JGBS: Holding Gains At Lunch

At the Tokyo lunch break, JGB futures are stronger, +27 compared to settlement levels, in choppy tra...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

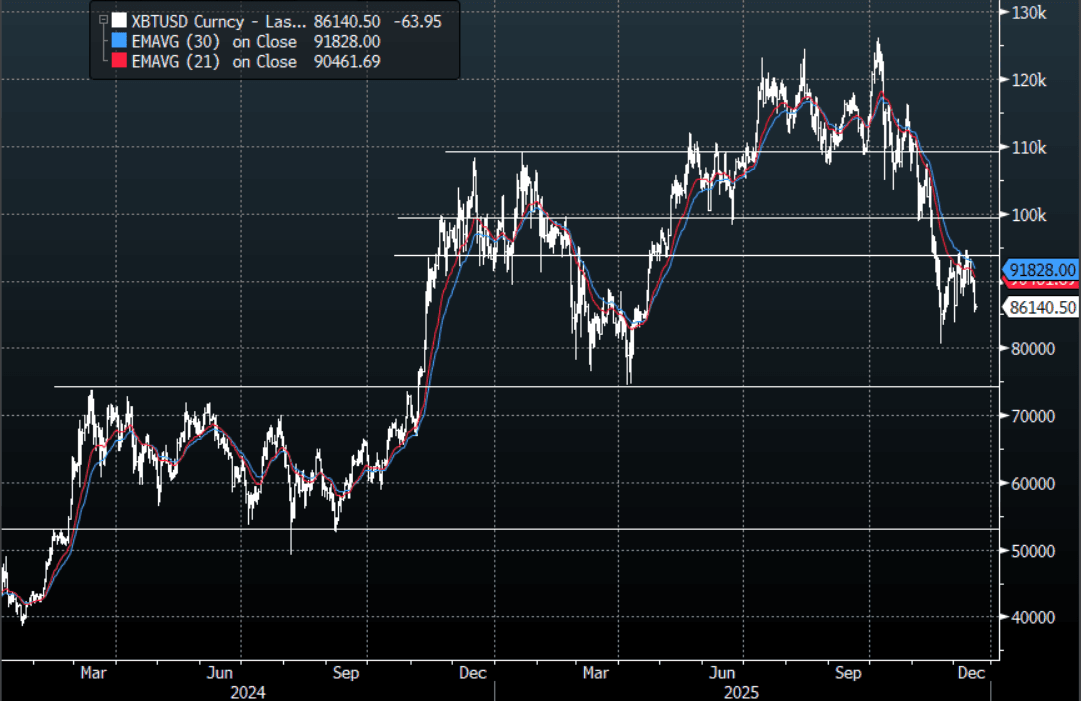

CRYPTO: Bitcoin - Falls Back Toward $84-$85k Support, Can It Hold Again ?

Bitcoin had a range overnight of $85,171.28k - $89,981.80k, Asia is currently trading around $86,150k, -0.10%. Bitcoin slipped lower again very easily in the N/Y session falling over 5% from the session highs. Risk is trading under pressure this morning heading into some important data inputs from the US tonight. This has seen price challenge the bottom of its recent $84k-$96k range, technically Bitcoin remains in a downtrend so while this remains the case bounces back towards the $96-$101k area looks like it would be faded initially. We are challenging the first support in the $84k-$86k area, a break below here and the market will again turn its focus back toward $80k and then the $70k-$75k support. This is the very well known line in the sand for the huge Bitcoin "treasury" company Strategy who has continued to buy into this dip by the sale of a combination of common stock and perpetual preferred shares, and it is still lower. {NSN T7BBN2T96OSH <GO>}

- Alexander Stahel on X: “Saylor’s creditors won’t care about Saylor’s ideology. We are $11k away from this point at a $75k average. Something else I am missing?”

- Shanaka Anslem Perera on X: “STRATEGY’S 671,268 BTC: THE BINARY MOMENT. The math remains unchanged. mNAV compressed to parity. Market cap now equals Bitcoin holdings. The premium that funded four years of accumulation has vanished. 720 million dollars in annual preferred dividends. Compounding. The 1.44 billion dollar buffer covers twenty four months. Not twenty five. MSCI decision in 30 days. 2.8 billion in estimated passive outflows if excluded. JPMorgan’s numbers. Not mine.”

- “BTC must exceed 12 percent annualized returns to outpace funding costs. Below that threshold, the Minsky moment accelerates. Saylor has made this binary. January fifteenth begins the verdict from the MSCI. Either we witness the largest corporate treasury failure in financial history or the birth of something the models cannot yet comprehend.”

- Bitcoin’s Average True Range(ATR) for the last 10 Trading days: $2,888

Fig 1: Bitcoin spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA PRESS: Non-Bank Deposit Slowdown Due To Less Capital Market Activity

The latest central bank data indicated that in November the growth rate of yuan deposits slowed markedly, experts told the Yicai news agency. Non-bank deposits rose by CNY80 billion, representing a year-on-year decline of CNY100 billion, with most institutional analyses suggesting that the pace of residents’ “deposit migration” had temporarily eased, largely reflecting reduced activity in capital markets. Wang Xianshuang, chief banking analyst at China Merchants Securities, said non-bank deposits had rebounded strongly in October, mainly due to banks’ quarter-end efforts to attract resident and corporate deposits, which in turn led to swings in wealth management and margin deposits—underscoring the inherently volatile nature of non-bank deposits. Data from other institutions showed that the volume of resident deposits maturing next year will exceed CNY170 trillion, nearly CNY20 trillion more than this year, with many industry professionals noting that the “deposit migration” trend will continue into next year.

CHINA PRESS: Excess Property Supply Damaging Confidence

The proportion of people searching for second-hand homes reached 65.8% in November, rising for five consecutive months, according to data from Anjuke, a real-estate research firm. However, the popularity did not raise prices as a surge in supply diluted demand enthusiasm, with listing volumes in some cities increasing significantly, according to Zhang Bo, a director at Anjuke. Core cities may see narrowing declines in the future due to resilient demand, but the overall market is still in a stage of bottoming out and building momentum, Zhang added. Specifically, in November, the sales prices of newly built commercial housing in first-tier cities fell by 0.4% month on month, with the decline widening by 0.1 percentage points compared with October. In November, second-hand housing sales prices in first-tier cities fell by 1.1% month on month, with the decline widening by 0.2 percentage points compared with October.