CANADA DATA: July PMIs Add To Evidence Of Activity Improving After Weak Q2

Aug-06 13:48

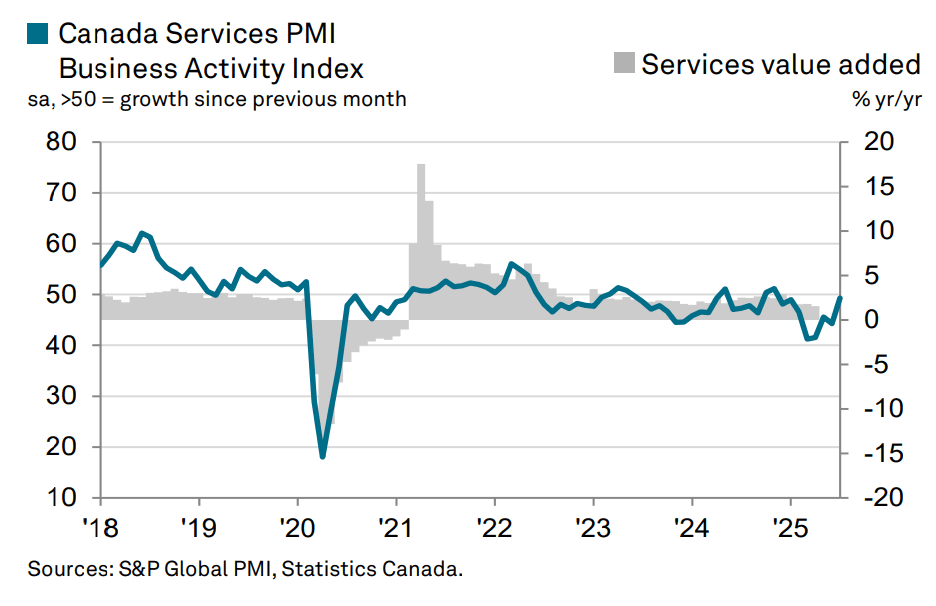

July's Canada Services PMI report was upbeat by recent standards, and one that is suggestive of economic activity having troughed in Q2 in line with expectations and the Bank of Canada's latest Monetary Policy Report projections.

- Weakness persisted in July but was not as acute as it was in the depths of the summer (49.3, below the 50.0 expansionary mark for an 8th consecutive month but the highest since November 2024 and up from 44.3 prior and 41.2 in March).

- Some highlights from the S&P Global report:

- "There were tentative signs of recovery in the Canadian services sector as the second half of the year got underway. Business activity neared stabilisation amid a further slowdown in the pace of contraction in new orders, while business confidence improved. Companies also increased their staffing levels again...Demand also showed tentative signs of improvement, albeit with customers still reluctant to commit to new projects, particularly those in international markets."

- "The impact of US tariffs was again the main factor highlighted by those companies that saw a drop in output over the month. On the other hand, the start of new projects led some firms to record a rise in activity."

- "On the price front, both input costs and output prices rose at slower rates than seen in June."

- Note the Composite PMI index came in at 48.7 (44.0 prior), weighed down by Manufacturing (46.1).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RIKSBANK: Implied Probability of August Cut Down to 20% Following Flash CPI

Jul-07 13:37

- Even though today’s Swedish June flash inflation report saw a 0.4pp rounded upside surprise, analysts had expected volatile components to drive the Y/Y acceleration in CPIF ex-energy. If these components (e.g. package holidays) were the sole drivers of the June increase, it would significantly dampen the hawkish impact of the release.

- Meanwhile, the Riksbank’s June minutes portrayed an Executive Board that is more concerned about weak demand pulling inflation below target in the medium-term than known upside risks. In this light, Thursday’s May monthly activity data will be important to monitor (despite its volatile/revision-prone nature). Early consensus looks for monthly GDP to fall 0.2% M/M (three estimates ranging between -0.4% M/M and -0.2%; vs 0.4% prior).

- Markets now assign just a ~20% implied probability of a 25bp Riksbank cut on August 20 according to sell-side estimates. That’s down from a ~50% chance before the inflation data. 2-year SEK swap rates are also up 8.5bps to the highest since June 26.

- SEK has mostly consolidated this morning’s post-data strength and remains the G10 outperformer. EURSEK is down 0.85%, but initial support at the 20-day EMA of 11.1042 has not been tested. NOKSEK is down 0.9% at 0.9410, off lows of 0.9377.

- We haven't seen any sellside forecast changes following the inflation data, but there remains a split of opinions on the terminal rate:

- Handelsbanken continue to expect a cut in August.

- JP Morgan still see one more cut in September.

- Danske Bank forecast no more cuts, but note that “we still see some downside risk to our call”. DNB and Nordea also expect no more easing this cycle.

SONIA OPTIONS: Latest Call Flies Buyers

Jul-07 13:35

- SFIQ5 96.20/96.30/96.40c fly, bought for 1.5 in 15k total.

- SFIV5 96.10/96.20/96.30c fly, bought for 1.5 in 6k.

MNI EXCLUSIVE: EU Update On Trade Talks With U.S.

Jul-07 13:33

EU officials give an update on talks with the U.S. -- on MNI Policy MainWire now, for more details please contact sales@marketnews.com.