AUSSIE 10-YEAR TECHS: (H6) Found Bottom?

* RES 3: 95.982 - 76.4% retracement Sep'24 - Nov'24 downleg * RES 2: 95.960 - High Apr 7 (cont.) * R...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

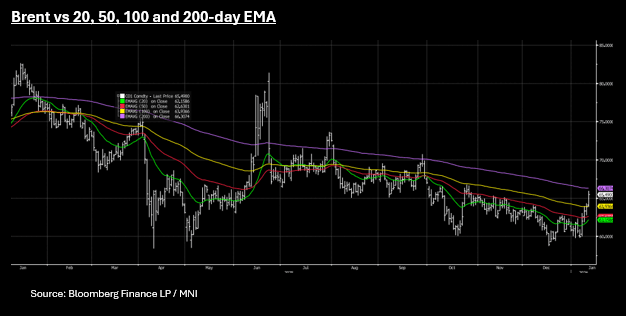

COMMODITIES: WTI Above US$61 bbl, Gold Moderates from New High Post US CPI

- As President Trump increases the rhetoric at Iran, oil prices rallied above key levels and to the highest since October. Concerns about Iran's domestic unrest and potential military action added a geopolitical premium to oil prices, outweighing concerns of a global oversupply.

- Posting on Truth Social, the President supported Iranians continuing demonstrations, saying he had “cancelled all meetings” with the country’s officials. This as the US Energy Secretary Chris Wright says the US would “happily be a commercial partner” to get “better price realizations” for Iranian crude oil if the regime there falls.

- WTI finished up +2% Tuesday at US$61.09 bbl trading through the 100-day EMA of $60.16. It is the first time since September that WTI has traded above the 100-day EMA given the weakening trend since August.

- Brent rose +1.8% to US$65.47 bbl also back at October levels and near to the 200-day EMA of US$.

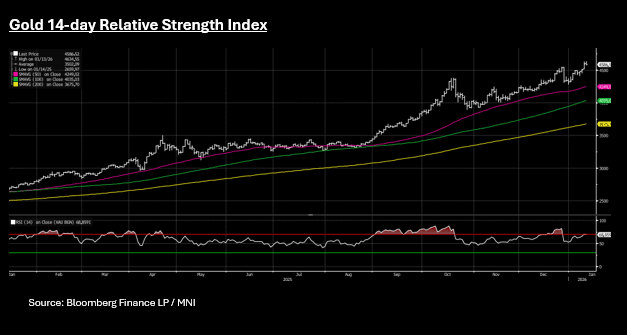

- Despite geopolitical tensions at the forefront of investors minds, gold finished modestly down as profit takers came in following new highs in place and US CPI for December in line with forecasts.

- Earlier, gold had reached US$4,634.55 intra-day before falling back to finished down -0.24% at US$4,586.52

- At US$4,586.52 gold is near to overbought on the 14-day relative strength index.

- Gold has started 2025 where it left off in 2025 and has rallied +5.6% year to date already.

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.870 @ 15:51 GMT Jan 13

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again on Thursday last week, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

AUSSIE BONDS: Slightly Mixed, Light Data Day, Oct-36 Supply

ACGBs (YM +0.5 & XM -1.5) are slightly mixed after cash US tsys finished little changed, well off the morning's knee-jerk post-CPI data bests. Markets continue to digest multiple anomalies in the data set stemming from a reversal of November holiday sale discounting for goods products, along with sampling issues from the use of bimonthly metro area surveys (with no October data for comparison due to no survey that month).

- Today’s US data includes PPI, Retail Sales and Existing Home Sales data.

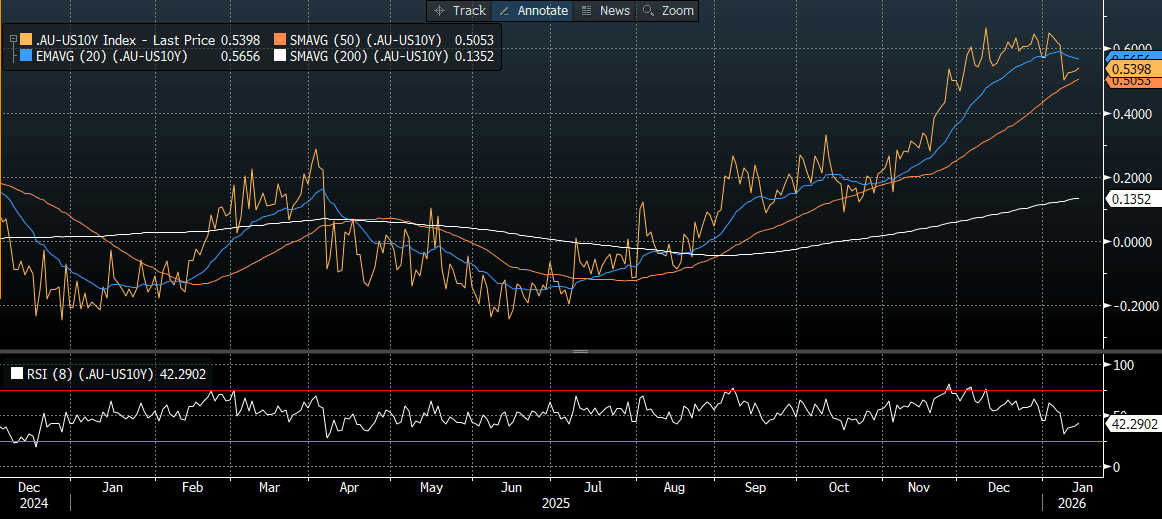

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +54bps. A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month (1Y3M) swap spread over the past two years suggests the current spread sits close to its regression-implied fair value.

- The bills strip is slightly stronger, with pricing +1 to +2 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 31% for February to 91% by June and 136% by December 2026.

- Today, the local calendar will see Job Vacancies.

- The AOFM plans to sell A$1bn 4.25% 2036 bond today and A$700mn 3.25% 2029 bond on Friday.

Bloomberg Finance LP