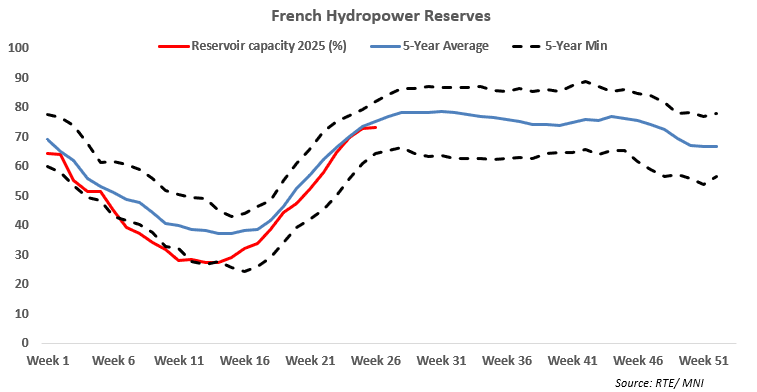

POWER: French Hydro Stocks Edge Up, Widen Deficit to 5-Year Avg

French hydropower reserves last week – calendar week 26 – slowed down the weekly increase to 0.5 percentage points to 73.2% of capacity. Stocks also widened the deficit to the five-year average, RTE data showed.

- Stocks slowed the weekly increase from 2.9 points the week before due to higher power demand, lower nuclear generation and dry weather in the hydro-intensive region.

- The deficit to the five-year average widened to 2 points, from 0.7 points the week before.

- The deficit to 2024 levels also widened to 8.8 points, from 6.5 points the week before.

- Power demand in France last week increased by 2.02GW to 46.24GW.

- Nuclear generation last week declined by 1.16GW to 36.1GW.

- French hydropower generation from pumped storage was broadly stable at 950MW, while output from reservoirs edged up by 127MW to 1.48GW. Run-of-river generation declined by 492MW to 3.73GW.

- Wind output in France last week was increased by 355MW to 3.3GW, while solar PV output declined by 769MW to 5.73GW.

- There was almost no precipitation in the hydro-intensive region of Grenoble last week.

- Looking ahead, the latest weather forecast for Grenoble for this week suggests again almost no precipitation in the region.

- Wind output in France for the remainder of this week (Tues-Sun) is forecast at 1.95GW to 8.11GW during base load. Solar PV output is forecast at 8.26GW to 11.08GW during peak load according to SpotRenewables.

- France’s hydro balance is forecast to end this week at -1.2TWh. The balance is forecast to widen to -419GWh as of 15 July, Bloomberg data showed.

- French nuclear generation capacity is forecast at 45.72GWh/h this week according to Reuters.

- Nuclear availability in France stood at 67% of capacity as of 30 June, RTE data showed, cited by Bloomberg.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (M5) Bear Cycle Remains Intact For Now

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.745 @ 14:57 BST May 30

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures rallied well on the RBA rate decision last week, reversing a small part of recent weakness. Recent price action pressured prices through to new pullback lows last week. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition. To the upside, a recovery of recent losses would shift attention to resistance at 96.207, a Fibonacci retracement point.

US-JAPAN: Trump To Deliver Remarks On Nippon Steel-US Steel Deal Shortly

US President Donald Trump is shortly due to deliver remarks in Pittsburgh, Pennsylvania, where he is expected to endorse Nippon Steel's takeover of US Steel. LIVESTREAM The announcement comes as the US and Japan remain far apart on a new bilateral trade deal.

- Trump said in a Truth Social message on May 23 that the planned partnership "will create at least 70,000 jobs, and add $14 Billion Dollars to the U.S. Economy," over the next 14 months.

- Semafor writes: “The US government will get a “golden share” in US Steel …, with the power to determine who sits on the board and control over production levels. It’s a dramatic provision that could lay out a roadmap for how deals get done in the Trump administration.”

- Japanese Prime Minister Shigeru Ishiba yesterday “expressed determination today to defend rules-based, free and multilateral trade systems and work on expanding the main Asia-Pacific trade group”, per AP.

- Ishiba said: “High tariffs will not bring economic prosperity. A prosperity built on sacrifices by someone or another country will not make a strong economy.”

- AP notes: “His comment comes as Japan’s chief tariff negotiator Ryosei Akazawa travels to Washington, D.C., for a fourth round of talks aiming to convince the U.S. to drop all recent tariff measures. So far Japan has not been successful in gaining U.S. concessions and is reportedly considering purchases of more U.S. farm products and defense equipment as bargaining chips.”

- Ishiba said after a call with Trump yesterday, “[we now] deeper understanding about each other,” but noted to reporters there has been no change to Japan’s position on the tariffs.

MACRO OUTLOOK: MNI US Macro Weekly: Jury’s Still Out On Q2 Downturn

We've just published our US Macro Weekly - Download Full Report Here

While the past week may be remembered for court decisions suspending the majority of the White House’s tariffs, it also brought further data evidence that the US economy did not fall off a cliff at the start of Q2.

- Consumer surveys (UMichigan, Conference Board) showed a downtick in consumer inflation expectations and improved sentiment, reflecting the US-China trade de-escalation on May 12.

- And while updated GDP data showed downwardly revised Q1 domestic demand, April personal consumption slowed but remained positive as underlying income growth remained solid.

- Likewise, though core durable goods orders retreated from Q1, a clear dropoff at the start of Q2 was not in full evidence. Regional Fed surveys signaled that activity stabilized in April-May, albeit at relatively weak levels, and labor market data pointed to incremental rather than sharp weakness.

- The point was underlined by the Atlanta Fed's nowcast for Q2 GDP growth which jumped to 3.84% on Friday from 2.18% in its May 27 update. Even if dramatic upgrade was due to a lower trade deficit in April as tariff front-running reversed, final domestic demand is still expected to be robust overall.

- Of course, things can change quickly: note Friday’s apparent re-escalation in US-China trade tensions and the temporary nature of the judicial tariff freeze (which in any case looks to be circumvented by the Trump administration), as well as the July “reciprocal” tariff negotiation deadline continuing to loom large.

- For the moment though, while uncertainty looks to be a constant, the data aren’t (yet) showing the degree of deterioration that had until recently been feared.

- Next week’s data highlights include key checkpoints for May, including ISM Manufacturing and Services surveys (which look likely to show some recovery versus April) and the US Employment report.

- Nonfarm payrolls growth is expected to moderate in May after a surprisingly robust 177k in April, with consensus currently around the 130k mark. The unemployment rate meanwhile is seen holding at 4.2% for what would be a third consecutive month.