CANADA DATA: GDP Expected To Confirm Tepid Bounce In Q3 – 0830ET

Nov-28 13:15

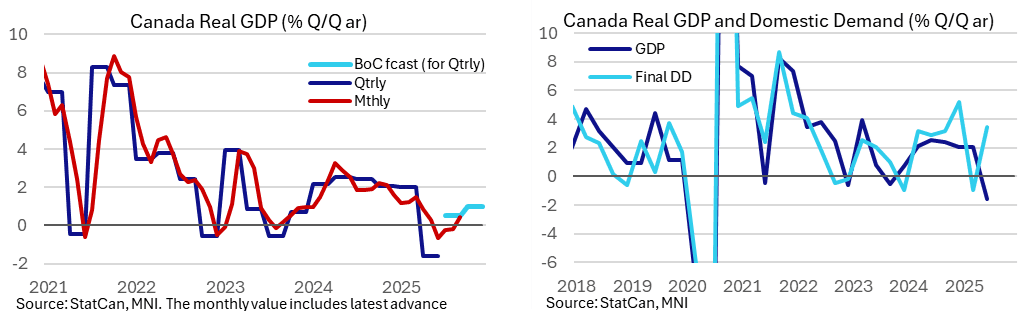

Real GDP growth for Q3 and separate monthly data for Sep/Oct advance are released shortly at 0830ET. The BoC puts more weight on the expenditure-based quarterly data, although the production-based monthly data still offer a valuable idea of momentum into Q4. Both however are likely more susceptible than usual to US trade-related revisions.

- Canadian GDP data is released at 0830ET for Q3 along with the monthly report for September and its advance estimate for October.

- Bloomberg consensus eyes real GDP growth of 0.5% annualized in Q3, with a range of -0.4% to 0.8%, after a heavy decline of -1.6% in Q2 when net exports dragged a huge ~7.5pp annualized from GDP.

- Six of the seven largest Canadian banks all look for 0.5% (BMO, Desjardins, National, RBC, Scotia and TD), with CIBC the exception at 0.7%. RBC doesn’t currently show in the Bloomberg survey.

- For the monthly series, Bloomberg consensus of 0.2% M/M sees upside risk to the 0.1% indicated in last month’s advance estimate, following upward revisions to manufacturing and wholesale trade.

- Analyst estimates on Bloomberg range from -0.1% to 0.2% M/M, with seven estimates for 0.2%, but RBC is again not included here and looks for a stronger 0.3% M/M.

- It follows two noisier months with -0.3% M/M in Aug and 0.3% M/M in Jul, but the prior trend had been weaker with three consecutive -0.1% M/M prints through Apr-Jun.

- As for potential advance estimates for October, CIBC pencil in a “small 0.1% increase” on the back of “little information regarding October available as yet”.

- The BoC last month forecast a 0.5% increase in Q3 before 1.0% in Q4. More broadly, it sees real GDP growth of 0.5% Y/Y in 4Q25 before 1.6% in both 4Q26 and 4Q27.

- Helping put these numbers into context, the BoC estimates potential output growth of 1.6% in 2025, 1.0% in 2026 and 1.3% in 2027.

- The Bank opted for a hawkish cut last month, signalling a pause ahead with the overnight rate of 2.25% deemed “about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment."

- BoC-dated OIS has nothing priced for the Dec 10 meeting although there is up to 10bp of cuts priced out in mid-2026. We suspect risks to near-term pricing from this release specifically are to the downside although with Thanksgiving timing likely limiting trading activity.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY OPTIONS: Estoxx downside Put Spread

Oct-29 13:10

SX5E (20th Mar) 4800/4400ps, bought for 16.8 in 17k.

BOC: Instant Answers For Today's Decision

Oct-29 13:08

Following are the questions for MNI Instant Answers for the Bank of Canada decision due out at 0945ET:

- Target for overnight rate

- Does the Bank signal it is prepared to lower rates in the future?

- Does the Bank say lower interest rates will likely be needed in the future?

- Does the Bank signal it intends to leave rates on hold?

- Does the Bank mention core or underlying inflation has been elevated?

- Does the Bank say it may be less forward looking with policy?

EQUITY OPTIONS: Large Stoxx600 Put Option

Oct-29 13:04

SXXP (19th Dec) 535p, bought for 1.95 and 2 in ~19.83k.