POWER: Italy September Power to Open Higher

The Italian September power is expected to edge higher, once liquid, tracking gains in EU gas prices, while forecasts for cooler weather in late August may limit the upside.

- Italy Base Power SEP 25 closed down 1.3% at 108.84 EUR/MWh on 12 Aug

- Italy Power Cal 26 closed down 1% at 105.45 EUR/MWh on 12 Aug

- TTF Gas SEP 25 up 0.6% at 32.59 EUR/MWh

- EUA DEC 25 up 0.1% at 71.56 EUR/MT

- TTF is edging up from a low of €32.25/MWh yesterday amid thin trading ahead of Norway maintenance next month and with focus on the outcome of Friday’s Trump-Putin meeting.

- The latest two-week ECMWF weather forecast for Rome suggests mean temperatures have been revised down to remain above normal until the end of next week, before dropping below normal.

- Mean temperatures in Rome are forecast at 27.7C on Thursday, from 27.8C on Wednesday and above the seasonal normal of 25.5C.

- The PUN index rose to €118.47/MWh for Wednesday’s delivery, up from €113.53/MWh the day before.

- Wind output in Italy is forecast at 946MW during base load on Thursday, from 1.15GW on Wednesday. Solar PV output is forecast at 10.9GW during peak load on Thursday, down from 11.49GW on Wednesday according to SpotRenewables.

- Power demand in Italy is forecast at 32.52GWh/h on Thursday, down from 36.08GWh/h on Wednesday, RTE data showed, with demand declining due to national holiday in Italy on Friday.

- Residual load in Italy is forecast at 25.91GWh/h on Thursday, from 28.69GWh/h on Wednesday, Reuters data showed.

- Italy’s hydro balance forecast has been revised down to end at -1.23TWh on 27 August, compared with -1.06TWh previously, Bloomberg data showed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US-RUSSIA: Trump Expected To Announce UKR Weapons Package, Endorse RU Sanctions

10:00 ET 15:00 BST: President Donald Trump will hold a (closed press) White House meeting with NATO SecGen Mark Rutte, where he is expected to finalise a new plan to arm Ukraine “that is expected to include offensive weapons,” per Axios. Later today, Trump is expected to make a 'major statement' on Russia. No timing has been released.

- Axios reports the plan is likely to include long-range missiles that could reach targets "deep inside Russian territory” a “major shift for Trump, who had until recently [said] he would provide only defensive weapons to avoid [escalation].”

- Politico reported the weapons package "numbers in the hundreds of millions”, and “could come from the fund approved by [Biden] that lets the DOD give weapons from the U.S. military stockpile...”

- Trump's 'major statement' is also likely to include preliminary approval of Senator Lindsay Graham's (R-SC) punitive sanctions/tariffs bill, reworked to provide Trump full discretion over implementation.

- Graham said on X: “.... A turning point is coming.” He told Axios: "Trump is really pis--- at Putin. His announcement tomorrow is going to be very aggressive."

- Senate Majority Leader John Thune (R-SD) indicated the bill will hit the Senate next week. House Speaker Mike Johnson (R-LA) endorsed the bill, putting it on a track to Trump’s desk.

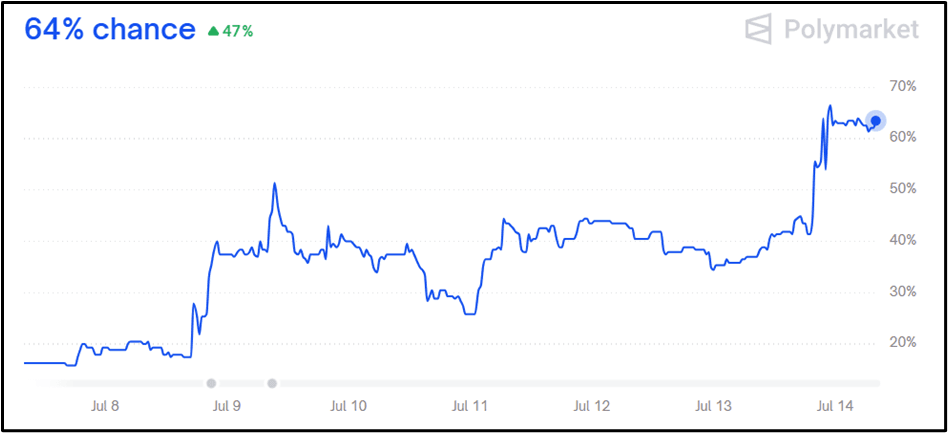

- Polymarket sees a 64% chance Trump increases Russia sanctions before August, a significant spike since last week.

Figure 1: Trump increase sanctions on Russia before August?

Source: Polymarket

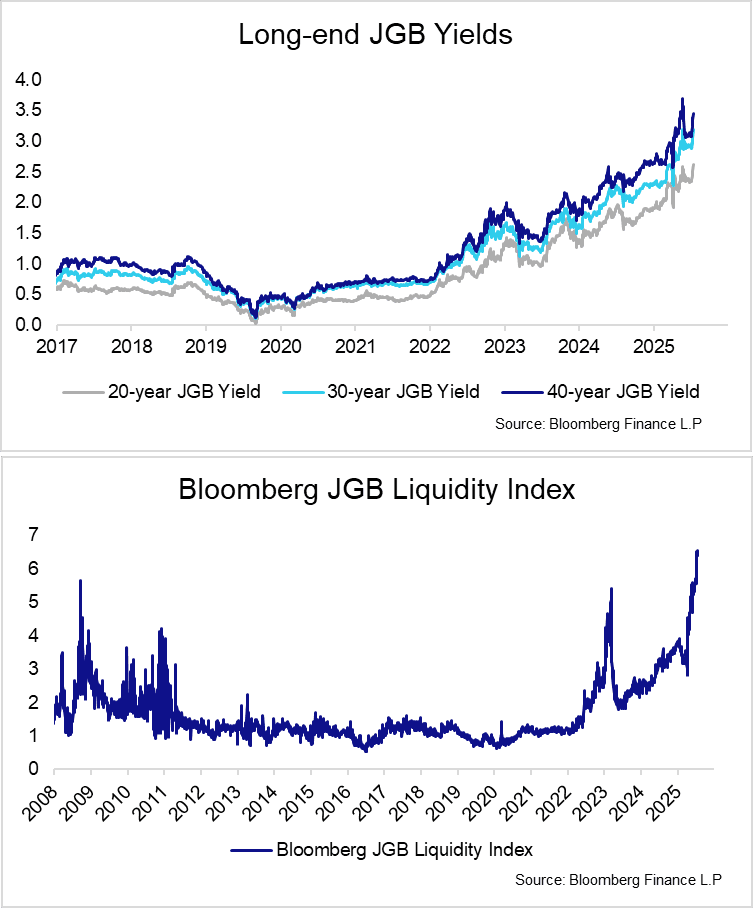

JGBS: Steepening Extends With 30-year Yields Eyeing May 21 High

Bear steepening in the JGB curve has extended this morning, spilling over into long-end EGBs and Gilts. 10s30s is currently just under 5bps steeper at 157.3bps, still below last Tuesday’s 160.3bp high.

- 30-year yields are up 11bps at 3.172%, with initial key resistance the May 21 high at 3.204% (the highest level since the BBG series began in 1999).

- Meanwhile, 10-year yields pierced the May 22 high of 1.582% overnight, but are currently back at 1.580% (+6bps today).

- As already noted, a combination of fiscal/political risks and possible upgrades to the BOJ’s inflation projections at the upcoming July 31 decision have contributed to the latest rise in yields.

- The Upper House election will be held on July 20. The LDP is on course to lose a significant number of seats and the governing coalition could also lose its overall majority. JNN reporting overnight was supportive of this scenario.

- Meanwhile the latest Bloomberg sources reporting was consistent with last week’s MNI Policy Team piece: BOJ officials may increase their median CPI forecast for FY25 from 2.2% partly due to a temporary surge in rice prices, MNI understands. The steepening of the curve suggests this is a contributing factor of today’s JGB selloff, rather than a driver.

- Structural forces pushing long-end JGB yields higher also remain in play, namely concerns around demand for long-end debt and weak liquidity at that portion of the curve.

- This week’s Japanese calendar includes 5-year supply tomorrow, June trade data on Thursday and June national CPI on Friday.

SILVER TECHS: Impulsive Bull Wave Extends

- RES 4: $40.285 - 1.618 proj of the Apr 7 - 25 - May 15 swing

- RES 3: $40.000 - Psychological round number

- RES 2: $39.655 - 1.500 proj of the Apr 7 - 25 - May 15 swing

- RES 1: $39.093 - Intraday high

- PRICE: $38.961 @ 08:18 BST Jul 14

- SUP 1: $36.493 - 20-day EMA

- SUP 2: $35.334 - 50-day EMA

- SUP 3: $33.967 - Low Jun 3

- SUP 4: $32.615 - Low May 22

Trend conditions in Silver are unchanged, a strong impulsive bull cycle remains intact and today’s gains further reinforce current conditions. The metal has cleared key short-term resistance at $37.317, the Jun 18 high. This confirms a resumption of the uptrend and sights are on the $39.655 next, a Fibonacci projection. On the downside, initial support to watch lies at $36.493, the 20-day EMA.