JGBS: Futures Off Earlier Highs, Govt Revises Up Debt Servicing Costs

JGB futures are holding a positive bias but at 132.89, +.04 versus settlement levels, we are comfortably off earlier highs (133.10). This keeps broader downtrends in futures intact, with recent Dec lows at 132.21 for March 2026 futures. The broader futures tone has been positive for US Tsys so far today, but moves have been tight amidst lighter volumes ahead of the Christmas break. In the cash JGB space, yields for the 10yr outright have edged back up above 2.04%, while the 30yr has edged back above 3.45%. Otherwise moves have been modest.

- News flow has centered on the fiscal outlook for the 2026 financial year. The debt servicing rate is expected to be at 3% for the 2026 financial year. This would be the highest rate since 1997 (when it was at 3.2%, per BBG) and reflects the surge in longer dated JGB yields.

- Via BBG and referencing debt servicing costs for the Japan government: "Based on the 3% assumed rate, total debt related spending, including interest payments, is projected to climb to a fresh high in the next fiscal year, exceeding the roughly ¥28.2 trillion allocated in the current budget. NHK reported debt servicing costs would increase to ¥31.3 trillion." This will be around one quarter of total spending per BBG.

- On the issuance side, via NHK: for the next financial year, issuance will be higher than the current financial year (¥28.6trln), with ¥29.6trln of new bonds expected to be issued in the 2026 financial year.

- Note that there will be a 2yr debt auction tomorrow, the last scheduled issuance before calendar year end.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Modest Gains on US Rate Cut Hopes (amended)

A modest rebound in major bourses today from last week's losses with the KOSPI in focus as with Japan out. The moves in USTs Friday resulted in cautious optimism for a December rate cut with the probability rising dramatically from a week ago. With all the focus on tech sector in Korea, a strong day for the industrials following the news that Korean ship builders secured large ship orders and the Seoul bus operator Chunil which is set to benefit from an announced redevelopment of its Seoul station . The tech sector is up also the usual suspects SK Hynix and Samsung gaining 2-3%. The Hang Seng delivered strong gains today with stock specific news the key drivers including the inclusion of new stocks and analyst recommendations. Onshore bourses all fell with some market commentary suggesting that the verbal spat between Japan and China over Taiwan was weighing on sentiment.

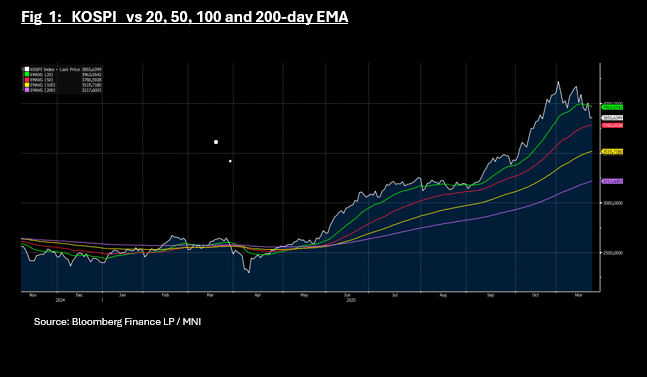

- The KOSPI is up just +0.30% as the Hang Seng led the way with gains of +1.4%. The onshore / offshore divergence was in full show with major onshore bourses all down from -0.15 - 0.60% Monday. The KOSPI has consolidated at the mid-point between the 20-day EMA and the 50-day EMA.

- SE Asia's bourses have a good start to the new trading week with the Jakarta Composite up+0.65%, SE THai up +0.25% whilst the FTSE Malay KLCI is flat on the day.

- As India opens to a new trading week the NIFTY 50 has had a quiet start up +0.06%. With valuations a top end of ranges, the hopes for further gains rests with a trade deal that local press suggest the Indian negotiators are close to achieving.

FOREX: BBDXY - USD Consolidates On A 1226 Handle

The BBDXY has had a range today of 1226.60 - 1227.70 in the Asia-Pac session; it is currently trading around 1226, +0.05%. The USD stalled toward 1230 heading into the weekend, this morning risk has opened strongly but with Japan out the reaction has been pretty muted. While the price remains above 1223/24 I would be skewed toward expressing a long, looking for a retest of the 1230-1240 area at some point. A move back through this support and the USD is back in the 1210/15-1230/35 range.

- EUR/USD - Asian range 1.1502 - 1.1521, Asia is currently trading 1.1520. The pair again consolidated around the 1.1500 area Friday night. On the day should risk manage to build on this open then the EUR could test the 1.1545-65 area, a break above here is needed for a retest of the 1.1650 area.

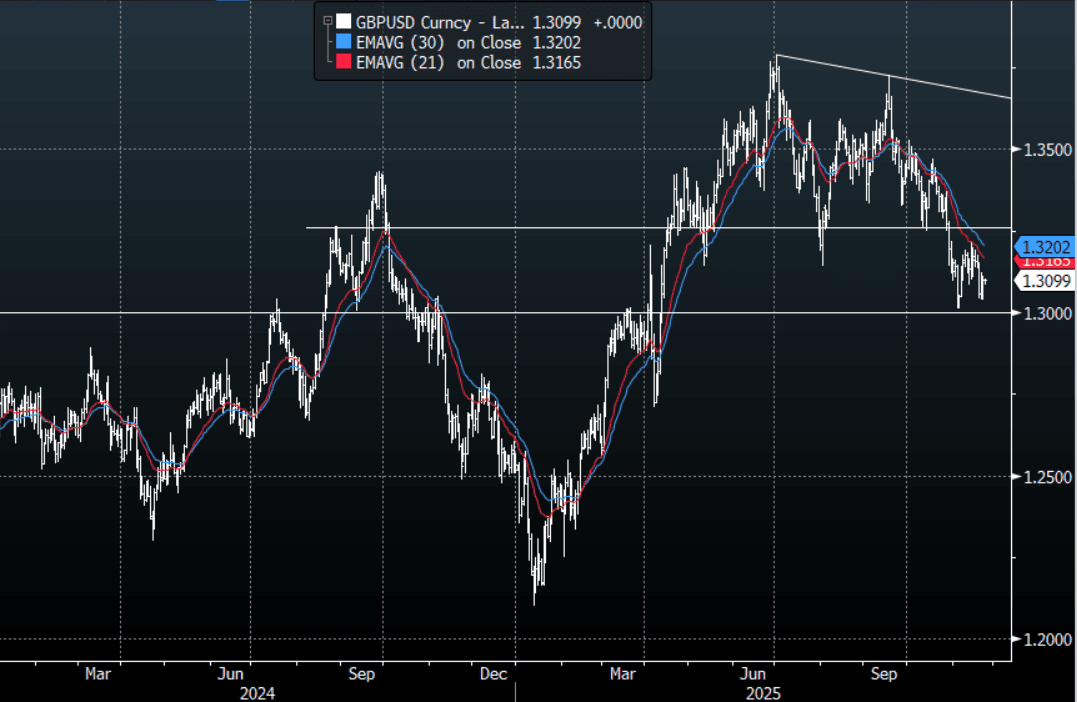

- GBP/USD - Asian range 1.3086 - 1.3105, Asia is currently dealing around 1.3100. The pair found solid demand again back toward 1.3000. I continue to favor fading rallies, as GBP looks to have put in a medium term top. Should the positive open for risk expand then we could test the resistance around the 1.3130-60 area, a break above here could signal better entry levels back toward the 1.3250 area. Lots of event risk this week with the budget presented on the 26th November.

- Cross asset : SPX +0.40%, Gold $4050, BBDXY 1226, Crude Oil $58.06

- Data/Events : Germany IFO Business Climate

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Steady Start, Futures Near Recent Lows, All Eyes On CPI on Wed

Aussie bond futures are little changed in a quiet start to the week, with Japan markets out (and no cash US Tsy trading) impacting. 3yr (YM) was last 96.22, no change from end Friday levels. 10yr futures (XM) were at 95.54, a touch higher for the session (+1.5bps). Both benchmarks remain close to recent lows. (96.135 from Nov 13 for the 3yr, and 95.485 (Nov 20) for the 10yr.

- The main focus this week domestically will be Wednesday's inflation data. This reference period for Oct, which will be the first complete release of full month CPI. A partial basket has been published for a while but the focus remained on the quarterly series as they contained updates for all components. RBA Governor Bullock said that the Board will continue to concentrate on quarterly CPI for now as it assesses the trends in the new monthly CPI and allows time for seasonal factors to emerge for the trimmed mean.

- In the cash ACGB yield space there is some slight softness, but outside of the 10yr yield (just under 4.45%), yield losses have been under 1bps. The 3yr is around 3.74% in latest dealings.

- The 3/10s curve is slightly flatter, last near +70bps.

- The local data calendar is empty until Wednesday's inflation print.