CANADA DATA: Expected November Retail Sales Jump Offsets Soft October

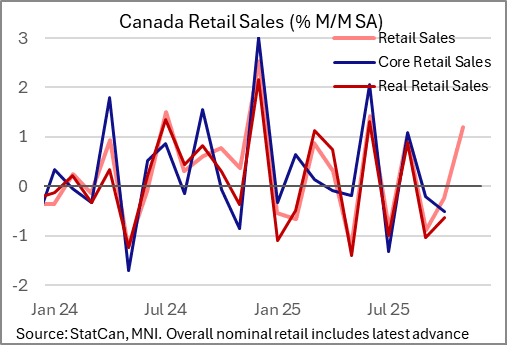

Friday's Retail Sales release from StatCan was mixed, with a third sequential decline in 4 months in October offset by expectations of a strong rebound in November. It will reinforce expectations for a negative October GDP print on Tuesday (-0.3% M/M expected, after +0.2%) but probably won't garner much attention from the BOC given the volatile nature of the series.

- Sales came in on the weak side of expectations in October, falling 0.2% M/M vs the advance estimate / consensus of a flat growth reading. Additionally, prior was revised down to -0.9% (was -0.7%), with the overall value of retail sales at 5-month lows. "Core" ex-autos/gasoline sales fell 0.5% (after a 0.2% fall), with volumes down 0.1% (after -1.0%). Breadth was mixed, with 4 of 9 subsectors seeing declines.

- But the report wasn't quite as bad as the headline statistics. The drop in core and headline was led by food and beverage retailers (-2.0% M/M) which in turn was due to sectoral labour disruptions in BC fueling a 10.6% drop in beer, wine and liquor sales.

- And November's advance estimate is +1.2% M/M, which would be the strongest monthly reading of the year.

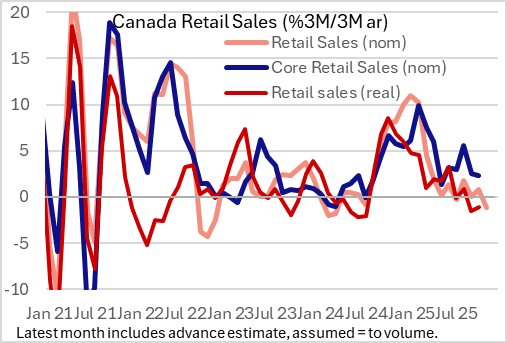

- Retail volumes contracted by 1.1% 3M/3M annualized in October, and that's only likely to weaken further even with a strong November monthly reading given a negative base effect from September. However that base effect should drop off as we head into 2026, barring a relapse in December.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post-Oct FOMC Minutes React

- Treasuries pared gains then rebound - still hold to narrow range after the October FOMC minutes showed "strongly differed" rate cut opinions.

- Currently, the Dec'25 10Y contract trades +2 at 112-27 (112-29 high). Resistance above at the 113-02 level in Treasuries, an area of congestion since Nov 5, remains intact.

- A clear breach of this hurdle would be a bullish signal and suggest scope for a climb towards 113-18+, the Oct 28 high. A breach would also cancel a short-term bearish theme. For bears, attention is on 112-10+, the 100-DMA and 112-06, the Sep 25 low. Trendline support also lies at 112-06+.

- Bbg US$ index continues to climb: +5.68 at 1225.11; SPX eminis firmer: +18 at 6857.75 - eyes on Nvidia earnings after the close.

MNI: mni: FED MEMBERS STRONGLY DIFFERED ON DEC CUT-MINUTES

- MNI: FED MEMBERS STRONGLY DIFFERED ON DEC CUT-MINUTES

- FED: SEVERAL PARTICIPANTS SAW DECEMBER CUT AS APPROPRIATE

- FED: MANY SUGGESTED KEEP RATES STEADY FOR REST OF YEAR

- FED: MOST SAW FURTHER CUTS LIKELY APPROPRIATE OVER TIME

- FED: MOST AGREED FURTHER CUTS COULD ADD TO INFLATION

- FED: ALL AGREED POLICY NOT ON A PRESET COURSE

- FED STAFF: RESERVES TO DIP TO QUITE LOW LEVELS AT TIMES

- FED STAFF BRIEFING ON SRF, CENTRAL CLEARING

EURGBP TECHS: Trend Set-Up Remain Bullish

- RES 4: 0.8893 2.000 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 3: 0.8875 High Apr 25

- RES 2: 0.8868 61.8% retracement of the 2022 - 2024 bear leg

- RES 1: 0.8865 High Nov 14

- PRICE: 0.8827 @ 17:24 GMT Nov 19

- SUP 1: 0.8783 20-day EMA

- SUP 2: 0.8769 Low Nov 10

- SUP 3: 0.8740 50-day EMA

- SUP 4: 0.8706 Low Oct 24 and a key support

The trend set-up in EURGBPis unchanged, it remains bullish and the cross is trading closer to its recent highs. A fresh cycle high last week confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 0.8868 next, a Fibonacci retracement. On the downside, initial key short-term support to watch lies at 0.8783, the 20-day EMA. A break of the average would signal scope for a deeper retracement.