CANADA DATA: Jobs Growth Seen Pausing And U/E Rate A Little Higher In November

Dec-05 13:11

- The labour force survey for November is released ahead at 0830ET and should help shape expectations for how long the BoC is likely to remain on hold for after signalling a pause ahead in October.

- The overnight rate of 2.25% is deemed “about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment." BoC-dated OIS currently shows only 5-6bps of easing bias out to mid-2026.

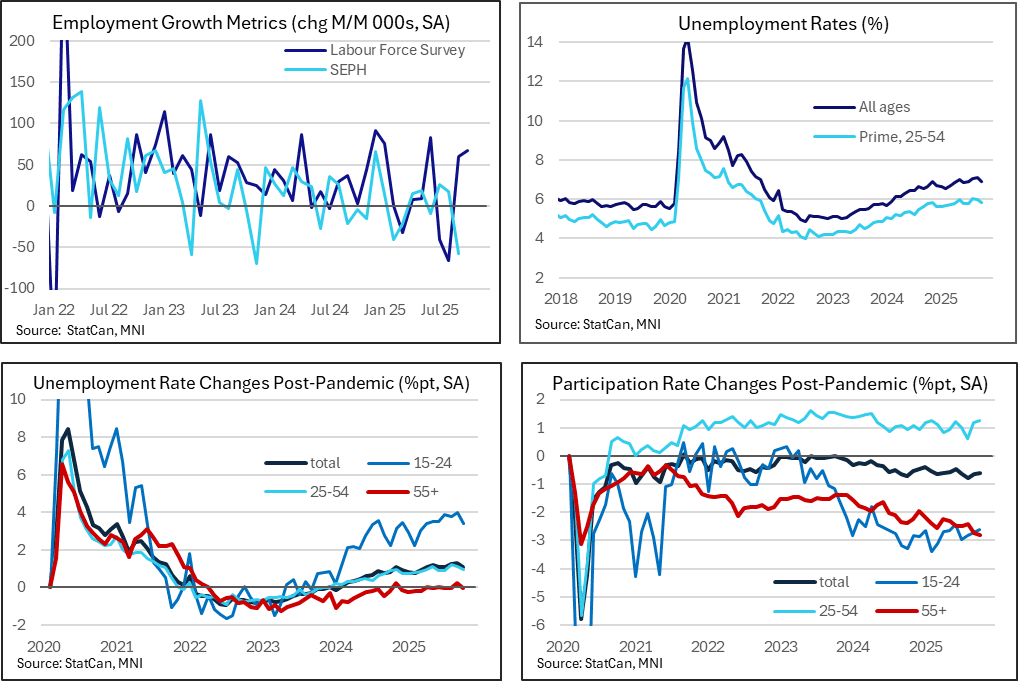

- Employment growth is expected to have slowed materially in Nov with Bloomberg consensus for -2.5k after a far stronger than expected 67k increase in October that came entirely from part-time positions. Separate payrolls data showed a sharp decline back in September with -58k but the two have weak correlation on a month-to-month basis.

- However, remember that the 127k cumulative increase in labour force survey employment in Sep-Oct followed a 106k decline in Jul-Aug. These monthly changes have been volatile for some time now whilst the unemployment rate helps gives a better sense of labour market pressures.

- Bloomberg consensus eyes a 7.0% unemployment rate (although with skew towards a lower print) after a surprisingly low 6.9% in October pulled back from two months at 7.1% at what were the highest since mid-2021. Having increased through 2023 and 2024, the climb in the unemployment rate has levelled off having averaged 6.9% since late 2024.

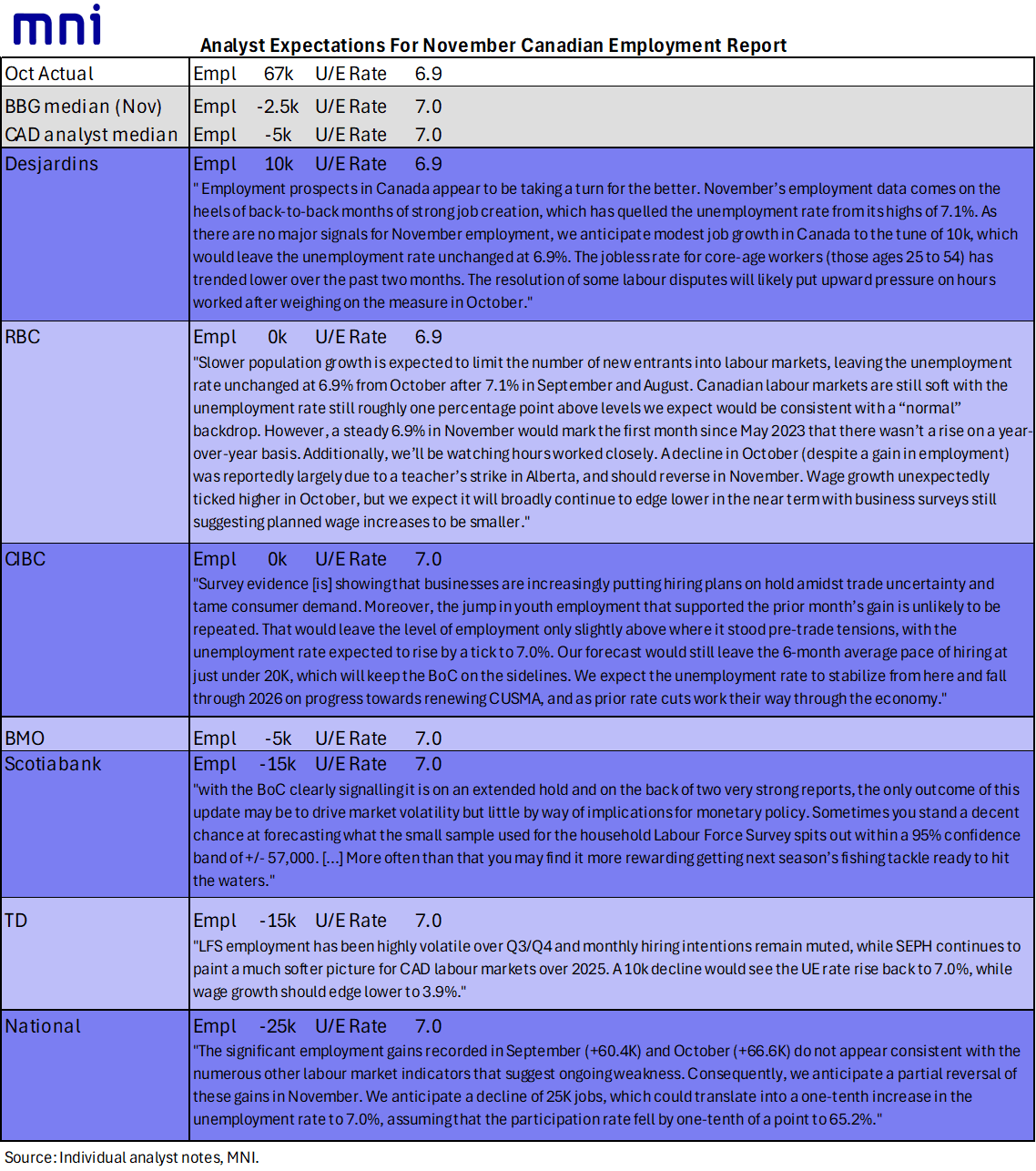

- See a range of Canadian bank analyst views in the table below.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS/SUPPLY: No Change To Coupon Size Guidance, But Bills Eyed in Refunding

Nov-05 13:11

A few areas to watch in today's 0830 Refunding announcement - MNI's full preview is here

- Guidance: We do not expect Treasury’s guidance on coupon issuance to change in this Refunding round ("Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.")

- Coupon sizes for upcoming quarter (Nov-Jan): As seen in table below. The Refunding itself will be $58B in new 3Ys, $42B in new 10Y, and $25B in new 30Y for next week.

- Buybacks: After being in some focus in August's Refunding, we don’t expect any changes to buyback program parameters this time, following the last round’s amendments that included higher-frequency operations/increasing the size of long-end buybacks. There are some risks that buyback sizes could be slightly increased, or that Treasury announces that the list of eligible counterparties will be expanded.

- Bill guidance: This will be of some interest given that borrowing expectations for the coming quarter were at the lower end of the expected range - one thing to watch will be if Treasury guides to reducing bill auction sizes soon having increased them significantly in late September/early October, helping push the TGA cash pile to the $1T mark. Last time that guidance read: "Treasury anticipates further marginal increases in short-dated Treasury bill auction sizes in the coming days and then maintaining sizes at or near those levels through the end of September. Additional increases to Treasury bill auction sizes are anticipated in October. Treasury will carefully monitor market conditions and adjust its bill issuance plans as appropriate. "

STIR: Repo Reference Rates

Nov-05 13:05

- Secured Overnight Financing Rate (SOFR): 4.00% (-0.13), volume: $3.147T

- Broad General Collateral Rate (BGCR): 3.98% (-0.11), volume: $1.183T

- Tri-Party General Collateral Rate (TCR): 3.98% (-0.11), volume: $1.156T

- (rate, volume levels reflect prior session)

PIPELINE: Corporate Bond Roundup: KEPCO, Santos Finance on Tap

Nov-05 13:03

- Date $MM Issuer (Priced *, Launch #)

- 11/05 $Benchmark KEPCO 3Y SOFR+62, 5Y +47

- 11/05 $Benchmark Santos Finance 10Y +195a

- $5.7B Priced Tuesday