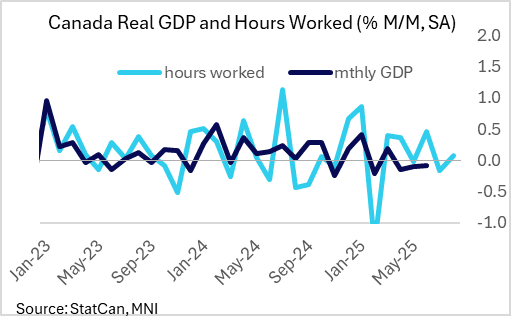

CANADA: GDP Preview: Some Relief Seen In July After Weak Q2

Sep-26 11:37

Bloomberg consensus sees July real GDP (by industry) growth of 0.1% M/M, vs -0.1% in June. That would be in line with StatCan's advance estimate, and would mark a rebound of sorts from 3 consecutive months of decline.

- That rate of growth would keep the 3M/3M annualized (ie quarterly) growth rate at -0.6%, after June's -0.7% was the weakest since the pandemic. Note the monthly industry GDP data do not translate directly to the overall quarterly GDP reading, though the industry-level dynamics did capture the deterioration in GDP to -1.6% in Q2 from +2.0% in Q1. Real GDP for Q3 is seen at 0.2% per Bloomberg consensus.

- Factors pointing to a pickup in growth in July include M/M improvements in exports, manufacturing, and wholesale data, as well as activity surveys such as S&P Global and Ivey PMIs; on the downside there was weakness in retail sales and employment / hours worked.

- Some sell-side analyst views:

- BofA (-0.1%): "The Canadian economy is likely to continue showing signs of weakness"

- National (+0.1%): " higher output in the real estate/rental/leasing and wholesale trade categories having likely been partially offset by a decline in the retail trade

segment" - TD (+0.1%): "Manufacturing shipments showed some early signs of stabilization in July on stronger auto production, while natural resources should provide another source of strength after a pickup in crude oil output. Services should see a mixed performance with offsetting contributions from wholesale/retail sales, as real estate provides another source of strength. Monthly activity data looked much brighter in July relative to Q2, but a pullback in hours worked (alongside material job losses) poured some cold water on the prospects a sharp rebound for Q3."

- RBC (+0.2%): "It is highly likely that Bank of Canada policymakers expect that additional interest rate cuts will be needed after reducing the overnight rate for the first time since March in September. But, further reductions are also more contingent than usual on more softness in economic data. Our tracking for GDP growth in early Q3 is not significantly different than the BoC’s, but its decision to cut again (or not) in October will depend heavily on early October trade and labour market data, as well as the results from the BoC’s Business Outlook Survey."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

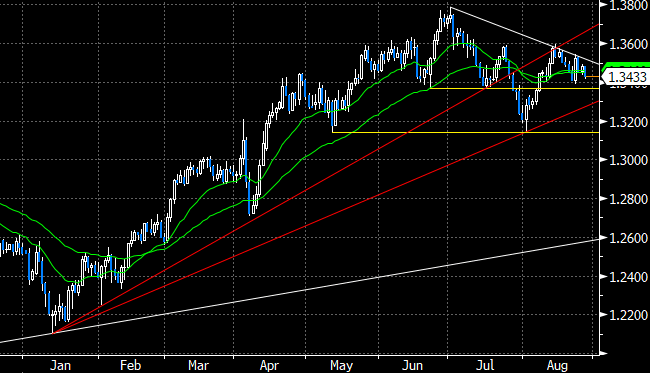

FOREX: GBPUSD Approaching Key Short-Term Support Amid Dollar Recovery

Aug-27 11:27

- Broader dollar strength has been extending into the NY crossover on Wednesday, as political concerns in Europe provide a moderate risk-off tone and post JH Powell positions are squeezed.

- This is contributing to GBPUSD also fully reversing the Powell induced move, although last Friday’s lows remain untested for now. This level at 1.3391 marks a key short-term support for the pair, of which a break would signal scope for a move towards 1.3315, the 61.8% retracement of the Aug 1 - 14 bull leg.

- Trendline support drawn from the year’s lows would then come back into focus, of which a breach may threaten the broader medium-term uptrend that has been evident this year. JP Morgan remain of the view that investors should be using any GBP rallies to set up bearish multi-month exposure covering the UK budget.

- JPM point out that what stood out last week is the lack of GBP strength on strong PMI and inflation data, which suggests focus may be on long end gilts and pressure on the chancellor. Sticky inflation, critiques on UK tax policy options and UK yield moves all add to UK government funding gap woes heading into the autumn budget. As part of JPM’s macro trade recommendations, they suggest keeping GBP shorts vs EUR, CHF, NOK & SEK.

SEK: SEB: Neutral Month-End Rebalancing Outlook

Aug-27 11:25

SEB’s model suggests that month-end rebalancing needs for the typical Swedish portfolio manager are SEK neutral.

OUTLOOK: Price Signal Summary - Resistance In Bunds Remains Intact

Aug-27 11:19

- In the FI space, Bund futures continue to trade above their recent lows. A bear threat remains present. The contract recently breached 128.84, the Jul 25 low and a bear trigger. Note that the 129.00 handle represents the base of a broad range. A clear range breakout would strengthen a bearish theme. This would open 128.40 initially, the Apr 9 low. Strength above the 50-day EMA of 129.78, is required to signal a reversal.

- A bear cycle in Gilt futures remains in play and yesterday’s fresh cycle low reinforces current conditions. Note that on the continuation chart, moving average studies are in a bear-mode position, highlighting a clear downtrend - for now. First support to watch is 90.25 (pierced), the Aug 26 low. A clear break of it would resume the bear leg and open the 90.00 handle. Initial resistance is at 91.24, the Aug 18 high.