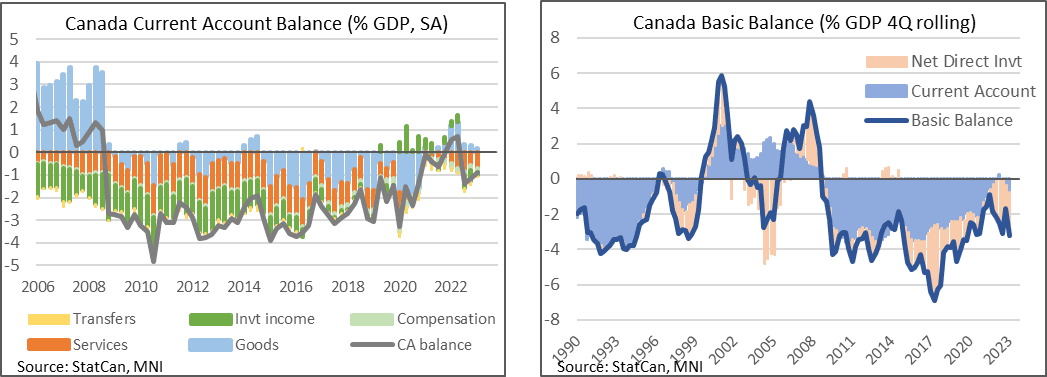

CANADA DATA: Current Account Deficit Clearly Smaller Than Expected In Q1

May-30 12:59

- The current account deficit was notably smaller than expected in Q1 at a seasonally adjusted C$6.1B (cons C$9.5B) after a downward revised C$8.1B (initial C$10.6B) in Q4.

- Prior revisions weren’t quite as favourable but left a trend improvement, with the current account deficit most recently peaking at 1.4% GDP in Q3, before narrowing to 1.2% GDP in Q4 and ~0.9% GDP in Q1 (vs 2-3% deficits pre-pandemic).

- The smaller deficit on the quarter came from smaller investment income outflows from -C$0.5B to -C$0.1B (with gains focused in direct investment and other income), whilst the goods & services balance saw a small deterioration from -0.3% to -0.5% GDP.

- Looking over a longer four-quarter rolling period though, the basic balance more sharply back from -1.7% GDP to -3.2% GDP, just exceeding the -3.1% GDP of Q3 for its largest deficit since 3Q19. It compares with the -3.9% averaged in 2019 or -4.9% through 2017-19.

- USDCAD has drifted almost 20 pips higher in the 30mins since the release despite the better than expected figures.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: US FI Rates, Equities Finish Strong Ahead Next Wed's FOMC

Apr-28 19:46

- After a rocky start, Treasury futures are trading broadly higher late Friday, short end lagging with curves running flatter, 2s10s -6.119 at -61.515. Heavy two-way flow noted after March Core PCE climbed 0.3% vs. 0.2% est, the 1Q ECI up 1.2% vs. 1.1%.

- Close to expectations, it’s technically the softest core PCE print since Nov’22 but clearly remains far stronger than the monthly rate consistent with the 2% target.

- Services eased from 0.38% to 0.23% M/M whilst Bloomberg's calculation of non-housing core services fell from 0.35% to 0.24% M/M for its softest since Jul'22.

- Treasuries marked session highs by midmorning (TYM3 115-12 (+20.5), trading sideways after a brief decline on stronger than expected Chicago Business BarometerTM, produced with MNI.

- The barometer improved by 4.8 points to 48.6 in April. This was the highest reading since August 2022. Nonetheless, the headline index remained sub-50, thus signaling an eight consecutive month of contractionary business activity.

- Focus turns to next Wednesday's FOMC policy announcement where a 25bp hike in could mark the end of the Fed’s hiking cycle. With rates above 5%, and sticky inflation fears offset by the tightening effect of banking sector woes, the FOMC is likely to move to a meeting-by-meeting policy beyond May, while retaining a bias toward further policy firming.

US STOCKS: Late Equities Roundup: Two Day Rally Off April Lows Into Month End

Apr-28 19:14

Stocks look to extend late session highs Friday, adding to Thursday's largest one-day rally since January 6 (+77.75 vs. +86.75). At the moment, DJIA up 221.63 points (0.66%) at 33983.68; S&P E-Mini Future up 28.5 points (0.69%) at 4175; Nasdaq up 61.3 points (0.5%) at 12188.54.

- There appeared to be no particular headline or catalyst for the support other than a reluctance to sell into the bounce off Wednesday's low for the month (SPX 4070.25) going into moth end. That, and generally positive quarterly earnings announced in the latest cycle.

- Friday's move higher exposes key resistance and the bull trigger at 4198.25, the Apr 18 high. Clearance of this level would confirm a resumption of the uptrend that started Mar 13 and open 4244.00, the Feb 2 high.

- On the downside, key short-term support has been defined at 4068.75, the Apr 26 low. A break would be bearish.

- Meanwhile, the Federal Reserve issued it's supervisory report on Silicone Valley Bank Friday, laying blame on the banks board of directors and management but is also critical of its own supervisors that the Fed says did not appreciate the extent of SVB vulnerabilities and did not take sufficient steps to ensure the bank fixed those problems quickly enough.

US OUTLOOK/OPINION: Macro Developments Since March FOMC - Labor [2/2]

Apr-28 19:05

- Released far more recently and well into the FOMC blackout, the Employment Cost Index data showed a trend of stabilization rather than further moderation that could begin to worry the FOMC.

- Specifically, the ECI increased slightly faster than expected in Q1 at 1.16% Q/Q non-annualized (cons 1.1) after an also upward revised 1.10% Q/Q (initial 0.97%) in Q4. Wages & salaries saw similar relative strength with 1.16% Q/Q after an upward revised 1.17%, with marginally more of an uptick in its private subcomponent at 1.21% Q/Q after 1.16% Q/Q.

- In annualized terms, the 4.7% for total ECI is down from 5.5% in 1H22 but importantly unchanged from 2H22 whilst private wages & salaries actually accelerated to 4.9% annualized vs 4.7% 2H22 av.

- This rates have recently shown no sign of further moderation, in contrast to the more pronounced easing in monthly AHE data from payrolls, and in turn are stabilizing at growth rates that require unusually elevated productivity growth to be consistent with the inflation target.

Trending Top

May-08 20:33