MNI US Macro Weekly: Labor Risks Averted, CPI Next

May-08 18:07By: Chris Harrison and 1 more...

USFederal ReserveUnemploymentPayrolls+ 4

Download Full Report Here

Executive Summary

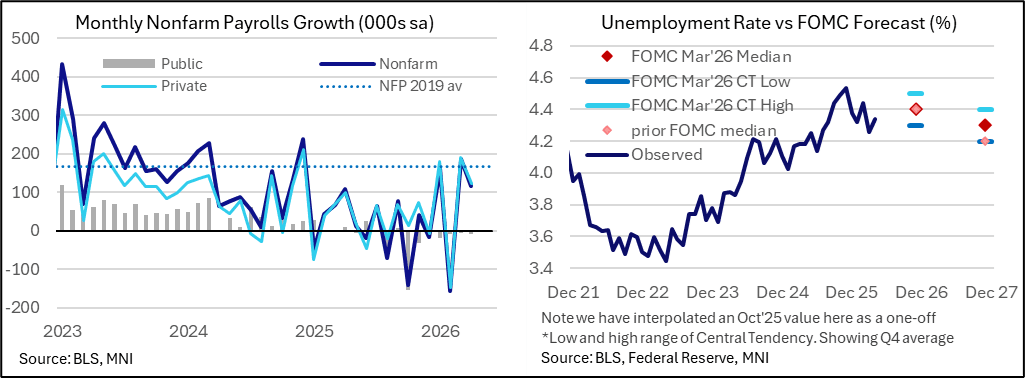

- This week’s key macro release was the April nonfarm payrolls report, where overall and private payrolls growth was again comfortably stronger than expected. Overall, recent jobs data should further focus the FOMC’s attention on inflation and less on downside risks to the labor market.

- Payrolls increased a seasonally adjusted 115k (sa) (Bloomberg consensus 65k) in September, with two-month revisions small on net at -16k, while private payrolls beat at 123k (vs bbg cons 75k) and left the six-month average for private payrolls growth at its strongest since Apr 2025. The rounded unemployment rate was steady at 4.3%, which the FOMC sees as relatively low, and little changed from recent months.

- If there was a dovish area, average hourly earnings were one of the softest areas of the report and AHE measures at 3.6-3.7% Y/Y continue to show little inflationary impact from the labor market.

- Beyond labor, business and inflation signals were mixed. ISM services was very close to expectations in April at 53.6 (cons 53.7) but details were on balance dovish relative to expectations (prices paid unchanged at 70.7 vs cons 73.5; new orders 53.5 vs cons 57.3; employment 48.0). The S&P Global US services PMI printed 51.0 in Apr final and highlighted “the first reduction in demand since April 2024” amid the war in the Middle East and higher inflationary pressures.

- The NY Fed consumer survey saw an uptick in 1Y inflation expectations to 3.64% (highs since Sep 2023) and 3Y to 3.15% (highest since Jul 2022), while Manheim used vehicle prices slipped -1.6% M/M in April ahead of next week’s April CPI report.

- The Fed rate path currently sees little net change over the week compared to huge swings in recent weeks, awaiting an Iranian response to the US 14-point plan. There have still been sizeable moves throughout the week, ending with a neutral rates outlook to end-2026 vs more than 10bp of hikes on Monday.

- Fedspeak also stayed hawkish-leaning, with Kashkari reiterating “it may well be that the next move might need to be up in interest rates, I just don't know,” and Musalem stressing “very plausible scenarios” for policy to be on hold “for some time,” cuts, or “higher interest rates,” with inflation “meaningfully above our target of 2%,” and “The tailwinds are larger than the headwinds.”

- What to watch next week: data focus will firmly be on a latest round of inflation updates (CPI Tuesday, PPI Wednesday) after Friday’s nonfarm payrolls report for April ruled out downside risks to the labor leg of the Fed’s dual mandate. Consensus looks for headline CPI 0.6% M/M sa (energy-driven) with core 0.3% M/M sa. The calendar also includes existing home sales (Mon), Retail Sales / Jobless Claims / Import & Export Prices (Thu), and Industrial Production (Fri), alongside multiple Fed speakers (incl. Williams, Goolsbee, Collins, Kashkari, Hammack, Barr).