JAPAN DATA: Japan Nov Retail Sales +2.8% Y/Y

- Japanese retail sales rose 2.8% y/y in November, accelerating from the 1.3% y/y growth reported last month.

- On a monthly basis, retail sales increased 1.8%, compared with the 0.2% decrease in October.

- General merchandise sales rose 0.9% y/y, improving from the 3.9% y/y decrease last month, while sales of fabric apparels and accessories increasing 10.7%, quickly up from the 0.7% increase registered last month.

- Sales of food and beverages increased 1.4% y/y, up from last 0.1% y/y decrease.

- Fuel sales, another key driver, increased 3.6% y/y, accelerating from the previous 2.6% y/y growth.

- Sales of machinery and equipment up 2.6% y/y, lower than the 3.4% y/y growth previously.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

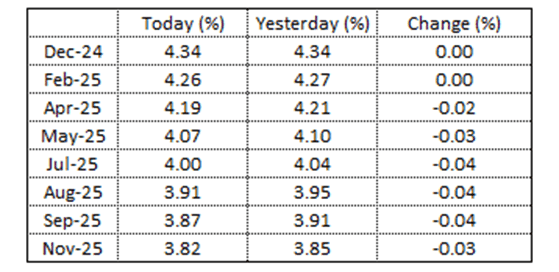

STIR: RBA Dated OIS Softer Ahead Of October CPI Data

RBA-dated OIS pricing is flat to 4bps softer across meetings, with the mid-2025 contracts leading the move.

- A 25bps rate cut is not fully priced until May.

- Notably, pricing for the May meeting is now 12bps softer than two weeks ago, when a full 25bps cut wasn't expected until August.

Figure 1: RBA-Dated OIS – Today Vs. Yesterday

Source: MNI – Market News / Bloomberg

AUSSIE BONDS: ACGB Dec-34 Supply Absorbed But Less Demand

Expectations of sustained strong pricing at auctions proved accurate, with the latest round of ACGB Dec-34 supply seeing the weighted average yield print 0.49bp through prevailing mids (per Yieldbroker).

- However, as flagged in our auction preview, a lower outright yield and flatter curve did appear dampen the overall strength of bidding today, with the cover ratio decreasing to 2.8375x from 3.2125x previously.

- The deterioration in sentiment towards global bonds over recent months also likely weighed.

- The ACGB Dec-34 cash line and the XM futures contract are slightly richer in post-auction dealings.

RBNZ: Possibility Easing Pace Could Be Increased Or Reduced

The RBNZ decision is announced today and is widely expected, including by the market, to cut rates 50bp to 4.25% (see MNI RBNZ Preview). The MPC’s discussion could be around easing 25bp, 50bp or 75bp. The economy has developed broadly in line with its expectations. With policy still restrictive, inflation probably sustainably within the 1-3% band and persistent excess capacity, there seems no reason to reduce or increase the pace of easing in November.

- A 25bp cut would be hawkish but it’s a possibility. October’s discussion was between 25bp or 50bp of easing. The economy has developed broadly as the RBNZ expected in August when the Q4 2024 OCR forecast was 4.9%. Rates are below that and so the MPC may decide to slowdown. Also, some monthly data are stabilising.

- Another reason for 25bp would be mixed Q4 inflation expectations. Some household measures were unchanged and the mean 2-year ahead rose 0.6pp to 3.7%.

- We don’t think that the RBNZ will yet be factoring in the inflationary impact from US President-elect’s proposed trade and fiscal policies, apart from the weakening of the kiwi already seen since the election. It is unlikely to react to what might happen.

- 75bp would signal “panic”, especially as it is above market pricing. Such a move could be driven by the fact that the next meeting is almost three months out and that rates are still well above neutral. This could add to the urgency to ease if the economic outlook is downgraded.

- The RBNZ highlighted higher frequency indicators and the PSI/PMI remain weak. BNZ estimates they are consistent with growth below -1%.

- An OCR forecast implying 25bp rate cuts per quarter in 2025 reaching the current terminal of 3% would be more hawkish, but dovish if the trough is revised materially below.