JGBS: Futures Up From Recent Lows, Back End Yields Lower, 40yr Auction Later

JGB futures have edged up a little in the first part of Thursday trade. We were last 135.91, -.05 versus settlement levels. Intra-session lows from Wednesday came in just under 135.80. US Tsy futures are up slightly for TY so far today. The BoJ minutes, as well as the services PPI print, have come and gone and not impacted market sentiment much.

- In the cash JGB space, we are slightly softer in terms of back end yields. The 40yr is back near 3.37%, off around 2bps. We have the 40yr debt auction later. The 10yr is close to 1.645%, little changed. The JGB 2/30s curve maintains a flattening bias. Similar trends are evident in the swap space.

- In terms of the BoJ July Minutes, via our Tokyo based policy team: Policymakers judged upside risks to prices had not strengthened, according to the minutes. One member said underlying inflation lay within a “range” and was recently around 1.5%–2.5%. Another noted it appeared to be about 2% but stressed sizable downside risks to prices remained, given estimation errors and uncertainty around indicators. On trade, several members highlighted the need to monitor the effect of U.S. tariff policy on major manufacturers’ profits, spillovers to smaller firms, and knock-on effects for 2026 wage negotiations. One member said at least two to three months were needed to assess the impact, but added that if the U.S. economy proved more resilient than expected, Japan’s downturn risk would be limited, potentially allowing the BOJ to end its wait-and-see stance as early as end-2025.

- On the data front we had the Aug PPI services print, which was slightly below market expectations. The Japan August PPI service print came in below expectations, printing at 2.7%y/y against a 2.9% forecast. Note that the July outcome was revised down to 2.6%y/y (originally reported at 2.9%). Today's PPI outcome brings it more into line with recent CPI outcomes, with the CPI tending to lead this recent period of softness in y/y momentum.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

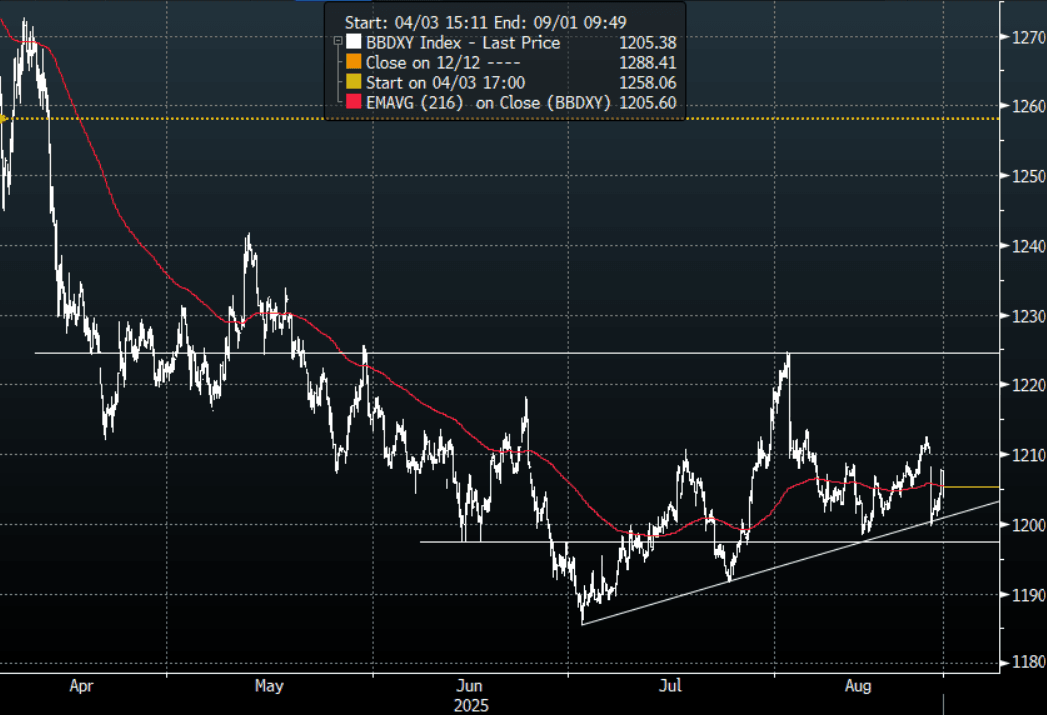

USD: BBDXY - Demand Towards 1200 Holds, Trump Firing Cook Brings Back Selling

The BBDXY range overnight was 1201.02 - 1207.89, Asia is currently trading around 1205, -0.20%. The USD bounced after finding good demand back towards 1200 again overnight. This morning's news that Trump has removed Fed Governor Cook will just add fuel to the rate cut fire, with Trump now in a position to appoint another uber dovish Governor to do his bidding. This has seen the USD fall quickly and could further erode confidence in US institutions which would provide further headwinds for the USD. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows.

- ISABELNET on X: “Dollar - Powell's speech has put the US dollar gauge under pressure, confirming a test of technical support is underway amid growing market bets on imminent Fed rate cuts to address softer employment data and economic risks.”

- Robin Brooks on X: “The Dollar is on a rising trend since July 2. Periodic setbacks like payrolls revisions on Aug 1, CPI on Aug 12 and Powell's Jackson Hole speech on Aug 22 hit USD, but after each of these it starts rising again. This is important. Markets aren't negative on the Dollar anymore...”

- Bloomberg - “The greenback’s three-month basis against five peers is on track to turn negative for the first time since August 2020 — a sign of fading foreign appetite for Treasuries. Factors possibly narrowing premiums include relative liquidity and prospects for Fed rate cuts, Mizuho said.”

- Data/Events : Philadelphia Fed Non-Man Activity, Durable Goods Orders, FHFA House Price Index, Richmond Fed Man Index/Bus Conditions, Conf. Board Consumer Confidence, Dallas Fed Services Activity

Fig 1: BBDXY 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

MNI: CHINA PBOC CONDUCTS CNY405.8 BLN VIA 7-DAY REVERSE REPO TUES

- CHINA PBOC CONDUCTS CNY405.8 BLN VIA 7-DAY REVERSE REPO TUES

NEW ZEALAND: NZIER Reduces Cash Rate Forecast Due To Disappointing Recovery

The NZIER has released its “Quarterly Predictions” and following the RBNZ’s signalling last week, it is now projecting 25bp rate cuts in October and November bringing rates to 2.5%. It also expects inflation to exceed the 3% top of the RBNZ target band over the coming year due to food prices, which is higher than the central bank forecast but like them it expects it to come down due to excess capacity.

- The institute had previously expected the cash rate to trough at its current 3%.

- NZIER notes that the pace of the recovery has been disappointing given the degree of policy easing this cycle. Increased global uncertainty is believed to have impacted household and business spending decisions.

- In addition, consumers are wary because of the weakness of the labour market where there has been job shedding. With only around half of mortgages repriced for lower rates, households should see more relief going forward which may support a pickup in consumption.

- See press release here.