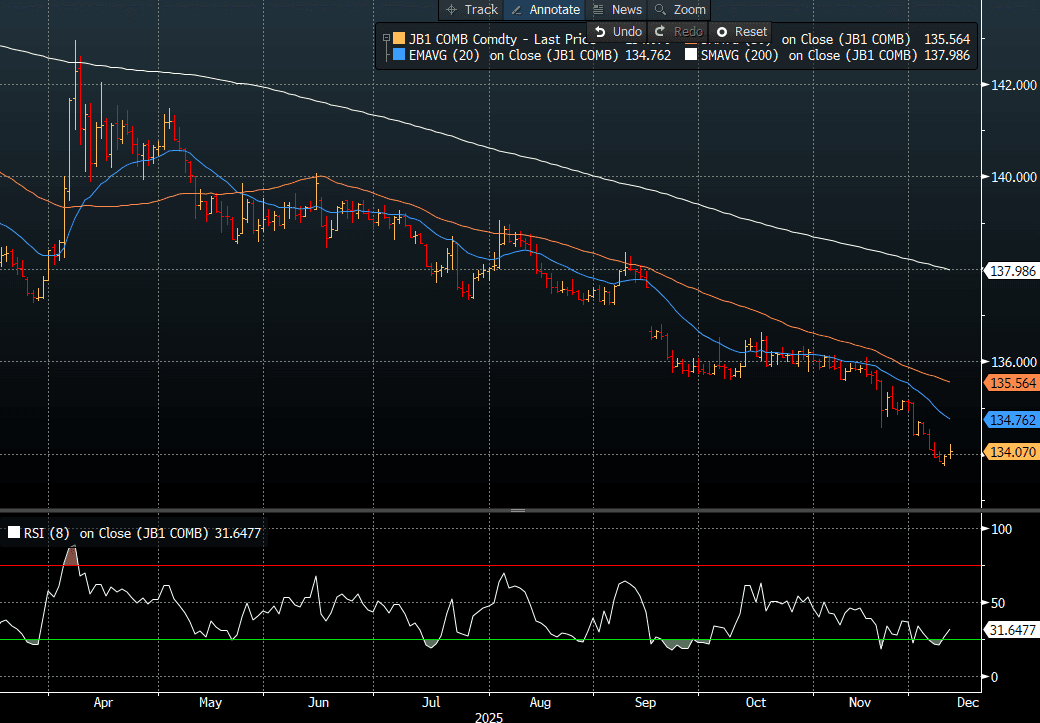

JGBS: Futures Stronger Overnight, Focus On The FOMC

In post-Tokyo trade, JGB futures closed stronger, +11 compared to settlement levels (see chart), despite US tsys closing near session lows on Tuesday ahead of today's FOMC decision.

- The US tsys move was initially driven by US job-openings data, which surprised sharply to the upside: October JOLTS printed at 7,670k (sa; cons. 7,117k), while September was also higher than expected at 7,658k. Both represent a notable jump from the 7,227k level seen in August, just before the government shutdown.

- MNI: Fed Dots To Show 1-2 Rate Cuts Next Year - Ex-Officials. A fragile consensus for a December interest rate cut from the Federal Reserve is likely to produce a negotiated pause for early 2026, with the centre of the FOMC projecting one to two more steps down toward neutral in 2026, former Fed officials told MNI.

- (Bloomberg) "Bank of Japan Governor Kazuo Ueda said the central bank is getting closer to attaining its inflation target, adding to signals that the BOJ may raise its interest rate at a policy meeting next week." (see link)

- Today, the local calendar will see PPI data.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Weekly Preview: Equity Divergence Reflects Views on Growth?

Download Weekly Preview Here

There performance of the onshore versus the offshore (Hang Seng) continues to diverge. Over the last month, the gains onshore have moderated and are barely positive whilst the Hang Seng has declined. This could potentially represent the two differing views on the China economy at present. The first being that the economic expansion is weak and likely to decline, the other being that the economy is in the early stages of a broader growth cycle.

OIL: Crude Trended Lower Last Week But Market Outlook Unclear

Oil was moderately higher on Friday but the overall trend was down over the week as concerns of the size of the expected market surplus dominated uncertainty related to Russian oil sanctions. These offsetting factors mean that crude tends to trade in a limited range. The IEA’s updated forecasts will be published in its monthly report released 13 November. It had been forecasting a record surplus for 2026.

- WTI rose 0.7% to $59.84/bbl after a low of $59.32. It reached $60.46 early in European trading and then trended lower as risk sentiment deteriorated. The benchmark was down almost 2% last week. Initial support is at $58.83 while resistance is $62.59.

- Brent was 0.5% to $63.70/bbl to be down 1.7% on the week. It made a high of $64.39/bbl before moving down to $63.23 trading between initial support at $62.84 and resistance at $65.98. The bear trigger is at $59.97.

- There are signs that the latest sanctions on Russia are have an impact with the diesel contract spread widening and some refiners in India/China looking for alternative sources. Increased demand for non-Russian crude could support or even increase benchmark prices despite expectations of excess supply.

- US President Trump has given Hungary a one year exemption from the US sanctions on Russia’s Rosneft and Lukoil, as “it’s very difficult for him [Hungarian PM Orban] to get the oil and gas from other areas”. According to Bloomberg, Hungary imports 90% of its oil from Russia.

CNH: USD/CNH Close To 20-day EMA, Awaiting Fresh Catalysts, Inflation Beats*

*corrected typo in final paragraph

USD/CNH tracks near 7.1265 in early Monday dealings, still close to the 20-day EMA support point (7.1240). The pair had fairly tight ranges to end last week, unable to get back under 7.1200, but upside moves into the 7.1300/7.1400 region drew selling interest. We are awaiting the next catalyst, although a slow grind lower is arguably the most likely outcome. CNH is expected to maintain a low beta with respect to broader USD shifts, but the CNY fixing bias should cap USD/CNH upside. Onshore USD/CNY spot finished up at 7.1221, while the CNY CFETS edged down slightly to 97.96, off recent highs. This is consistent with softer USD index levels.

- The China to global equity ratio edged higher to end last week, but USD/CNH doesn't look too out of sync with these shifts. US-CH yield differentials are up from recent lows, so we may have to see a turn lower, particularly at the short end for USD/CNH to re-test sub 7.1000.

- Over the weekend, we had Oct inflation data, which was stronger than expected. Notably, CPI rose 0.2%y/y, against a -0.1% forecast and -0.3% prior outcome. PPI deflation remained at -2.1%y/y, but was a slight improvement on the Sep outcome. On a monthly basis, CPI rose 0.2%, edging up from September's 0.1% growth. Core CPI, which excludes food and energy, rose 1.2% from September's 1.0%, marking the sixth consecutive month of increase and reaching its highest level since Mar 2024.

- The early Oct holiday period is thought to have boosted seasonal demand and aided higher price levels. We get more data at the end of this week around Oct activity figures. Consumer spending trends and property investment will be eyed.