LNG: JERA Signs LNG SPA with Hokkaido Gas for Seven Years From 2027

Dec-18 11:27

Japan's JERA has signed an LNG sales and purchase agreement with Hokkaido Gas to supply two-to-three LNG cargoes a year for seven years from 2027.

- JERA will supply about 130k to 200k metric tons of LNG annually, on a delivered ex-ship basis from its extensive global LNG portfolio, a JERA statement said.

- The deal contributes to reinforcing Japan’s energy security and enhancing supply resilience.

- The agreement supports JERA’s efforts to diversify its LNG sales portfolio while strengthening the stability and flexibility of Japan’s LNG supply.

- JERA aims to continue to build a balanced LNG portfolio across the Asia, Middle East, and the US to strengthen resilience against market volatility.

- The company also aims to enhance cost competitiveness and deepen collaborations with Japanese domestic energy partners and further expand LNG sales across Asia.

- Earlier this month, JERA signed a 10-year sales agreement with India’s Torrent Power for up to 270k tone per year of LNG from 2027.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Latest Fiscal Sell Off Limited To One Session

Nov-18 11:22

Gilts have stabilised after Friday’s sharp sell off.

- Chancellor Reeves’ reported u-turn on income tax rate hikes has not triggered an ongoing round of all-out market panic linked to worries surrounding the UK fiscal situation, with the resulting adjustment contained to one session.

- While benchmark yields are still 5-13bp off Thursday’s closing levels, they remain well below October highs.

- We previously noted that swap spreads remain some distance above year-to-date lows, which suggests that there is far less fiscal risk premium in the price vs. what seen during other stages of the year (admittedly with spillover from U.S. and German swap contributing to the recovery from lows multi-month).

- Looking ahead to next week’s budget, ING believe that the idea that “roughly half the fiscal hole is filled by upfront tax hikes feels like it is well priced now. Unless tax hikes are much less frontloaded in 2026, we doubt gilt yields need to rise materially on the back of this budget”. They also see a high bar when it comes to the budget blocking a cut from the BoE in December.

- Ultimately, they believe that “inflation should slow quickly, restoring confidence in a lower policy rate. Lower rates underpin the cost of financing positions for foreigners but may also help to restore needed confidence in fiscal management, Meanwhile shortening gilt supply and very moderate long-end QT should help to address the loss of historical support from UK pensions”.

- As a result, ING think UK 30-Year gilt yields could fall back to 4.40%.

- They suggest that the main risk to that view stems from political risks/a potential leadership challenge within the ruling Labour Party.

OPTIONS: Expiries for Nov18 NY cut 1000ET (Source DTCC)

Nov-18 11:14

- EUR/USD: $1.1600-05(E915mln), $1.1675(E1.4bln), $1.1700(E1.0bln)

- USD/JPY: Y153.00($1.3bln)

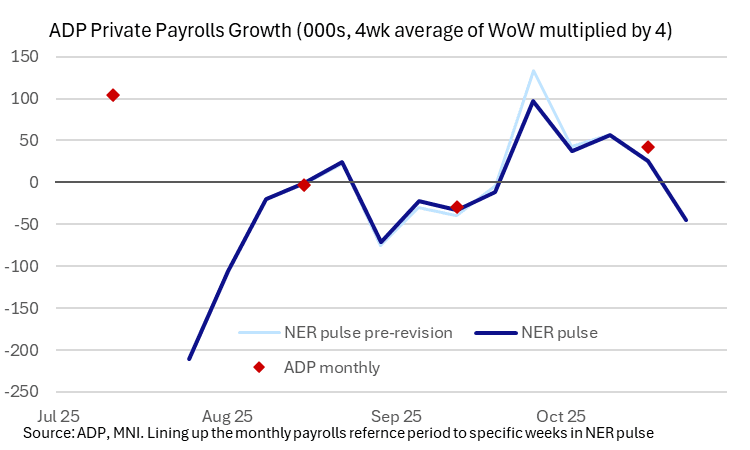

US OUTLOOK/OPINION: Weekly ADP Watched After Renewed Rolling Over

Nov-18 11:11

The weekly ADP report offers another timely update on labor conditions, watched to see if last week’s decline is revised and for latest momentum heading into November.

- The weekly ADP report will be released today at 0815ET, covering the four weeks up to Nov 1.

- Last week’s release was the first one when we knew it would be published and saw some dissemination issues.

- It was first published here: https://www.adpresearch.com/the-ner-pulse/ although ADP said beforehand that it would be published here: https://www.adpresearch.com/category/mainstreet-macro/. We’ll monitor both but expect a smoother release this week.

- Last week’s release suggested a return of private sector job losses in data up to Oct 25 with a four-week average decline of -11.25k jobs on a week-on-week basis. On its own it points to renewed sizeable deterioration in net job creation after some stabilization in the monthly October report with its +42k (for its reference week including the 12th of the month).

- ADP has warned that these data are preliminary and can be revised although last week’s release made it difficult to accurately assess these revisions in a timely manner.

- Fed Governor Waller (voter, dove), who is one of the leading voices calling for further cuts including at next month’s meeting, has referenced ADP data for some time. That included in yesterday’s speech (link): “While the ADP data are quite volatile and have some other shortcomings that make them less reliable than government statistics, I do think these data are telling us something. And in September and October, ADP reported that businesses created a net total of only 6,500 jobs a month. And the latest weekly data are even weaker.”

Related bullets

Related by topic

Energy Data

US Natgas

G3

North America

TTF ICE

Asia LNG

Asia

Gas Positioning

Japan