BUNDS: German 10yr Yield highest since 2011

* As expected the German 10yr Yield gaps higher to match the March high of 3.129%, although it did...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD TECHS: In Oversold Territory But Remains Bearish

- RES 4: $5044.6 - High Mar 17

- RES 3: $4806.6 - 50-day EMA

- RES 2: $4741.6 - 20-day EMA

- RES 1: $4655.7 - Low Feb 6

- PRICE: $4559.3 @ 07:24 GMT Mar 31

- SUP 1: $4306.4/4099.2 - Low Mar 24 / 23

- SUP 2: $4000.0 - Round number support

- SUP 3: $3945.2 - 1.236 proj of the Jan 29 - Feb 2 - Mar 2 price swing

- SUP 4: $3771.1 - 1.382 proj of the Jan 29 - Feb 2 - Mar 2 price swing

Gold is unchanged and remains in consolidation mode. Short-term trend signals are bearish and the recovery from the Mar 23 low is considered corrective. Note that the downtrend is in oversold territory and a stronger corrective bounce would allow this condition to unwind. Key near-term resistance is at $4806.6, the 50-day EMA. For bears, a resumption of the bear leg would open $3945.2, a Fibonacci projection.

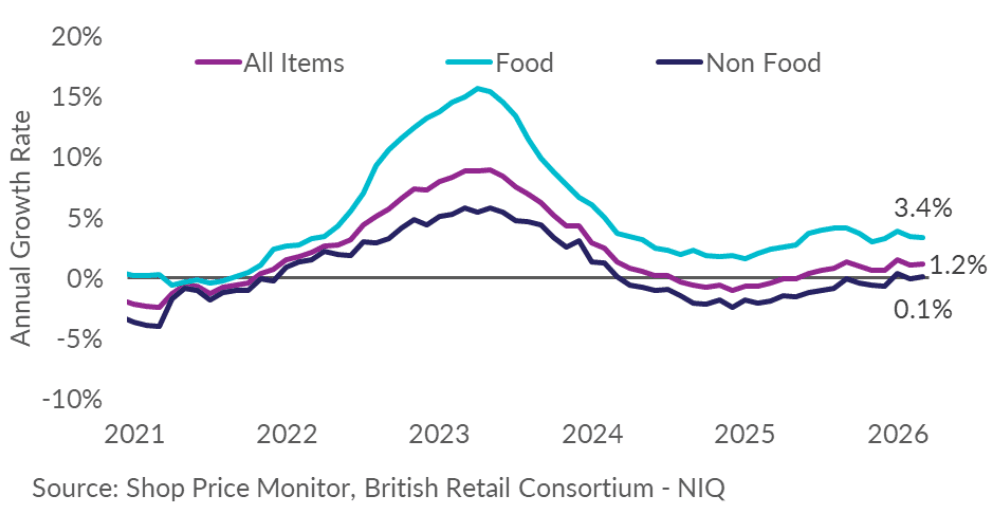

UK DATA: BRC Shop Price Inflation Edges Up, but Down M/M; Energy Impacts Unclear

BRC shop price inflation edged up 0.1ppt in March to 1.2% Y/Y (1.1% Feb, 1.5% Jan) on base effects, as prices fell 0.1% M/M (after 0.0% Feb, +0.4% Jan). Movements in core goods prices will see less focus than usual in CPI data given the large fuel price increases that will be incorporated into the print and any additional transportation costs that feed into core goods prices will not be evident in the data yet. Still, the press release comments that conflict-driven cost pressures are starting to feed into supply chains.

- Food inflation slowed a touch to 3.4% Y/Y (3.5% Feb, 3.9% Jan), again driven by ambient food as opposed to fresh food. Month-on-month, food prices fell 0.1% M/M (after 0.0% Feb, +1.1% Jan).

- Within food, ambient food inflation slowed again to 2.0% Y/Y (2.3% Feb, 3.1% Jan), now well off January's spike, while fresh food inflation rebounded to 4.4% Y/Y (4.3% Feb, 4.4% Jan), still notably above December's 3.8% Y/Y.

- Non-food inflation picked up to 0.1% Y/Y (-0.1% Feb, 0.3% Jan), back in positive territory but still hovering around flat. The press release notes some Six Nations-driven promotions on TVs and sound systems, as well as on clothing and footwear helping the rate lower.

- Both the slightly earlier collection date vs official CPI and, more importantly, the narrower range of goods means the effects of the shock to energy prices are probably not as pronounced here as they will be in the official ONS CPI data (due 22nd April). The release covers the retail prices of 500 commonly-bought high street products between 1-7 March 2026.

- Comments from the press release: "Higher costs resulting from the conflict in the Middle East are starting to feed into supply chains. While retailers will work with their suppliers to mitigate the impact on prices as far as possible, inflation will rise, although there are no indications it will reach the peaks of the last spike in April 2023."

- "Whilst it’s good news that food inflation slowed in recent weeks, shoppers are increasingly conscious of the amount of money they are spending at the checkout, and non-food retailers will be hoping for a good Easter to drive sales. However, if price rises come through the supply chain over the next few months, this has the potential to take the edge off retail growth.”

GILT TECHS: (M6) Trend Outlook Remains Bearish

- RES 4: 91.52 High Mar 10

- RES 3: 90.29 High Mar 18

- RES 2: 89.00 20-day EMA

- RES 1: 88.18 High Mar 26

- PRICE: 87.67 @ Close Mar 30

- SUP 1: 85.91 Low Mar 23 and the bear trigger

- SUP 2: 85.89 2.500 proj of the Feb 27 - Mar 3 - 4 price swing

- SUP 3: 85.59 2.618 proj of the Feb 27 - Mar 3 - 4 price swing

- SUP 4: 85.21 2.764 proj of the Feb 27 - Mar 3 - 4 price swing

Gilt futures continue to trade above their recent lows. The trend condition remains bearish and recent gains appear to have been corrective. Sights are on 85.91, the Mar 23 low. A break of this level would confirm a resumption of the downtrend and signal scope for an extension towards 85.59, the 2.618 projection of the Feb 27 - Mar 3 - 4 price swing. On the upside, resistance to watch is 89.00, the 20-day EMA.