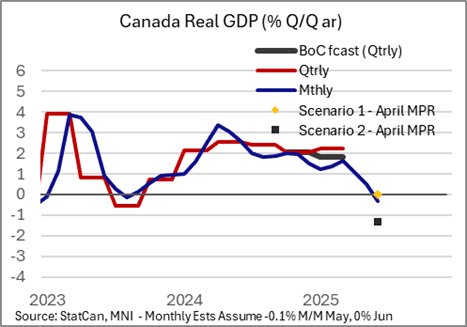

BOC: Forecasts To Be Less Pessimistic, Uncertainty Precludes Firm Guidance(3/4)

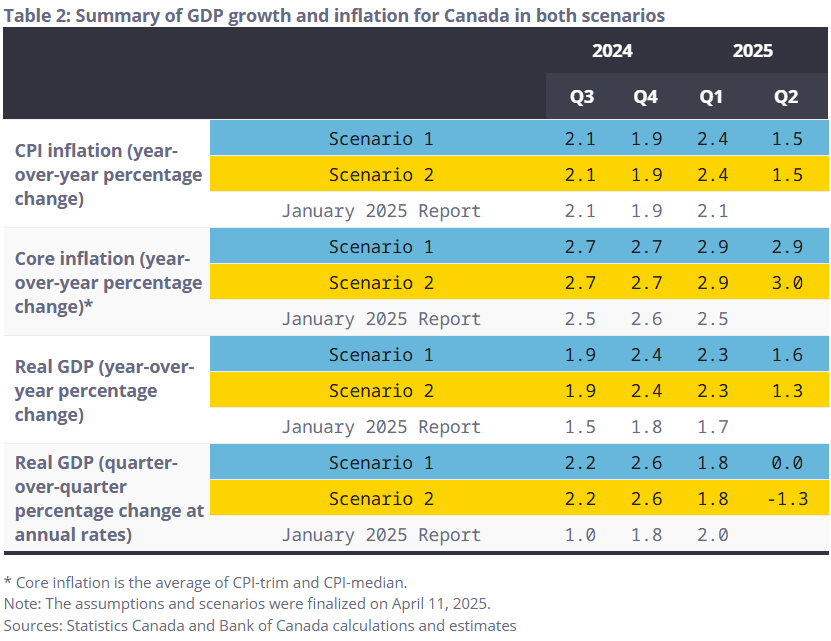

The prior Monetary Policy Report (April)'s summary table is below, showing two “scenarios”, one more pessimistic on the outlook than the other amid tariff threats. The BOC has signaled a preference to get back to a central forecast as opposed to dual scenarios, though it’s not likely that will happen in July.

- That’s because of multiple areas of uncertainty that could continue to warrant scenario-based analysis. First and foremost is US President Trump’s stated deadline of August 1 to reach a trade deal with Canada, absent which a 35% tariff rate on Canadian exports to the US has been threatened.

- We could add to such areas of uncertainty the federal government’s fall budget and various incoming data, but those are fairly ordinary areas of uncertainty and the US tariff situation is enough to keep the outlook extremely clouded.

- Given the above, we expect to see another dual-scenario outlook, albeit a more optimistic one than April’s on the activity front.

- As the aforementioned data since April suggests, this will include a less negative estimate for Q2 GDP with slightly higher core inflation. If they do publish a single, central forecast, this would be a surprise and suggest that the BOC has more confidence in its ability to make projections despite aforementioned uncertainties.

- The policy statement should reflect this better-than-expected economic activity evolution as well, suggesting as Gov Macklem has previously that reality has unfolded much closer to Scenario 1 than Scenario 2. There could be some note of continued elevation in core inflation metrics. In June the BOC noted "firmness in recent inflation data" which could stand, though "softer but not sharply weaker" economic activity could sound a little more positive this time.

- Once again, however, we do not expect any firm forward guidance given tariff uncertainty.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

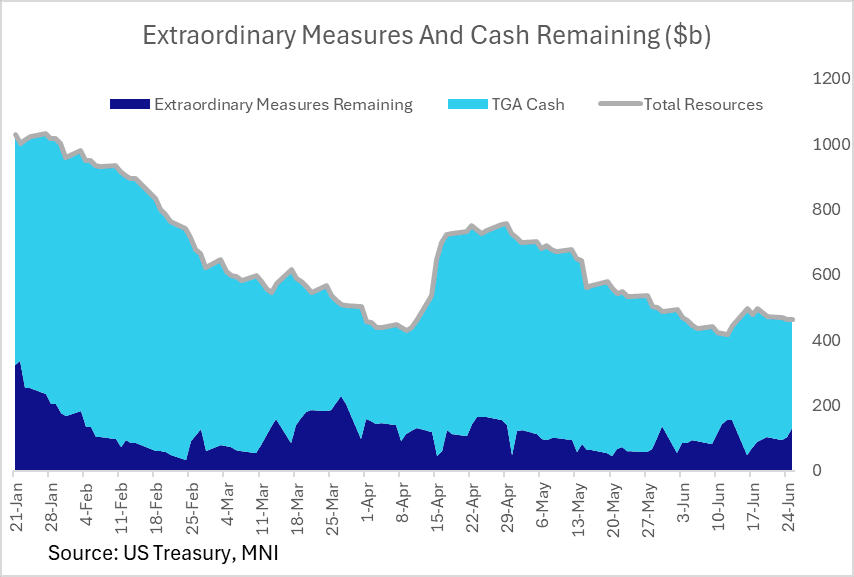

US FISCAL: Available "Extraordinary" Measures To Ward Off X-Date Pick Up

Treasury reported Friday that as of Jun 25 it had $130B in remaining "extraordinary" measures (of a total $378B available) to ward off an "x-date" of running out of resources before defaulting. That's the highest in 2 weeks.

- Combined with $334B cash as of Jun 25 (after a bit of a buildup after the mid-June tax deadline), that's a total of roughly $465B in total resources available.

- We noted earlier this week that Treasury told Congress that it was required to extend its debt issuance suspension period from Jun 27 to Jul 24, in effect prolonging the use of extraordinary measures while we await a resolution to the debt limit impasse, probably through the fiscal legislation currently going through Congress.

- Realistically, fiscal dynamics so far this year point to potential for Treasury to get into September without running out of cash + extraordinary measures. That seems to be the broad market expectation.

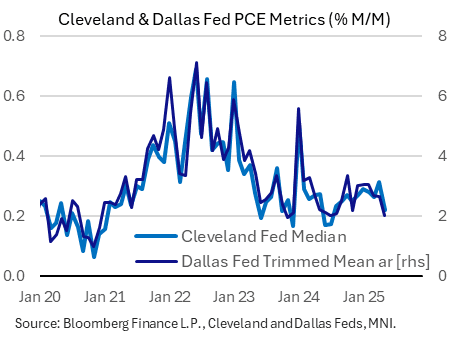

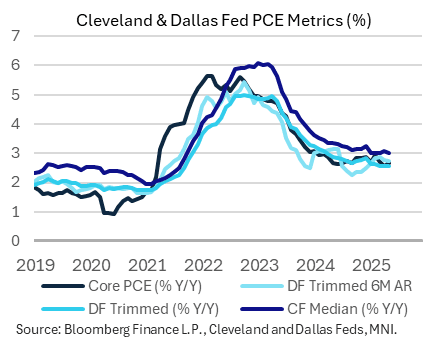

US DATA: Cleveland, Dallas Fed PCE Medians Show Progress But Still Above-Target

The Cleveland and Dallas Fed's median PCE metrics showed a notable drop in May. All indices suggest PCE inflation running above 2%, and higher than the actual core and headline PCE measures, but pressures appear to have cooled from a pickup in the early months of the year.

- The Cleveland Fed's median PCE measure came in at 0.22% M/M, a 10-month low after April's 15-month high 0.31%. This left median PCE at 3.01% on a Y/Y basis, down from 3.06% prior for a the joint-lowest (with Feb) since September 2021.

- The Dallas Fed's annualized median rate fell to 2.01%, from 2.65% prior for a 10-month low. The 6-month annualized rate edged lower to 2.74% (2.76% prior), a 4-month low, with the Y/Y rate ticking down to 2.55% from 2.56%, echoing the Cleveland Fed for the lowest reading since September 2021.

USDCAD TECHS: Pivot Resistance Remains Intact

- RES 4: 1.4111 High Apr 4

- RES 3: 1.4016 High May 12 and 13 and a key resistance

- RES 2: 1.3920 High May 21

- RES 1: 1.2710/3803 20- and 50-day EMA values

- PRICE: 1.3658 @ 16:23 BST Jun 27

- SUP 1: 1.3618 Low Jun 26

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

USDCAD has pulled back from its recent highs. The primary downtrend remains intact and short-term gains appear to have been corrective. Key support and the bear trigger has been defined at 1.3540, the Jun 16 low. Clearance of this price point would resume the downtrend. Any reversal higher would instead signal scope for a stronger retracement. Pivot resistance to monitor is at the 50-day EMA, at 1.3803.