HYBRIDS: Hybrids: Week in Review

Aug-29 12:43

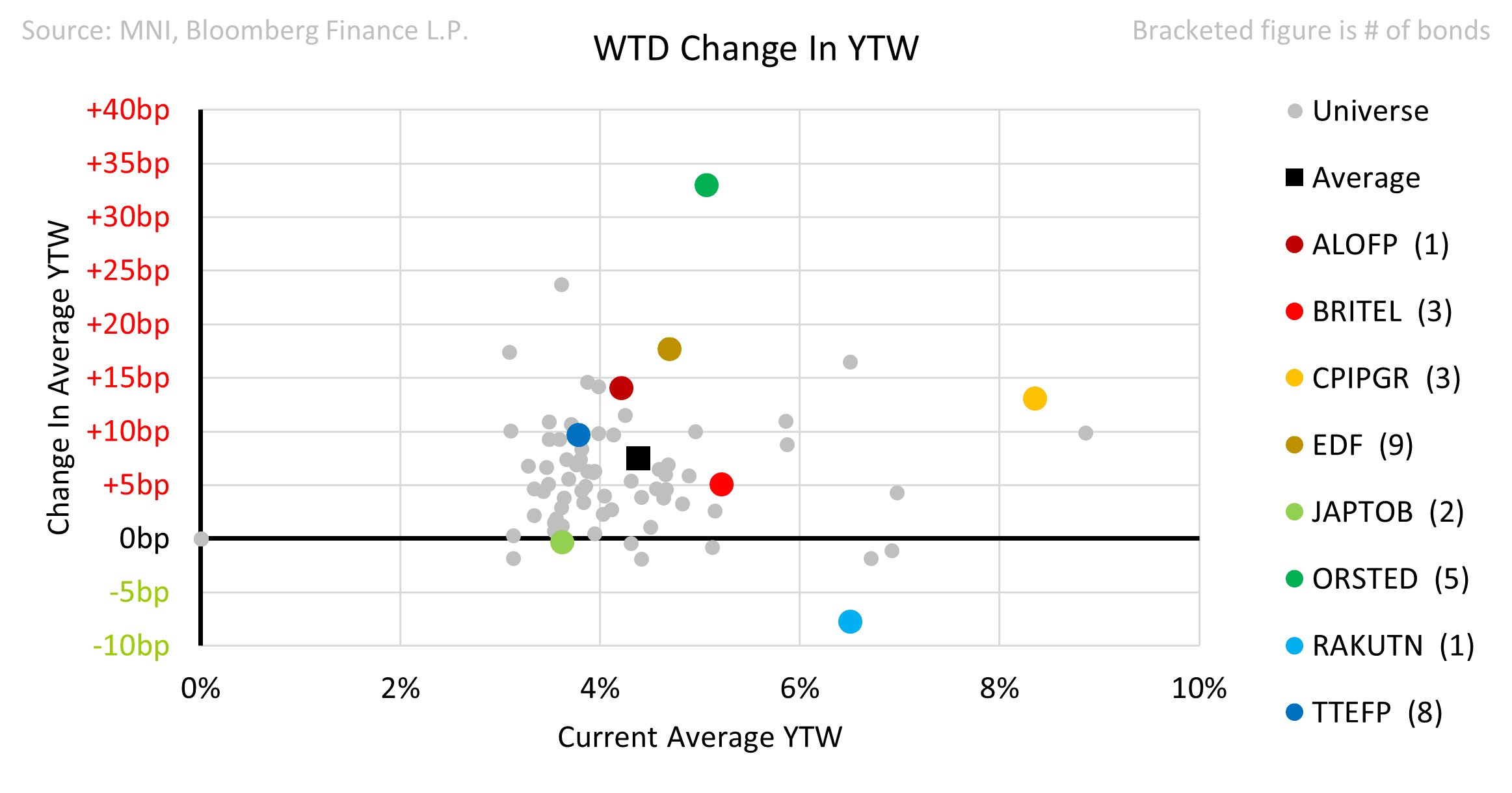

- Japan Tobacco extended its Hybrid deck with an any-and-all Tender of the NC26 combined with a new €500m 30NC5.5. The deal benefitted from an A3 rating under Moody’s new regime. Books were almost €8bn for the transaction which priced with a 75bps Sub_Sen spread.

- Orsted perps were 1-1.5pts lower as further US political risk for offshore projects weighed on sentiment. More details in Utils section above.

- French names were soft this week on Political concerns. EDF was up to 75c lower, ALOFP -65c, FRPTT -64c, TTEFP -50c. BRITEL NC31 +35c was a rare gainer.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Trump Post on the US GDP and level of Rates

Jul-30 12:40

Donald J. Trump

@realDonaldTrump

2Q GDP JUST OUT: 3%, WAY BETTER THAN EXPECTED! “Too Late” MUST NOW LOWER THE RATE. No Inflation! Let people buy, and refinance, their homes!

US TSYS: Post-Core PCE, GDP React

Jul-30 12:34

- Fast two-way flow -- Treasury futures bounce then extend lows after higher than expected GDP and Core PCE figures. Tsy Sep'25 10Y futures currently trades -6.5 at 111-05 (111-03.5 low, 111-14.5 high).

- Key support is 110-08+, the Jul 14 and 16 low. Clearance of this level would reinstate a bearish theme. First support is at 110-19+, the Jul 24 low. Resistance at 111-13+, the Jul 10 high, has been pierced. A clear break of it would highlight a stronger reversal and open 111-28, the Jul 3 high.

- Curves mildly flatter now: 2s10s -0.091 at 44.854, 5s30s -0.507 at 95.021

- New pullback lows for EUR/USD as the greenback builds again on the better-than-expected GDP headline. EUR/USD comfortably through yesterday's lows to open 1.1454 as the next downside target.

MNI: US Q2 NOM PCE +1.4%

Jul-30 12:30

- MNI: US Q2 NOM PCE +1.4%

- US Q2 REAL FINAL SALES TO PRIVATE DOMESTIC PURCH +1.2%

- US Q2 PCE PRICE INDEX +2.1%

- US Q2 CORE PCE PRICE INDEX +2.5%