EUROPEAN INFLATION: Italy HICP Undershoots But Core At Highest In A Year

Aug-29 10:03

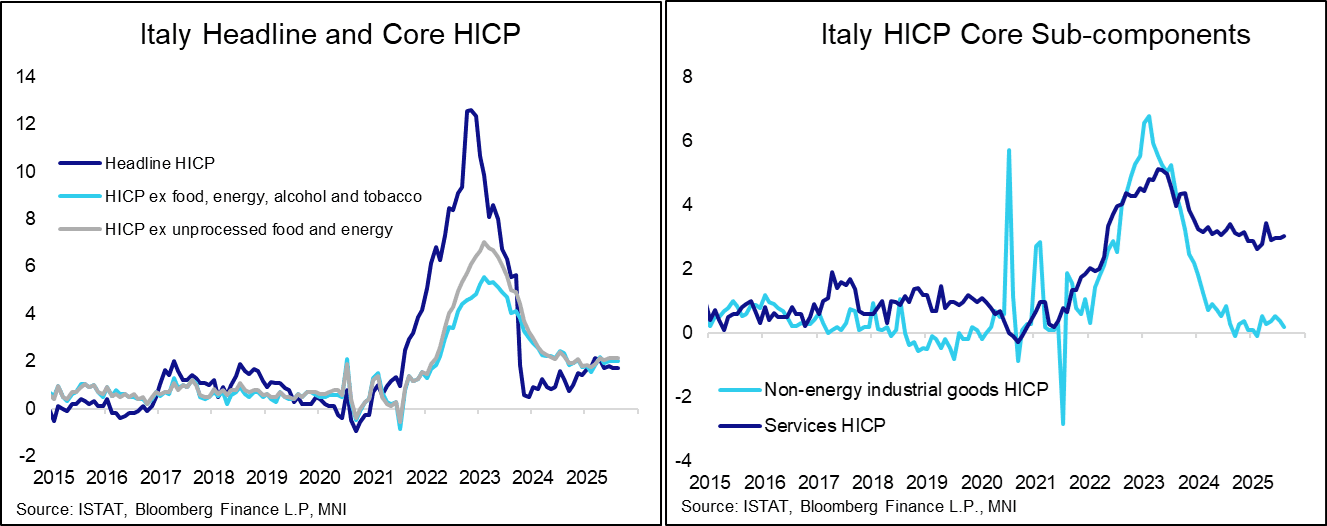

The preliminary August release for Italian inflation saw HICP and CPI headline measures a tenth softer than expected in Y/Y terms but core metrics firmed a tenth, with the HICP core at its highest since Aug 2024.

- HICP inflation held at 1.7% Y/Y (Bloomberg cons 1.8) in the preliminary August release, having rounded to 1.7% in three of the past four months.

- On the month, HICP fell -0.2% M/M (cons 0.0) after -1.0% M/M.

- Core HICP inflation (ex energy & unprocessed food) firmed a tenth to 2.2% Y/Y after two months at 2.1%, extending to a new fresh high since Aug 2024.

- Services HICP inflation also firmed a tenth to 3.0% Y/Y although has been oscillating between 2.9-3.0% for four months now and remains below the pop higher to 3.4% Y/Y in April.

- Service-heavy categories saw a further sizeable drag from housing & utilities (-0.4% Y/Y after 0.2%) along with relative weakness in health (2.7% after 3.2%). Offsetting this were accelerations for communications (-4.2% after -4.6%), recreation & culture (1.6% after 1.0%) and restaurants and hotels (3.1% after 2.8%).

- Elsewhere, energy provided a sizeable drag at -4.4% Y/Y after -3.5% in July whilst food, alcohol & tobacco inflation inched a tenth higher from 3.8% to 3.9% Y/Y for its fastest since Jan 2024.

- National-basis CPI inflation meanwhile eased to 1.6% Y/Y (Bloomberg cons 1.6) from 1.7% in July, with monthly inflation of 0.1% M/M (cons 0.2) after 0.4% M/M.

- Core CPI inflation accelerated a tenth to 2.1% Y/Y, echoing the uptick in the core HICP noted above.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

DUTCH T-BILL AUCTION PREVIEW: On offer next week

Jul-30 10:02

The Netherlands has announced it will be looking to sell the following next Monday, August 4:

- E0.5-1.5bln of the 4-month Nov 27, 2025 DTC

- E1.0-2.0bln of the new 6-month Jan 29, 2026 DTC

OUTLOOK: Price Signal Summary - S&P E-Minis Bull Cycle Remains In Play

Jul-30 09:51

- In the equity space, the trend set-up S&P E-Minis remains bullish. Recent cycle highs once again confirm a resumption of the uptrend. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, 1.618 projection of the May 23 - Jun 11 - 23 price swing. Support at the 20-day EMA is at 6322.32.

- The trend condition in EUROSTOXX 50 futures is unchanged, it remains bullish and short-term weakness appears corrective. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of this level would strengthen a bearish threat. For bulls, a resumption of gains and a clear break of 5486.00, the May 20 high, would resume the bull cycle and open 5500.00.

GILTS: Tender Demand & Eyes On Month-End Underpin Rally

Jul-30 09:33

Gilts remain underpinned.

- Late Tuesday cues from Tsys provided support at the open, with solid demand at the GBP300mn tender of the 3.75% Jul-52 gilt then helping underpin after a pullback into the bidding deadline.

- A reminder that month-end index extension projections for gilts are sizeable, which could also be factoring into today’s rally.

- Futures have pierced resistance at the 20-day EMA (91.82). Bulls now eye the July 22 high (92.15). highs of 91.97 seen thus far. To the downside, well-defined key support comes in at the July 18 low (91.08).

- Benchmark yields 3-4bp lower, curve marginally flatter

- 2s10s and 5s30s remain in fairly close proximity to 75bp and 140bp, respectively, trading back from ’25 highs, but consolidating the bulk of the year-to-date steepening.

- GBP STIR pricing takes cues from the rally in the long end. SONIA futures flat to +1.5, BoE-dated OIS little changed, showing 46bp of easing through year-end, with ~90% odds of an August cut priced.

- Little of note on the UK calendar for the remainder of today, which will leave focus on broader headline flow, as well as the U.S. quarterly refunding announcement and GDP data ahead of the FOMC decision.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 3.994 | -22.3 |

Sep-25 | 3.960 | -25.7 |

Nov-25 | 3.808 | -40.9 |

Dec-25 | 3.754 | -46.3 |

Feb-26 | 3.647 | -57.0 |

Mar-26 | 3.611 | -60.6 |