EU BASIC INDUSTRIES: Industrials: Week in Review

Oct-31 14:39

- Air Liquide issued €2.15bn across 4-tranches to finance the €2.85bn DIG Airgas acquisition. The 4yr and 7.5yr were 3-4bps tighter in secondary. 12yr +1bp wider. The company had solid earnings with a growing backlog.

- Verallia was placed on Outlook Neg at Moody’s following last week’s profit warning. The bonds are only rated by S&P though. Levels unchanged.

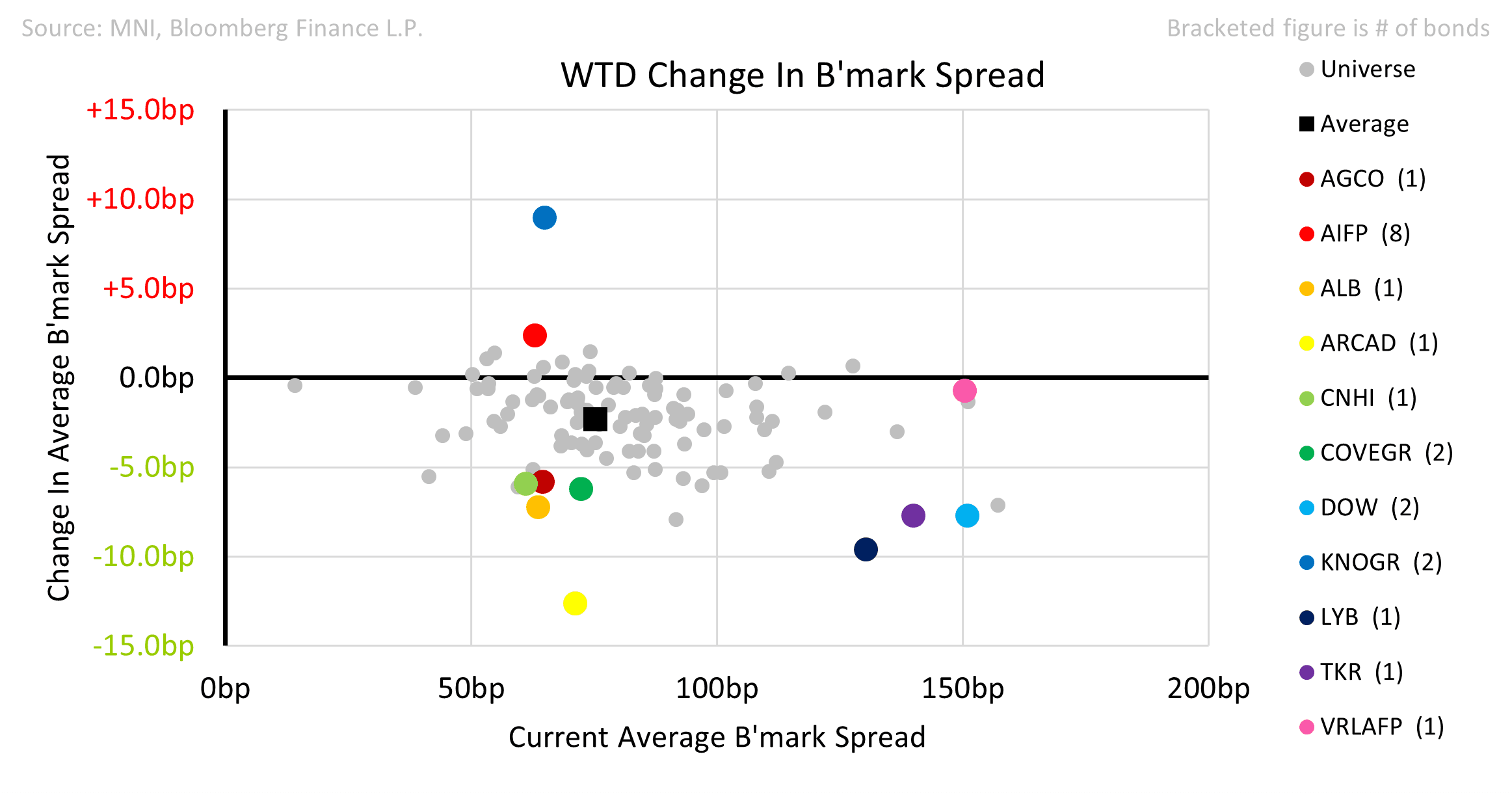

- Albemarle announced a $660m asset sale which will be used to reduce debt. Curve -7bps tighter.

- Westlake, Covestro and Symrise had weak results. DSM-Firmenich reduced guidance slightly.

- Knorr-Bremse had poor results in Commercial Vehicles; curve +9 wider.

- Imerys management said that the market is still weak so will focus on cost cutting.

- UPM-Kymmene was squeezed on pricing and costs with EBITDA down 44%. Leverage now 2.4x vs 1.6x 3Q24.

- Glencore benefitted from an uptick in copper production. Anglo American was largely unchanged but sees its main Chilean copper mine back to full production by 2027.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: BLOCK: Dec'25 SOFR Put Condors

Oct-01 14:38

- 10,000 SFRZ5 96.12/96.25/96.37/96.50 put condors, 6.25 net at 1029:44ET

GILT AUCTION PREVIEW: On offer next week

Oct-01 14:33

The DMO has announced it will be looking to sell GBP5bln of the new 4% May-29 Gilt (ISIN: GB00BVP99566) at its auction next Wednesday, October 8.

STIR: Fed Pricing Slightly Less Dovish After ISM, Bulk Of Dovish ADP Move Holds

Oct-01 14:33

FOMC-dated OIS incrementally less dovish (little changed to 1.5bp of easing taken out of Fed meetings through June ’25) since the ISM manufacturing survey crossed, showing 25bp of easing through October, 47bp through December, 69bp through March and 89bp through June.

- SOFR-implied terminal rate pricing last 3.03% vs. 3.085% heading into the ADP data and hawkish September extremes of 3.145%.

- Lack of reaction to the data isn’t particularly surprising given ongoing focus on the labour market (earlier dovish repricing was driven by a soft ADP report) and the ISM release showing only a slight, uneven improvement in manufacturing conditions amid soft demand (as detailed in our recent macro bullet).

Related bullets

Related by topic

AIFP

France

EU Utilities

VRLAFP

ALB

Germany

WLK

US

COVEGR

SYMRIS

NK

UPMFH

Finland

GLENLN

UK

AALLN (del)