EUROPEAN FISCAL: French YTD Deficit Tracking In Line With Forecast

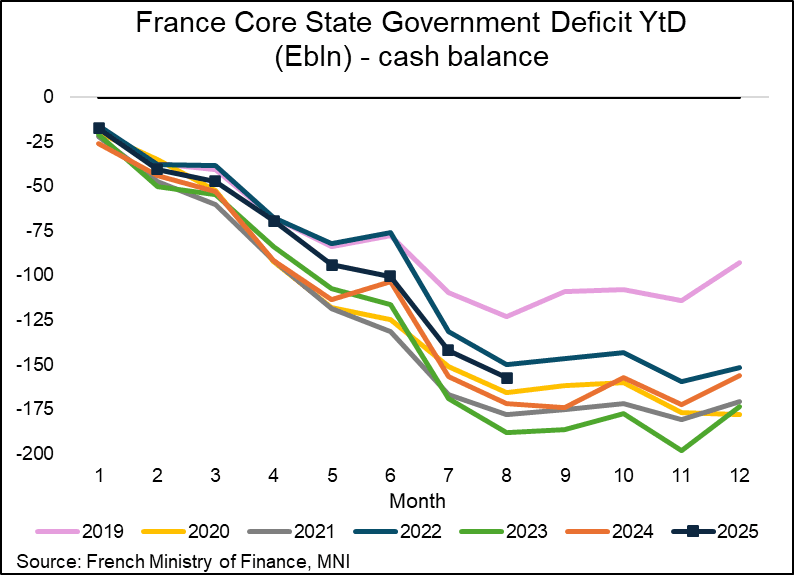

The French core state budget deficit tracking versus 2025 targets is broadly in line for both spending and receipts as a proportion of the year's running total, versus the past couple of years. The deficit YTD is running smaller than last year, but this was expected in the annual 2025 forecast. The French finance ministry's commentary notes both upward and downward dynamics contributing to the overall tightening of the deficit.

- The French core state YTD budget deficit widened to E157.5bn in August (vs E142.0bn July), an improvement of E14.5bn relative to E171.9bn in Jan-Aug 2024. The July-August change is broadly in line with previous years (widening E15.4bn versus E15.0bn in 2024).

- Net tax revenue stands at E199.6 bn (vs E187.8bn in 2024), an increase of E11.8bn, mainly explained by growth in "other tax" revenues (+E4.1bn in line with the end of the energy tariff shield, which reduced the figure since February 2023), net income tax (+E3.1bn) and net corporation tax (+E1.8bn). VAT is tracking almost exactly in line with last year (E67.4bn vs E67.3bn 2024).

- "Other tax" revenues are expected to be higher than last year, and may be pointing towards disappointment given that only 55% of the annual forecast has so far been collected, while this has been closer to 60% over the past couple of years. There is a higher target this year which may have impacted the seasonality (E84.1bn vs E65.4bn 2024, E66.3bn 2023).

- The proportion of corporation tax raised YTD (versus target) stands at 52%, higher than the 45% seen in Jan-Aug the last two years.

- PM Lecornu, like previous PMs, is keen to close the deficit in next year's budget plan (noting the 2026 deficit target of 4.7% of GDP). On Monday, Lecornu met with allies from the centre-right coalition, as a starting point for discussions on tax proposals. Having already ruled out a wealth tax, he insisted that "any debate on taxation must go hand in hand with a real reduction in public spending", reported by Le Figaro. He also said that short-term measures will only be acceptable if accompanied by medium- and long-term reforms, and reiterated the importance of combatting tax fraud.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT AUCTION PREVIEW: On offer next week

The DMO has announced it will be looking to sell GBP1.75bln of the 4.75% Oct-43 Gilt (ISIN: GB00BPJJKP77) at tis auction next Tuesday, September 9.

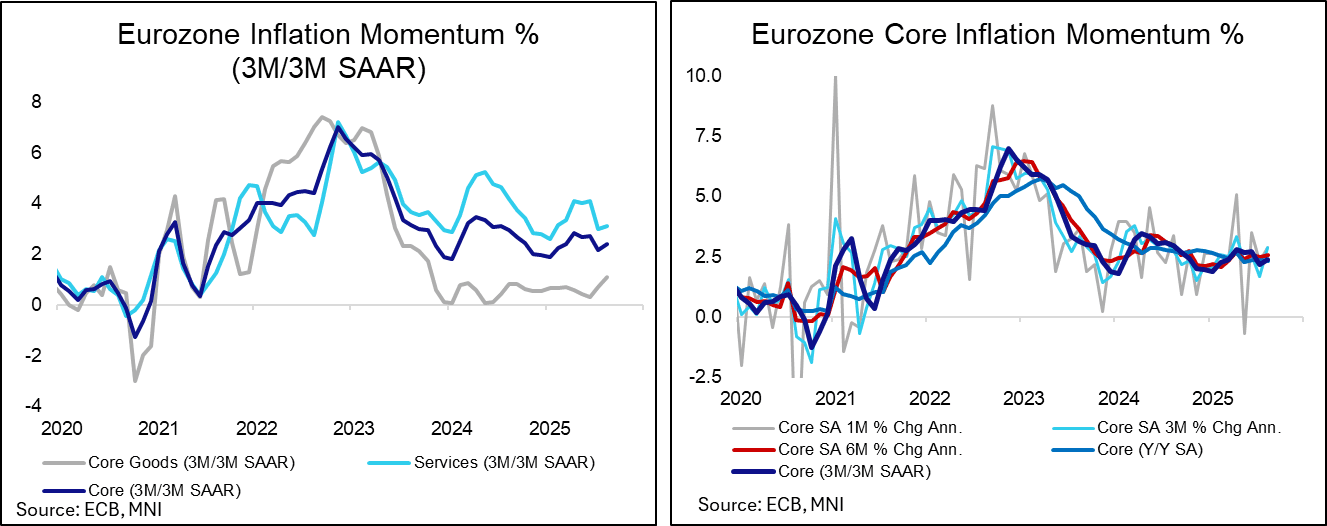

EUROPEAN INFLATION: Core Inflation Rises In Aug, But Not Enough To Concern ECB

Eurozone core inflation momentum increased in August, but remains below rates seen in April through June. As such, there shouldn’t be much to concern the ECB Governing Council, who will feel reassured by another deceleration in annual NSA services inflation.

- MNI’s inflation momentum series are calculated as a 3m/3m seasonally adjusted annualised rate using ECB seasonally adjusted flash data.

- In August, core inflation momentum rose to 2.39%, up from 2.17% in July but below the 2.72% seen in June. On a sequential basis, core prices rose 0.24% M/M (vs 0.19% in July, 0.27% in June).

- Services inflation momentum ticked up to 3.09% (vs 2.99% in July), but remains comfortably below the >4% readings seen the three months prior. Services prices rose 0.36% M/M SA, a solid rebound from the soft 0.14% last month but below June’s 0.41%.

- Core goods momentum rose for a second consecutive month to 1.10% (vs 0,70% in July, 0.31% in June), with sequential price increases essentially flat at 0.03% M/M.

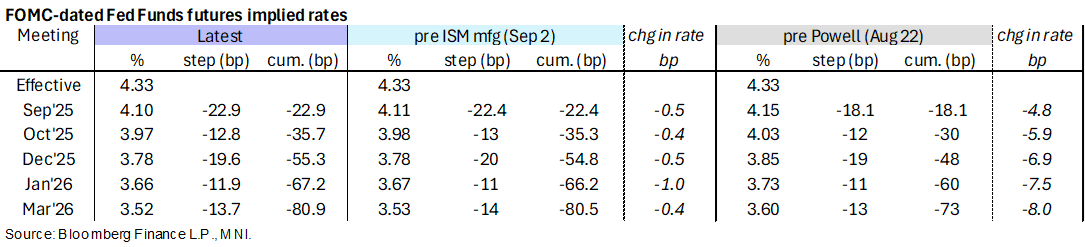

STIR: ISM Mfg Helps Extend Lift Off SOFR Lows

- There has been a contained dovish reaction to the ISM manufacturing report, with a small overall miss and then softer than expected prices paid & employment details vs robust new orders.

- Fed Funds implied rates are 0.5-1bp lower post-release for meetings out to 2026.

- Cumulative cuts from 4.33% effective: 23bp Sep, 35.5bp Oct, 55.5bp Dec, 67bp Jan and 81bp Mar.

- SOFR futures have rallied up to 2-2.5 ticks post-release in 2026-27 contracts, extending an earlier bounce off lows as they limit losses to 4 ticks from Friday’s settle (of which half came in yesterday’s holiday trading). As noted earlier, lifts off lows have been helped by a sharp pullback in WTI futures.

- The terminal implied yield remains in the H7, at 2.985% (+4bp from Fri) still a little above last week’s lows of ~2.95% were near the lowest closes since Oct 2024.