JGBS: Futures Rangbound, Back End Bonds Seeing Demand, Tokyo CPI Tomorrow

Post the lunchtime break saw JGB futures dip modestly to 131.40, but we now sit back at 131.60, -.12...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: A$ Outperforming, AU-US Yield Spread Widens & Metals Rebound

While the US dollar index has range traded today, Aussie has outperformed the G10 with the yen underperforming. AUDUSD is up 0.25% to 0.6710, close to the intraday high, supported by a widening of the AU-US yield differentials with the 10-year spread at a cycle high and a rebound in metal prices. Risk-averse Aussie hasn’t been pressured by lacklustre equity indices.

- Aussie is also outperforming kiwi driving AUDNZD to 1.1549. The pair is currently up 0.1% to 1.1545.

- USDJPY has moved in a fairly narrow range as there haven’t been any comments from Japanese officials or data releases. The pair fell to 155.93 early in the session before rising to 156.34. It is currently up 0.1% to 156.14.

- AUDJPY is 0.3% higher at 104.78 but still below the December 29 high of 105.216.

- In terms of European currencies, NOK and SEK have outperformed while EUR and GBP are little changed.

- Equities across the region are generally slightly weaker with the Nikkei down 0.1% but Hang Seng up 0.5% and S&P e-mini flat. Oil prices are steady with WTI at $58.08/bbl. Copper is up 2.5% and silver +3.3% while iron ore remains around $105.50-106/t.

- Later the December FOMC minutes are published. In terms of data, US 13 December ADP employment, December MNI Chicago PMI, December Dallas Fed services and October house price data print. Also preliminary December Spanish CPI data are released.

OIL: Crude Unwinds Earlier Losses As Focus Returns To Geopolitics

Oil prices have unwound earlier losses following EIA data showing US crude and product builds in the week to 19 December. It has found support during today’s APAC trading from ongoing geopolitical risks after Russia put into doubt a peace deal over an alleged attack on a presidential residence, the US announced a strike on docks in Venezuela as its blockade continues and said it would attack Iran again if it resumed its nuclear programme. All are oil exporters.

- WTI has broken back above $58/bbl after it fell to $57.60. The benchmark is currently slightly lower at $58.05, close to the intraday peak of $58.15. The Brent February contract is flat at $61.92/bbl after reaching $61.99. Trading volumes in the contract are very light as it expires today.

- The EIA reported delayed US inventory data for the week ending 19 December. It showed a stock build of 0.4mn barrels which followed two consecutive drawdowns. Distillate inventories rose 0.2mn and gasoline 2.86mn, 6th straight weekly increases. Refinery utilization fell 0.2pp to 94.6%, 2.1pp higher than the same time in 2024.

- A Bloomberg survey showed that Saudi Arabia is expected to cut prices to Asia in February by up to 40c/bbl but may also leave them unchanged. January’s premium was reduced 40c/bbl. Ongoing OPEC and non-OPEC excess supply is pushing prices lower.

- Later the December FOMC minutes are published. In terms of data, US 13 December ADP employment, December MNI Chicago PMI, December Dallas Fed services and October house price data print. Also preliminary December Spanish CPI data are released.

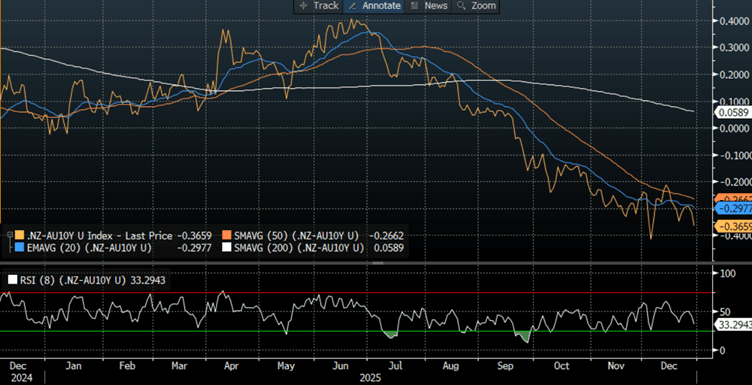

BONDS: NZGBS: Bull-Flattener With NZ-AU 10Y Diff Near Cycle Lows

NZGBs closed showing a bull-flattening of the 2/10 curve, with benchmark yields 2-6bps lower.

- The NZ 10-year outperformed ACGBs by ~6bps, with the differential returning to within striking distance of its cycle low of ~-40bps.

- Cash US tsys are slightly richer in today’s Asia-Pac session before the release of the Federal Reserve’s meeting minutes later Tuesday. The Fed will release minutes of its Dec. 9-10 meeting, where the central bank lowered the policy rate by 25bps. Fed Governor Stephen Miran voted against the decision in favour of lowering rates by twice as much.

- Swap rates closed 4-7bps lower, with tighter implied swap spreads.

- RBNZ-dated OIS pricing is slightly softer across meetings. No tightening is priced for February, while October 2026 assigns 23bps.

- The local calendar will be empty until Cotality Home Value data on January 1.

Bloomberg Finance LP