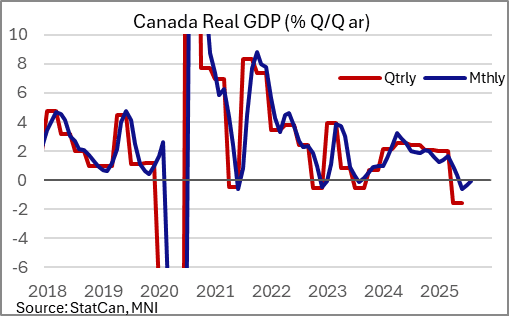

CANADA DATA: July GDP Beats Expectations, But Q3 Recovery Still Looks Tepid

Sep-26 15:13

Industry-level GDP came in at 0.2% M/M in July in real terms, exceeding the 0.1% expected by both consensus and StatCan's advance report, with growth looking to have flatlined in August.

- The unrounded growth of 0.24% M/M, thus nearly rounding up to 0.3%, made July's outturn even more impressive vs expectations. Steady/accelerating growth was seen in multiple industries in July: manufacturing (+0.7% after -1.5%), mining (+1.4% after +0.3%), public administration (+0.3% after +0.1%), wholesale trade (+0.6% after +0.6%) and real estate (+0.3% after +0.3%). As had been flagged by a separate report, retail (-1.0% after +1.5%) weakened while construction (+0.1% after +0.3%) slowed albeit remained positive.

- Looking ahead, the August advance estimate is for "essentially unchanged" GDP (StatCan: "Increases in wholesale trade and retail trade were offset by decreases in mining, quarrying, and oil and gas extraction, manufacturing, and transportation and warehousing").

- On a quarterly basis, that sectoral breakdown bodes ill. Wholesale trade continues to improve (-2.7% 3M/3M annualized rate of growth in July, after -6.1% in Jun) and an improvement in retail trade should see quarterly growth in that industry return to positive territory (-0.1% 3M/3M ann. in July, first negative reading in a year). But sectors including manufacturing and mining look set to remain in quarterly contraction (-6.5% and -3.2% in Jul, respectively), even after having contributed the most to GDP growth in July.

- Overall the economy looks to have begun to recover from the -1.6% Q/Q SAAR GDP print in Q2 but judging from the monthly data and estimates, as well as industry surveys, the Q3 growth rebound looks to remain tepid. Current Bloomberg consensus for Q3 growth is 0.5%, which looks close to the mark after these data and not far off the trajectory implied by the BOC's July MPR projections for a tepid H2 recovery.

- As such it shouldn't substantially impact the BOC's thinking on an end-October cut, which looks to be more dependent on the Labour Force Survey (Oct 10), BOC Business Outlook Survey (Oct 20), and CPI (Oct 21). That said, implied cut pricing receded to 10bp (40% chance of a cut) vs 12.5bp (50% chance of a cut) pre-data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Pivotal Significance for NZDUSD at 0.58, AUDNZD Reaches 6-Month Highs

Aug-27 15:11

- Weakness for the New Zealand dollar standing out across the G10 complex today, and despite the most recent bounce, spot has narrowed the gap to the pre-Powell lows overall, located at 0.5800.

- Friday’s low print adds to the medium-term significance of this level, which has proven an important pivot point dating back to late 2023. A break of the figure will be required for a deeper selloff, potentially targeting a move to 0.5728, the 61.8% retracement of the Apr/Jul rally.

- Firmer-than-expected Australian CPI data was largely shrugged off by the market, however, it has provided another boost for AUDNZD, which has extended its August rally to just under 2%. A break above 1.11 has placed the cross at fresh 6-month highs, placing renewed focus on key medium-term resistance at 1.1180.

- On the domestic calendar, monthly filled jobs data is scheduled early Thursday, before ANZ activity outlook, business and consumer confidence figures cross.

FOREX: EUR/AUD Breaks to New Daily Lows as AUD Benefits From Equity Strength

Aug-27 15:05

EUR/AUD breaking to new daily lows in recent trade (and through the WMR fix) - this puts the price clear of both the 50-dma at 1.7893 and likely avoids the formation of support at a possible uptrendline drawn off the February lows.

- Worth noting today marks month-end value date given Aug31st falls on a Sunday, so could tie-in some month-end flow to recent moves.

- Similarly, equities remain firm, helping aide AUD strength here: AUD/USD is back to flat, reversing the day's losses of ~0.4%.

ESM ISSUANCE: USD2bln WNG New 5-Year: Priced

Aug-27 14:58

- USD2bln WNG of the new 3.75% 5-year Sep-30 ESM-Bond

- Spread set earlier at SOFR MS+39 (SA 30/360) (guidance was SOFR+40 Area, IPT was MS+42 area, that was equiv. to CT5 + ~7.3bp)

- Books closed in excess of $13.3bn excl. JLM interest

- Reoffer 99.855 to yield 3.782%

- Issuer: European Stability Mechanism (TICKER: ESM)

- Issuer Ratings: Aaa (stable) (Moody's) / AAA (stable) (S&P) / AAA (stable) (Fitch)/ AAA (stable) (Scope)

- Format: Registered Notes, Reg S (NSS) / 144A

- Ranking: Senior, Unsecured, Unsubordinated

- Listing: Luxembourg

- Settlement: 4 September 2025 (T+6 (TARGET) / T+5 (NY))

- Maturity Date: 4 September 2030 (5Y)

- HR 101% vs CT5 (T 3 ⅞ 07/31/30 )

- ISIN: Reg S: XS3171756128 / 144A: US29881WAG78

- Coupon: 3.75%, Fixed, Semi-annual, 30/360, Following, Unadjusted

- Bookrunners: CACIB(DM/B&D) / DB / JPM

From market source and Bloomberg.

The transaction comes ahead of a USD3bln redemption for the ESM in September. That line also had a 5-year maturity initially.