MNI US Employment Insight: Downside Labor Risks Dissipating

May-08 16:29By: Tim Cooper and 1 more...

Employment

Hidden PDF

EXECUTIVE SUMMARY:

Nonfarm and private payrolls growth was comfortably stronger than expected in April and sees solid recent trends considering estimates for the breakeven pace of payrolls growth have drifted towards zero. Overall, recent jobs data should further focus the FOMC’s attention on inflation and less on downside risks to the labor market.

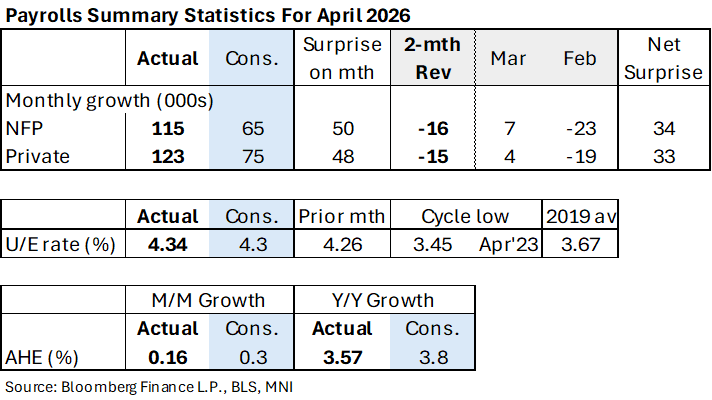

- Payrolls increased a seasonally adjusted 115k (sa) compared to Bloomberg consensus of 65k and a primary dealer median of 70k.

- Two-month revisions were small on net at -16k although still managed to further boost the volatility seen in recent months. Payrolls growth has now swung from 160k in Jan (not affected by today’s release) to -156k in Feb (vs -133k prior) and 185k (vs 178k prior) before today's 115k in April.

- Private payrolls told almost exactly the same story, with a solid beat (123k vs bbg cons 75k) supported by a typically strong contribution from healthcare sectors although other industries also saw solid growth compared to recent year standards; two-month revisions were only -15k. The six-month average for private payrolls growth is at its strongest since Apr 2025.

- There was some evidence of both weaker labor market supply and demand at play in the Household report, though most figures were relatively steady. The unrounded unemployment rate printed 4.337%, an uptick from the 9-month low 4.256% in March but just a 2-month high and in line with expectations for a steady 4.3% (range 4.2-4.4).

- Weakening in greater fashion was the U-6 "underemployment" rate which rose to 8.2% from 8.0% for a 4-month high, though still well below the recent high of 8.7% seen in November.

- Overall April’s Household survey won't alter the narrative of the unemployment rate as having “changed little in recent months”, as expressed by Chair Powell in the April FOMC press conference who also said that "4.3...that's a low rate. That's pretty close to mainstream estimates of the natural rate."

- Average hourly earnings were one of the softest areas of the report albeit with a caveat that average hours worked increased. There was another caveat that non-supervisory employees saw stronger wage growth. That said trends for each of these main AHE measures at 3.6-3.7% Y/Y continue to show little inflationary impact from the labor market against a backdrop of strong productivity.

- There were only modest dovish adjustments in US rate markets on net in the wake of the NFP report, with initial hawkish reaction to the firmer-than-expected headline reading (which was accompanied by positive revisions to the month prior) countered by softer-than-expected AHE figures and higher-than-expected underemployment. FOMC-dated OIS showed 3.5bp of easing through September vs. 2.5bp pre-release, before pricing 6.5bp of hikes through March vs. 9.0bp pre-release.