JGBS: Futures Stronger Overnight With US Tsys

In post-Tokyo trade, JGB futures closed stronger, +11 compared to settlement levels, after US tsys finished modestly richer on Wednesday. US tsys finished off midday bests after slightly mixed messaging from the July FOMC minutes.

- A majority of participants judged the upside risk to inflation as the greater of these two risks, while several participants viewed the two risks as roughly balanced. "Almost all participants viewed it as appropriate to maintain the target range for the federal funds rate at 4.25% to 4.5%".

- MNI FED: MNI 2025 Jackson Hole Preview. Powell's Speech Unlikely To Clearly Signal September Cut: The key question for Friday's Powell speech is the degree to which he signals that the Fed is likely to resume the easing cycle in September. We think Powell will avoid an overtly dovish nod at this meeting, given how split the Committee appears to be on the need to cut rates.

- (Bloomberg) -- Japan's exports sustained their steepest drop in more than four years as US tariffs continued to weigh on global commerce, clouding the outlook for economic growth at a time when personal spending remains unsteady.

- Today, the local calendar will see Weekly International Investment Flows, S&P Global PMIs (P) and Machine Tool Orders alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Moderately Richer With US Tsys, RBA Minutes Due

ACGBs (YM +1.5 & XM +2.5) are moderately stronger after US tsys finished Monday with gains.

- Multiple factors helped US tsys extend their rally into a 4th day. However, a survey of various desks suggested a specific catalyst couldn't really be identified, with no tier 1 data or FOMC speakers (pre-meeting blackout period) on the docket.

- Cash ACGBs are 2bps richer with the AU-US 10-year yield differential at -8bps.

- The bills strip is stronger, with pricing flat to +2.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in August is given a 100% probability, with a cumulative 65bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar will be empty, ahead of the RBA Minutes for the July Meeting tomorrow. Governor Bullock is speaking at the Anika Foundation lunch on Thursday. Both will be monitored for further information on what lies behind the unexpected decision to hold and the central bank's thinking following the disappointing June jobs data.

- A new 21 October 2036 Treasury Bond is planned to be issued via syndication this week (subject to market conditions).

BONDS: NZGBS: Extends Post-CPI Rally After A Rally In US Tsys

In local morning trade, NZGBs are 2bps richer after US tsys finished Monday with gains.

- Multiple factors helped US tsys extend their rally into a 4th day, though a survey of multiple desks suggested a specific catalyst couldn't really be identified.

- A decline in oil prices helped bring breakevens lower, with reports of a potential Russia-Ukraine meeting applying downside pressure.

- Some cited reports of potential trade tension between the US and EU ahead of the White House-imposed Aug 1 deadline for a deal.

- NZ trade surplus narrowed to NZ$142m in June from a revised +NZ$1.082b in May.

- "Westpac noted that the decline in core inflation observed over the past year has stalled this quarter, but with most measures still a bit above 2%, inflation will need to be watched closely in the coming months, Westpac added." (BBG)

- Swap rates are 1-3bps lower, with a flatter 2s10s curve.

- RBNZ-dated OIS pricing remains little changed across meetings. 21bps of easing is priced for August, with a cumulative 38bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.0% Apr-29 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 5.0% May-54 bond.

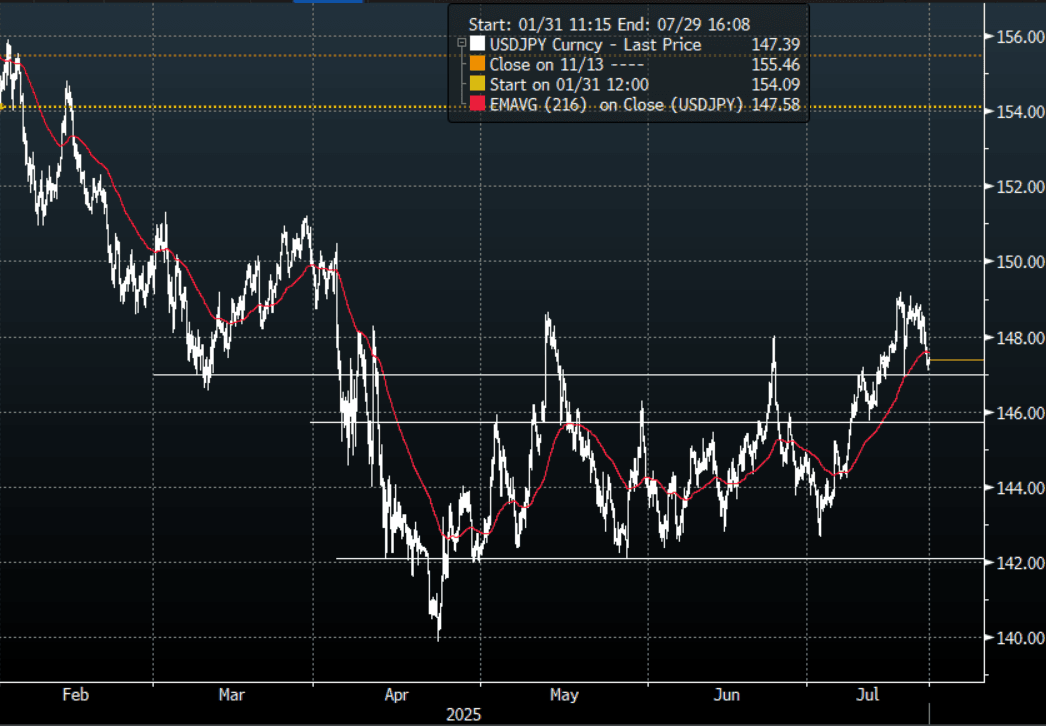

JPY: USD/JPY - Pulls Back To 147.00, Aided By US Yields

The overnight range was 147.08 - 148.30, Asia is currently trading around 147.35. USD/JPY continued to surprise the market by moving lower, one could surmise the election outcome had already been priced in and there were more negative scenarios that did not come to pass. The move lower in US yields provided further headwinds for the pair. The CFTC data showed the market is shifting its view on the JPY, with leverage funds just starting to build JPY shorts and Asset managers actively reducing their own. As a result I would expect some demand on dips first support is around 146.50/147.00 then 144.50/145.00.

- (Bloomberg) - “The yen is unlikely to get any lasting relief now that Japan’s upper house election is out of the way as negative real yields won’t be quickly addressed by the Bank of Japan.”

- “The yen rose but strategists warned of downside risks to the currency and JGBs due to the prospect of more government spending following PM Shigeru Ishiba’s election defeat.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.40($648m), 146.75($893m), 147.00($1.64b July 22).Upcoming Close Strikes : 147.50($1.45b July 24), 147.00($916m July 24) - BBG.

- CFTC data shows Asset managers starting to reduce JPY longs more aggressively +71610, while leveraged funds have started to build into a new short JPY position -12606.

- Data/Event : Trade Balance, Japan Weekly Investment Flow

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P