JGBS: Futures Up From Lows, BoJ Outlook Remains Focus, PPI Tomorrow

JGB futures sit up from earlier lows, showing a modestly positive bias post the lunch time break. We were last 137.93, -.07 versus settlement levels. Earlier lows were at 137.70.

- Focus remains on the BOJ outlook. Out Tokyo based policy team noted earlier - MNI discusses the diminishing chances for a 2025 BOJ hike, see this link for more details.

- This comes after BBG reports yesterday that the central bank could still hike this year, potentially as soon as Oct, even amidst fresh political turmoil.

- The Reuters monthly Tankan survey painted a resilient backdrop for manufacturing. "Manufacturers' sentiment index +13 in September vs +9 in August" (Rtrs). It added, "...showed the manufacturers' mood index improved to 13 in September from 9 in August, marking a third month of increases and the highest reading since August 2022." The official Tankan report for Q3 is due Oct 1.

- The 5yr debt sale came and went without much fanfare, another positive for futures post the lunch time break. The bid to cover was 3.7, versus 2.96 at the August auction. The tail of the auction was also unchanged at 0.03.

- In the cash JGB space, back end yields are holding softer, while the front end is slightly softer. The 30yr and 40yr tenors are down 2bps in yield. The 10yr was last around 1.57%. The JGB 2/30s curve is flatter by around 3bps, last +239.5bps.

- Tomorrow on the data front, we have the BSI industry and manufacturing surveys, along with the August PPI.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

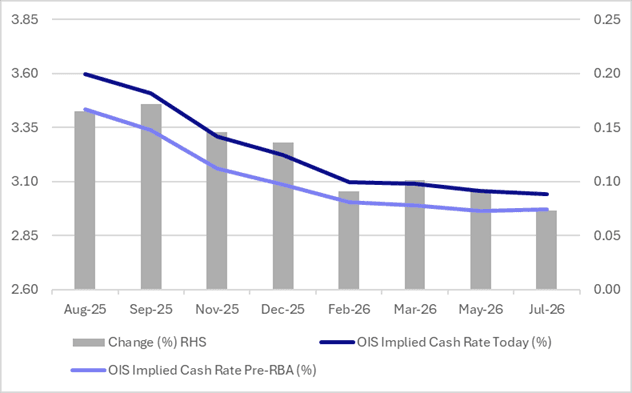

STIR: RBA Dated OIS Little Changed Ahead Of Tomorrow’s RBA Decision

At the time of writing, RBA-dated OIS pricing is little changed on the day across meetings ahead of tomorrow’s RBA Policy Decision.

- A 25bp rate cut this week is given a 97% probability, with a cumulative 62bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Notably, pricing remains 7-16bps firmer than levels before the July 8 RBA Meeting.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA (July)

Source: Bloomberg Finance LP / MNI

BONDS: NZGBS: Subdued Data Light Start To Week

NZGBs closed little changed, with benchmark yields flat t 1bp higher, after a subdued start to the trading week.

- Cash US tsys were closed during today’s Asia-Pac session, with Japan out for a holiday.

- Swap rates closed unchanged.

- With the next RBNZ meeting approaching (August 20), this week contains a number of high frequency releases that the MPC monitors and should give a sense for how the economy began Q3.

- July card spending is out Wednesday and while it is off its lows, growth has remained soft. There could be some payback in the month following the 0.5% m/m rise in June.

- On Friday, July monthly price series are released including food, travel, electricity and rents. Food and power price inflation have been trending higher while petrol and rents have been moderating.

- The July BNZ manufacturing PMI also prints on Friday. It returned to contractionary territory in May after five months signalling growth in the sector. In June, the pace of decline moderated with the index at 48.8 after 47.4.

- RBNZ dated OIS pricing closed unchanged across meetings. 23bps of easing is priced for August, with a cumulative 41bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond and NZ$250mn of the 2.75% Apr-37 bond.

NZD: Asia Wrap - NZD/USD Consolidates On A 0.59 Handle

The NZD/USD had a range of 0.5944 - 0.5962 in the Asia-Pac session, going into the London open trading around 0.5955, -0.02%. Risk has traded a little higher this morning, E-minis +0.20%, NQU5 +0.20%. NZD/USD bounced nicely off its 0.5850 support last week but depending on your view I would suspect sellers could return on any bounce back toward 0.6000/0.6050. For the moment firmly back in the 0.5850-0.6100 range looking for a catalyst to break and give clearer direction, US CPI tomorrow is an important input.

- "NZ'S LUXON: SEEING A TWO-SPEED ECONOMIC RECOVERY IN NZ, LAST THREE MONTHS HAVE BEEN CHALLENGING FOR ECONOMY. EXPECT FUTURE INTEREST RATE CUTS" - BBG

- MNI NZ: July Data Releases Ahead Of August RBNZ Meeting. With the next RBNZ meeting approaching (August 20), this week contains a number of high frequency releases that the MPC monitors and should give a sense for how the economy began Q3. July card spending is out Wednesday and while it is off its lows, growth has remained soft. There could be some payback in the month following the 0.5% m/m rise in June. On Friday, July monthly price series are released including food, travel, electricity and rents. Food and power price inflation have been trending higher while petrol and rents have been moderating.

- Kelly Eckhold(Westpac NZ) on LinkedIn - “Something to keep an eye on is the possibility that the reciprocal tariffs NZ got lumped with last week get removed by the courts. Sounds very possible as Trump is operating beyond his legal authority.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5920(NZD583m), 0.5930(NZD646m), 0.5960(NZD301m). Upcoming Close Strikes : 0.5825(NZD300m Aug 14). - BBG

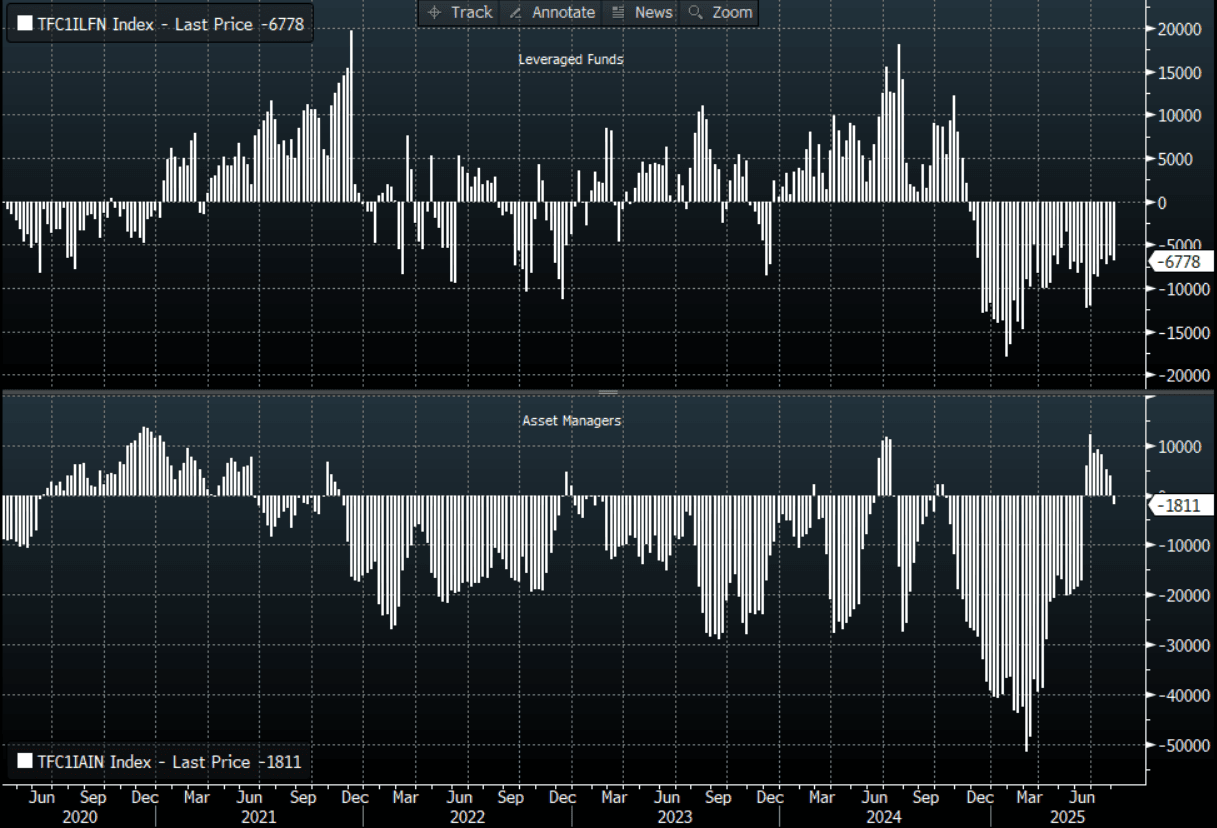

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short in the NZD -1811(Last +3903), the Leveraged community added to their shorts slightly -6778(Last -6250).

- AUD/NZD range for the session has been 1.0929 - 1.0960, currently trading 1.0940. The Cross continues to trade sideways after stalling towards the 1.1000 area once more. The range looks to be 1.0850-1.1000 for now.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P