of confidence in the data has far-reaching consequences."

- He adds: "How on earth are businesses supposed to plan – or how is the Fed supposed to conduct monetary policy – when they don’t know how many jobs are being added or lost in our economy? It’s a serious problem that needs to be fixed immediately."

- This interview was conducted on Monday, before Antoni's nomination by the President. Though it's notable he "told FOX Business that he doesn’t believe the jobs data was intentionally manipulated, as some have suggested, but instead argues that persistent flaws in the Bureau of Labor Statistics' methodology have gone unaddressed."