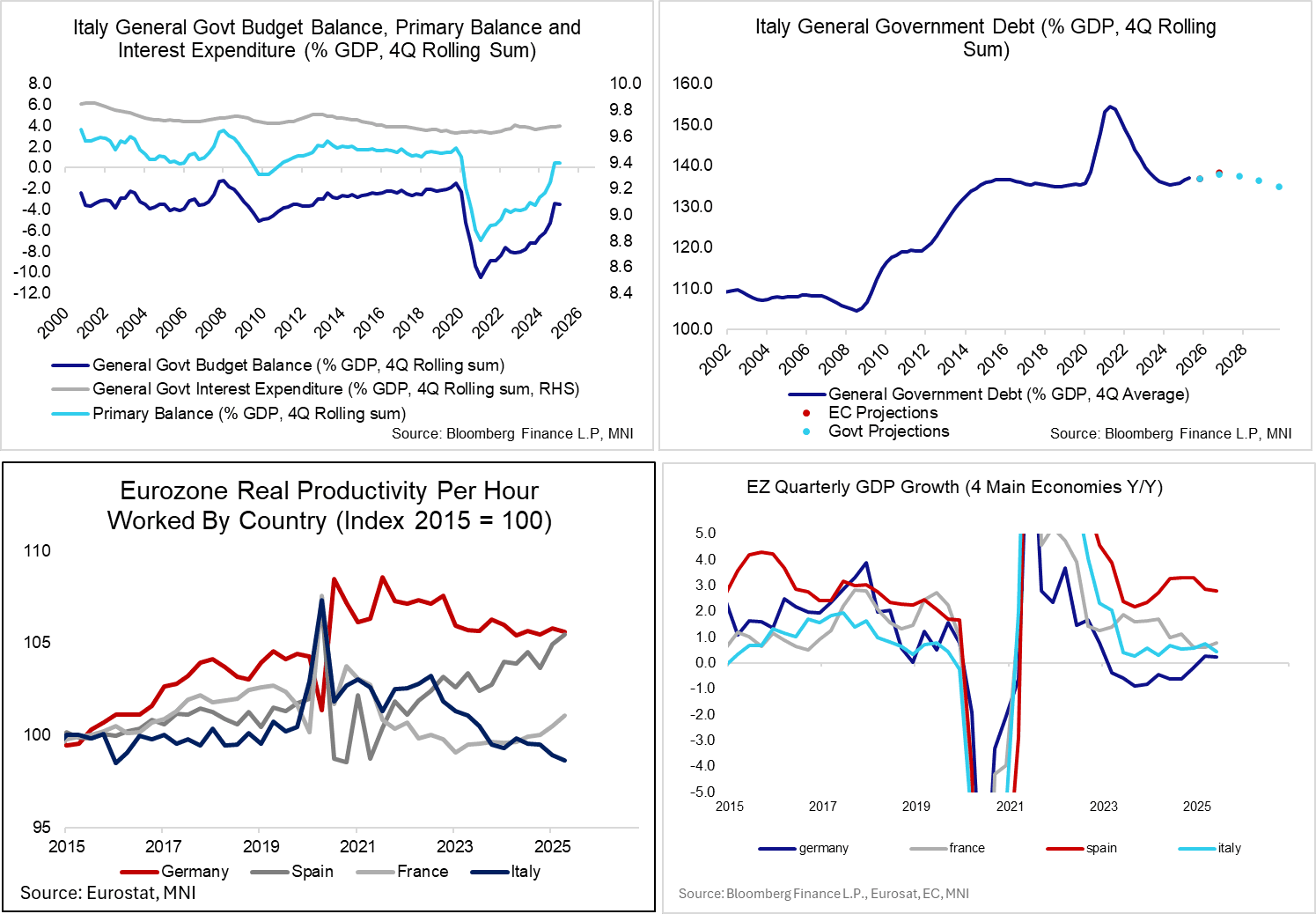

BTP: Domestic Macro/Fiscal Progress May Be Needed For Further Narrowing (2/2)

Sep-24 11:46

Additional Italy-Germany spread narrowing may require support from domestic macroeconomic/fiscal factors.

- Fiscal: Q2 Italian fiscal data is due on October 3. Recent fiscal consolidation has culminated in the first primary surpluses (on a 4Q rolling basis to GDP) since Q1 2020. Persistent primary surpluses are a necessary condition for the debt/GDP ratio to start easing in line with Government/EC projections from 2027. Looking ahead to the fiscal trajectory beyond this year:

- Bloomberg reported earlier this month that lower bond yields have created E13bln of extra fiscal space across 2025/26.

- Meanwhile, the Government is still trying to find a concrete way of raising revenue from the banking sector. It recently drafted plans to raise E1.5bln from banks through postponing tax deductions. This has historically been a politically difficult issue to navigate for Meloni.

- Furthermore, the FT reported this morning that the Government is considering a freeze in the retirement age of 67. The current retirement age is linked to life expectancy improvements, so has automatically crept higher over the past decade. Freezing the retirement age could put pressure on public finances, and worsen Italy’s existing demographic problems.

- Growth: Q2 real GDP growth was -0.1% Q/Q, and growth momentum has waned in recent quarters as the Superbonus tax credit tailwinds faded. However, analysts expect sequential growth rates to pick up in Q3 (0.1% Q/Q - flash print due October 30) and Q4 (0.2% Q/Q), which will be necessary for continued improvements in fiscal metrics as a % of GDP. That said, Italy’s weak productivity and demographic problems continue to limit potential growth rates.

- Ratings: Fitch upgraded Italy’s sovereign rating to BBB+ last week. S&P are due to provide a review on October 10th, but we don’t expect a ratings update given they already upgraded Italy to BBB+ in April. There’s more interest in Moody’s review on November 21. An upgrade from the current Baa3 rating appears likely, but we wouldn’t exclude a 2 notch upgrade to Baa1 to align with S&P and Fitch, particularly if the Q2 fiscal and Q3 flash growth data are encouraging.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup: Modest Put Volume

Aug-25 11:31

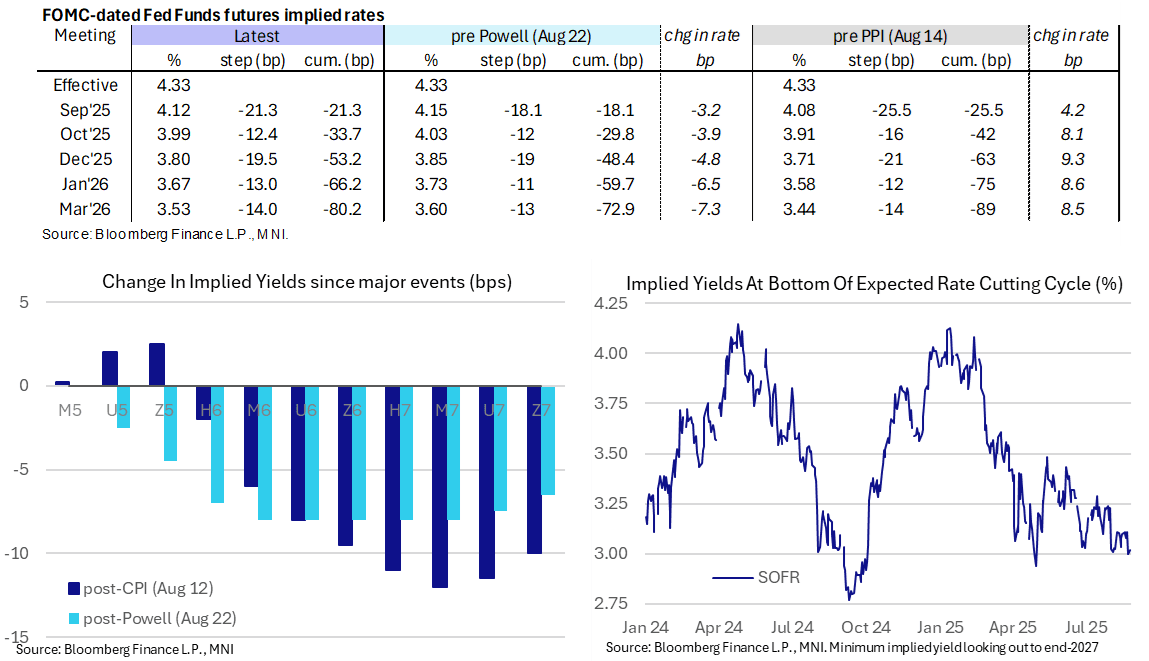

SOFR & Treasury options volumes rather modest ahead of the NY open - partly tied to London bank holiday today. Heavy futures volumes (TYU5 near 600k already) largely ties to Sep/Dec rolling, % complete over a third coming into the session. Underlying paring a small portion of Friday's post-Powell speech support. Un turn, projected rate cuts have cooled vs. late Friday (*) levels: Sep'25 steady at -21.2bp, Oct'25 at -34.1bp (-33.1bp), Dec'25 at -52.9bp (-55.1bp), Jan'26 at -65.6bp (-68.6bp).

- SOFR Options:

- over 11,100 SFRU5 95.93 puts, 7.0 last

- over 7,400 SFRU5 95.81 puts, 2.25 last

- 6,000 SFRU5 95.87 calls 5.75 last

- 4,000 SFRV5 96.06/96.18 put spds vs. 96.43 calls ref 96.21.5

- 7,600 SFRV5 96.25/96.37 call spds ref 96.22

- Treasury Options:

- 2,000 USX5 109/112 put spds

- over 5,700 TYV5 110 puts, 6 last

- over 3,700 TYV5 113 calls, 23 last

- 1,500 wk5 TY 111/111.5/111.75/112 broken put condors ref 112-04.5, exp Fri

- 2,000 FVX5 108/108.25/108.75 put trees ref 109-05

STIR: Late Fedspeak Could See Further Paring Of Reaction To Powell

Aug-25 11:23

- Fed Funds implied rates range from 1bp lower (Sep) to 2.5bp higher (Mar) from Friday’s close but still hold a large part of the dovish shift seen on Powell’s Jackson Hole speech.

- There’s still been a sizeable adjustment off dovish extremes though, with implied cuts to year-end at 53bp currently vs almost 58bp at one point on Friday (but 48bp pre-Powell).

- Recall that Powell on Friday noted that "with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance". The risks appear to have shifted since the July meeting as "downside risks to employment are rising”.

- Cumulative cuts from 4.33% effective: 21.5bp Sep, 33.5bp Oct, 53bp Dec, 66bp Jan and 80bp Mar.

- The SOFR implied terminal yield of 3.02% (SFRH7) is 2bp higher on the day after Friday’s close of 3.00% was the lowest since late April. It probes the well-kept range seen since the Aug 1 payrolls report of 125bp +/-5bp of cuts.

- Today’s Fedspeak could see some further ‘patient’ rhetoric, something generally seen last week prior to Powell, which could see some renewed focus on the “may” aspect of Powell’s remarks.

- 1515ET - Dallas Fed’s Logan (’26 voter, hawk) speaks at Banxico conference. This will be her first post-July FOMC comments having said on Jul 16 that she supports holding rates to keep cooling inflation and that the tariff impact won’t be clear until at least into the fall.

- 1915ET – NY Fed’s Williams (permanent voter) gives keynote remarks at Banxico conference. Speaking after the weak revisions of the Aug 1 payrolls report, he said Aug 2 that “modestly restrictive” policy is still needed and that the labor market is “still solid”. He sees economic growth rebounding in 2026.

OUTLOOK: Price Signal Summary - Bear Threat In Oil Futures Still Present

Aug-25 10:56

- On the commodity front, the medium-term trend condition in Gold remains bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend. The sideways direction that has been in place since the Apr peak appears to be a pause in the uptrend. A resumption of gains would open $3439.0, the Aug 23 high. On the downside, first key support to watch lies at $3268.2, the Jul 30 low. First support is $3311.6, the Aug 20 low.

- In the oil space, a bear cycle in WTI futures remains intact and recent short-term gains appear corrective - for now. A key support at $61.99, the Jun 30 low, has been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme.