JGBS: JB1 Hovering Near Cycle Lows, No Chance of BOJ Hike Priced For Next Week

JGB futures are weaker, -17 compared to settlement levels, hovering just above cycle lows.

- The Bank of Japan is expected to keep its policy rate at 0.75% at the January 22-23 meeting following the December hike. The broader trajectory remains toward further tightening as Governor Kazuo Ueda has reiterated in recent guidance. However, with a snap election possible, we doubt Ueda will provide signals on the timing or magnitude of future hikes, given the risk of political backlash.

- Markets expect the BOJ to wait until the government’s tolerance for a weaker yen and higher yields is tested before tightening further, with a full 25bp hike priced in by July.

- US tsys are slightly cheaper in today's Asia-Pac session after finishing Thursday near session cheaps, with the curves flatter with the 30Y Bond outperforming.

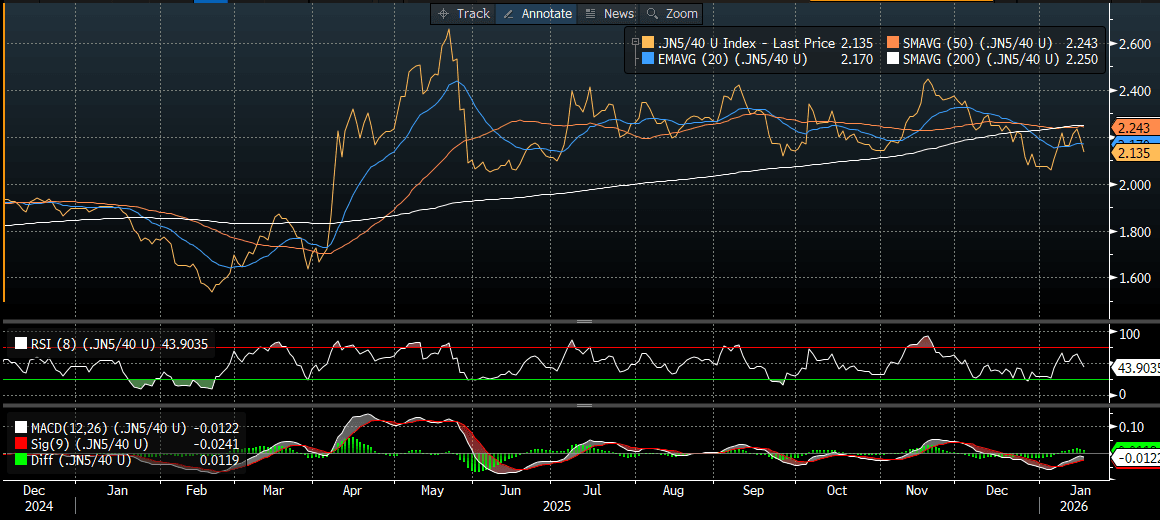

- Cash JGBs have twist flattened across benchmarks, with yields 2.2bps higher (5-year) to 3.5bps lower (40-year). Nonetheless, the 5/40 curve remains within the range it has traded in since May 2025 (see chart).

- Swap rates are 1bp higher to 2bps lower, with a flattening bias.

- On Monday, the local calendar will see Core Machine Orders, Industrial Production & Capacity Utilisation and Tertiary Industry Index data.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Chinese AI Chip Co. Debut Gives Tech Stocks a Boost

Asia's equity markets are higher today with China's bourses up as tech stocks rebounded and hopes of further interest rate cuts in the US prevail. The NIKKEI was up as it awaits the decision this week by the BOJ on interest rates with it widely expected that rates will rise by 25bps. China's bourses were buoyed by the market debut of AI chipmaker MetaX Integrated Circuits on the Shanghai exchange. MetaX shares jumped by over 600% on their first day of trading, following a similar stellar performance by rival Moore Threads earlier in the month. This highlights investor enthusiasm for homegrown Chinese technology companies amid geopolitical tensions with the US. The optimism for the tech sector in China spilled over into Korea with key tech stocks in Korea up between 1-3%.

- The NIKKEI feels like it is treading water ahead of the BOJ but remains up a mere +0.08% today, whilst the KOSPI found real support for tech stocks and is up +0.80%.

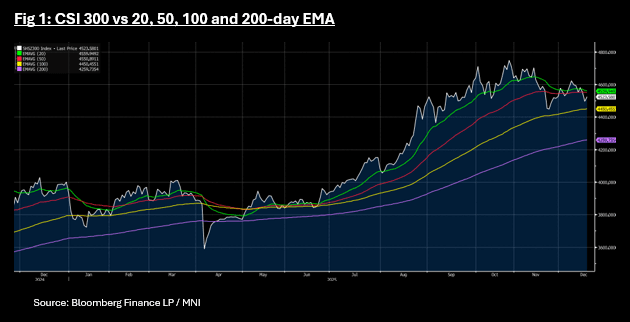

- China's major bourses were all up between +0.20% + 0.60% with the CSI 300 the outperformer. The gains for the CSI 300 to 4,523 sees it at the mid-point of the topside resistance from the 50-day EMA of 4,550 and the downside resistance from the 100-day EMA at 4,450.

- India's NIFTY 50 has opened flat after two days of falls as investors look for signals for US interest rates whilst commodity prices remain pressured.

- SE Asia's bourses were mixed with the Jakarta Comp up +0.20% and the FTSE Malay KLCI down -0.50%.

FOREX: USD - BBDXY Pushes Higher In Asia

The BBDXY has had a range today of 1204.77 - 1206.60 in the Asia-Pac session; it is currently trading around {BBDXY Index}. The USD broke below 1204 in reaction to the US data overnight, but it could not follow through and has recouped all of yesterday's losses and more. On the day I am a little confused, perhaps some patience is needed for a look back towards the 1208-110 area and above here the more important 1213-1216 area where sellers should remerge initially. Can this 1204 area provide some support again if not a move below here would target 1198-1200.

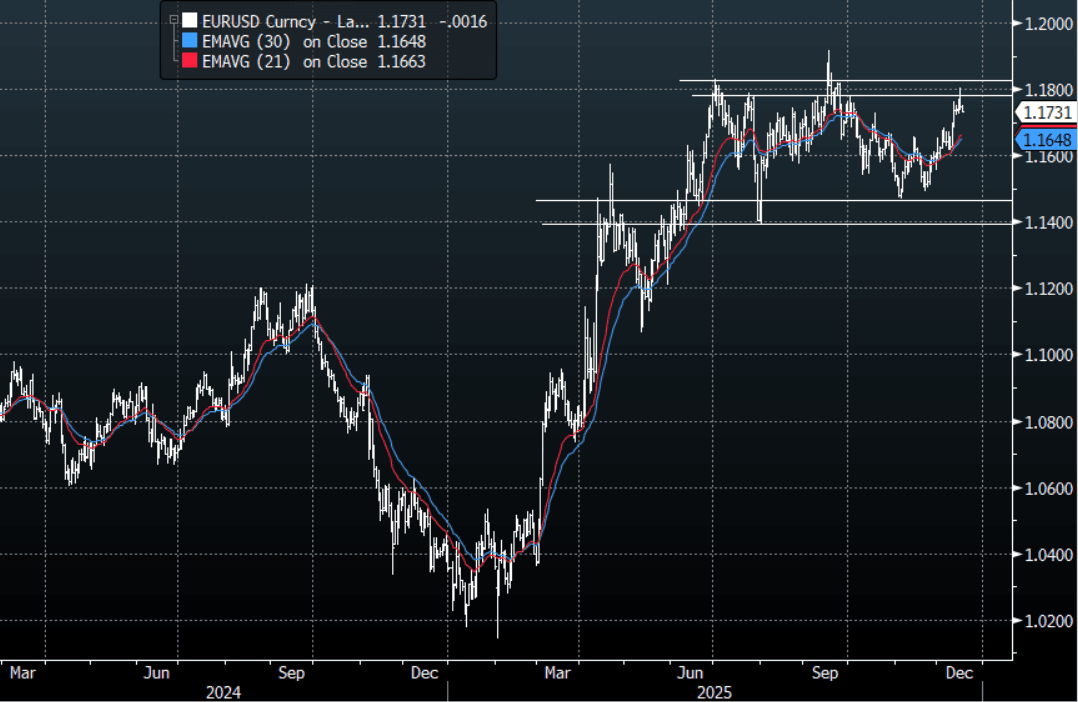

- EUR/USD - Asian range 1.1737-1.1752, Asia is currently trading {EURUSD Curncy}. The pair did not like it back up towards 1.1800 and very quickly rejected the move higher. On the day, first support is toward 1.1680-1710 initially, looking for the pair to consolidate before finding a base to attempt another move higher again.

- GBP/USD - Asian range 1.3407-1.3427, Asia is currently dealing around {GBPUSD Curncy}. The pair stalled back toward the 1.3450 level overnight. On the day GBP has initial support around the 1.3340-1.3370 area, if this does not hold look for a pullback to the more important 1.3260/90 area. I continue to watch for signs of GBP potentially topping out, which for the moment looks a lost cause.

- Cross asset : SPX -0.05%, Gold $4325, US 10-Year 4.16%, BBDXY 1205, Crude Oil $55.97

- Data/Events : Germany IFO, Spain Total Mortgage Lending, EZ CPI/Labour Costs YoY

Fig 1: EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: NZD/USD - Unchanged, Consolidating Above 0.5750

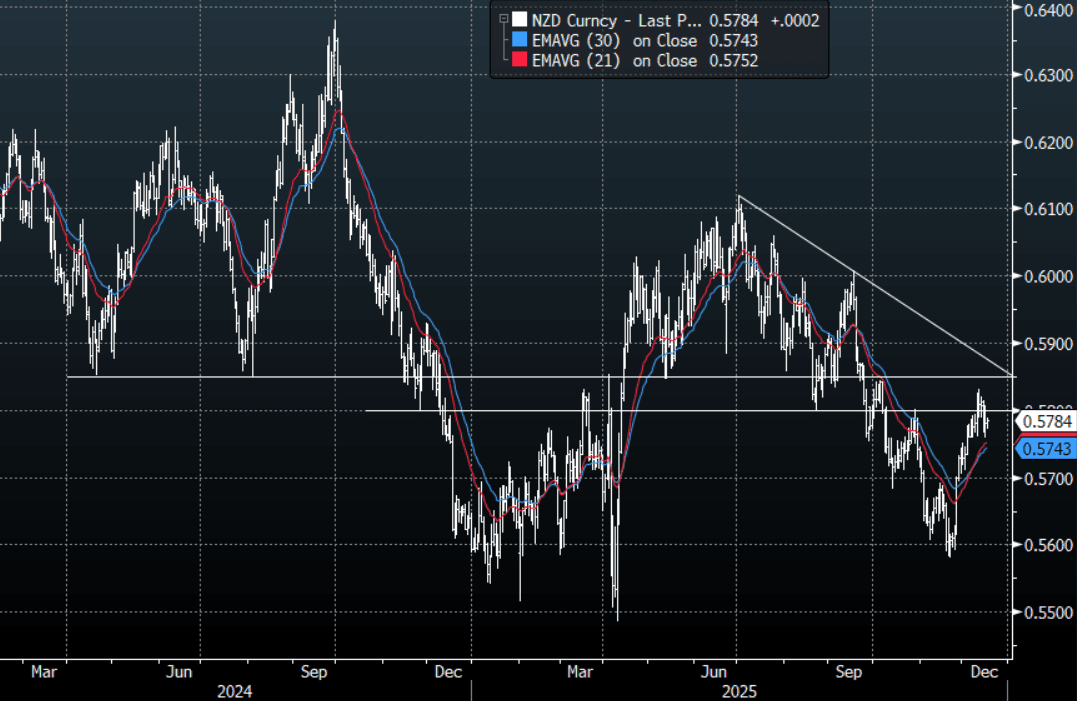

The NZD/USD had a range today of 0.5771-0.5789 in the Asia-Pac session, going into the London open trading around {NZD Curncy}. The NZD traded sideways in a quiet session, consolidating its gains above 0.5700-0.5750. On the day, I suspect this sort of price action could continue as the pair settles into a range, support is back toward 0.5740-0.5760 and resistance is around 0.5810-30.

- MNI AU - Q3 Current Account Deficit, As % Of GDP, Continues Improvement: The Q3 headline current account deficit widened to -NZD8.365bn, from, -NZD1.297bn in Q2, but this is part of the typical seasonal norms. In seasonally adjusted terms we were slightly wider in Q3 at -NZD3.8bn. As a percent of GDP, the deficit was -3.5% in YTD terms, slightly wider than the -3.4% forecast but still an improvement on the Q2 outcome of -3.7%. The deficit trend as a share of GDP continues to improve, we were at -9.0% of GDP at the end of 2022.

- MNI AU - Further Weakness In Whole Milk Prices, Back To Mid 2024 Levels: Overnight the GDT whole milk auction price fell sharply, down 5.7% on the prior outcome to $3161/mt. This is the lowest level since mid 2024 for the twice monthly auction outcome. The Q3 official terms of trade print for NZ showed a 2.1%q/q fall. We were still up 7.2% in y/y terms. Export prices are moving off earlier 2025 highs, consistent with lower whole milk auction price outcomes.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5780(NZD344m), 0.5800(NZD502m), 0.5850(NZD328m). Upcoming Close Strikes : 0.5630(NZD594m Dec 19), 0.5690(NZD531m Dec 18 ), 0.5860(NZD471m Dec 18 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 42 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P