CANADA: Foreign Min-PM Looking To Recalibrate Relations During China Trip

Jan-14 14:28

(MNI) London - Foreign Minister Anita Anand says that Canada and China have a "complex relationship"...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: US Cash Opening Calls

Dec-15 14:26

SPX: 6,883.1 (+0.8%); DJIA: 48,812 (+0.7%/+353pts); NDX: 25,436.0 (+0.9%).

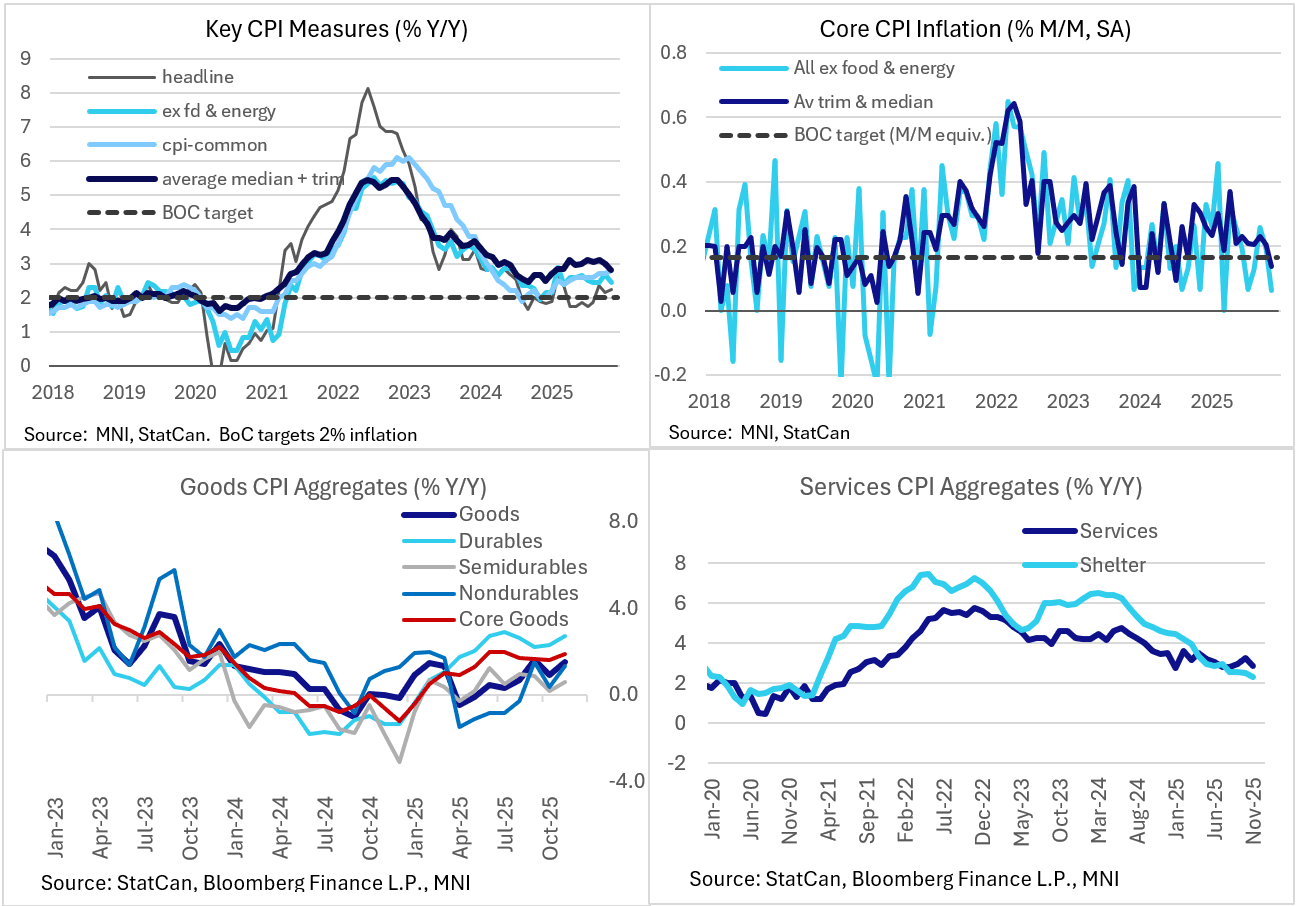

CANADA DATA: Services Deceleration Maintains Downside Pressure On Core CPI

Dec-15 14:25

The composition of November CPI was in line with MNI's expectations, with core items' moderation - led by services, offset by core goods' stubbornness - contrasting with an acceleration in food and energy prices.

- On the headline side, overall inflation came in basically as expected at 2.22% (2.3% consensus though lean had been toward the lower side of that unrounded), basically unchanged from 2.16% prior. And while energy prices saw less deflation (-5.1% Y/Y after -6.5%) as anticipated, the more significant surprise on the headline side was food which jumped by 4.2% Y/Y (3.4% prior), the highest since 2023 - led by grocery price inflation (4.7%). Overall food and energy ticked up to 1.6% Y/Y, after 0.6% prior.

- Within most core items however, moderation continued. Overall core goods prices continued to tick up, rising to a 4-month high 1.9% Y/Y (1.6% prior), but services prices printed a 3-month low 2.8% (3.2% prior).

- Shelter prices - around 30% of overall CPI, and seen as one of the key drivers of further CPI deceleration - ticked down to 2.3% Y/Y from 2.5% prior, lowest since February 2021 as there was notable disinflation in both owned (1.7% after 2.0%) and rented (4.6% after 5.1%) accommodation prices.

- Elsewhere, transportation (0.7% for a 2nd month) and recreation/education (12-month low 0.4% after 2.0%) - which total an additional 27% of CPI - kept a lid on overall inflation.

- They offset modest pickups in clothing and footwear (0.8% after -0.3%), household operations (32-month high 3.3% after 2.9%), and health and personal care (11-month high 3.0% after 2.5%), which total around 23% of the basket.

- We note that for overall goods prices (1.5% Y/Y after 0.9%, in a series that continues fluctuating month-to-month), there was an acceleration across categories: durables (4-month high 2.7% after 2.3%), semidurables (0.6% after 0.2%), and nondurables (1.3% after 0.4%) all picked up.

- While combined they are below 2% and thus it's still services keeping overall inflation at the high end of the BOC's comfort range, the pickup is notable in part because the Canadian government's decision in September to drop retaliatory tariffs on the US was seen to help moderate incoming goods price pressures.

EGB FUNDING UPDATE: Portugal 2026 Funding Plan

Dec-15 14:17

- E29.4bln financing needs for 2026 (versus E25.8bln 2025, down from the initial plan of E34.2bln).

- E24.0bln OT issuance E24.0bln OT issuance (versus E20.6bln for 2025, broadly in line with the E20.5bln originally expected).

- There are 9 auctions planned (8 in 2025) and 3 syndications expected (3 in 2025). Auctions are to be held on the second or fourth Wednesday of the month.

- E2.5bln expected from MTN transactions (none in 2025): "IGCP will issue notes under the new established ECP and EMTN Programmes subject to market conditions and interests that suit the overall financing strategy."

- Bills issuance to be a net E5.1bln increase - with BT auctions on the third Wednesday of the month (with the option to also use the first Wednesday of the month if needed).

- EU funding is expected at E2.2bln (E0.5bln in 2025) with retail debt increasing net E0.9bln (E3.2bln expected in 2025)

Related bullets

Related by topic

Canada

China

Mark Carney

Trade war

Tariffs

Donald Trump

US