EURJPY TECHS: Corrective Cycle

* RES 4: 188.65 3.236 proj of the Oct 17 - Oct 30 - Nov 5 price swing * RES 3: 187.99 Bull channel t...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Mar'26 30Y Ultra-Bond Sale

- -2,000 WNH6 118-13, sell through 118-14 post time bid at 1443:28ET, DV01 $364,200.

- The 30Y Ultra-bond contract trades 118-10 last (-6)

FED: Varying FOMC Opinions On Labor, Inflation Outlooks And Risks (2/3)

The Minutes showed there was unanimous agreement on changing the December Statement language to reflect that "in considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee would carefully assess incoming data, the evolving outlook, and the balance of risks.... All members agreed that the post-meeting statement should relay this judgment about additional rate adjustments". Recall that the previous statement's forward guidance started with "In considering additional adjustments". This Statement change was seen as maintaining the overall easing bias while suggesting that the consecutive pace of reductions is set to slow in 2026.

- The division in the Committee on the path ahead is unsurprisingly about varying outlooks for inflation and the labor market, and the balance of risks.

- On inflation, the majority outlook is reflective of a preponderance of opinion in favor of further easing ("participants generally expected inflation to remain somewhat elevated in the near term before moving gradually to 2 percent"), with "many" seeing the tariff impact on core goods inflation waning, a "majority" expecting "continued disinflation in housing services", and a "few" seeing "continued disinflation in core nonhousing services".

- On the risks to inflation: "participants generally judged that the risks to inflation remained tilted to the upside, although several participants commented that they considered these upside risks to have decreased. Some participants highlighted the risk that elevated inflation might prove more persistent than expected." In stating their concerns over a December cut, "several participants pointed to the risk of higher inflation becoming entrenched and suggested that lowering the policy rate further in the context of elevated inflation readings could be misinterpreted as implying diminished policymaker commitment to the 2 percent inflation objective."

- And on the labor market: "Most participants remarked that some of the most recent indicators of labor market conditions, including survey-based measures of job availability or reports of planned layoffs, pointed to continued softening. Some participants noted, however, that other indicators, such as weekly initial unemployment insurance claims and measures of job postings, suggested more stability". The latter sentiment was reflected in the judgment on rates, in which "A few participants judged that lowering the federal funds rate target range at this meeting was not justified because data received over the intermeeting period did not suggest any significant further weakening in the labor market" - the latter of which appears to be a key basis for supporting further cuts. However, "participants...judged that downside risks to employment had risen in recent months."

- Overall, "participants generally assessed that, under appropriate monetary policy, the labor market likely would stabilize next year but noted that their outlook for the labor market was still quite uncertain, especially amid the delays in the release of government data. Most participants judged that risks to the labor market remained tilted to the downside."

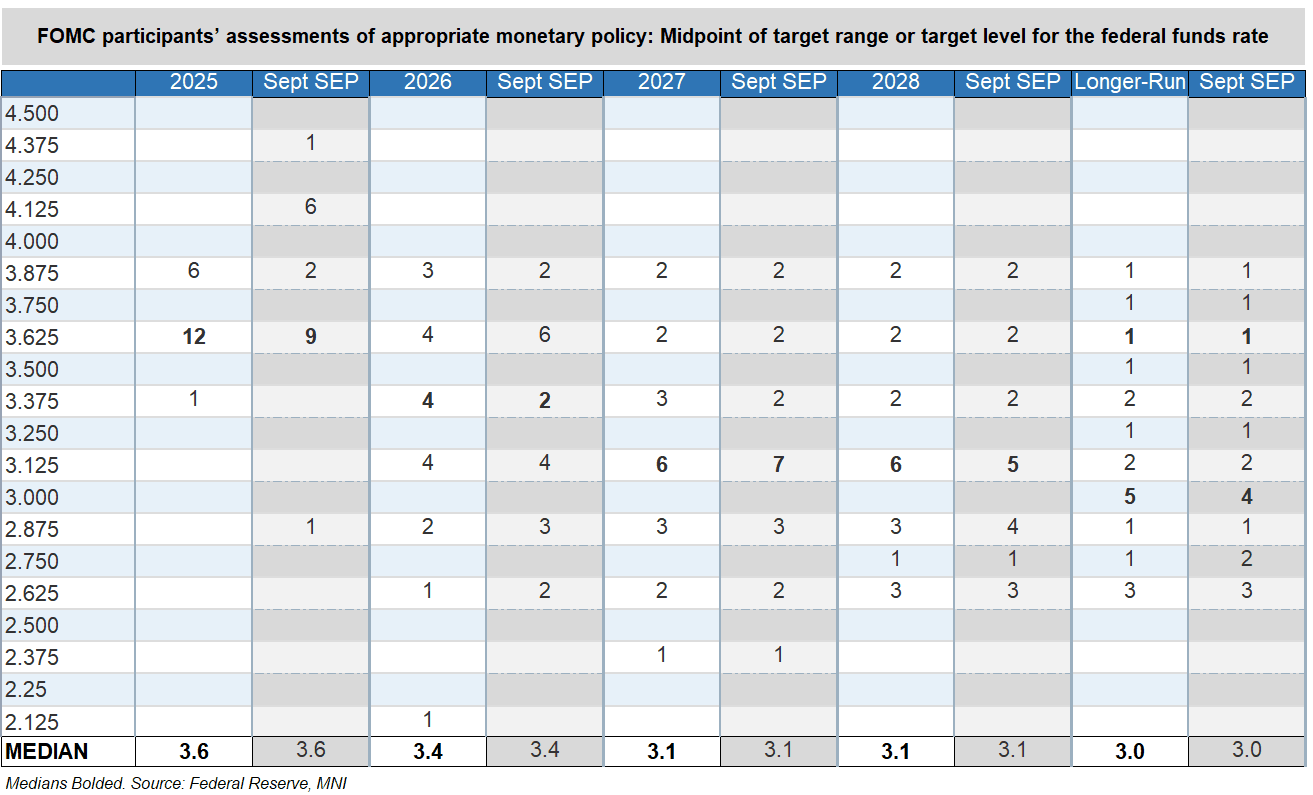

FED: December Minutes Show A Solid (But Narrow) Majority Eyes Further Cuts (1/3)

The key paragraph from the December FOMC meeting minutes (link here) indicates (as did the meeting Dot Plot) a sizeable minority of members seeing no further easing through end-2026, but a base case among a solid if narrow majority that further limited cuts would ensue if the data cooperate.

- It was: "Most participants judged that further downward adjustments to the target range for the federal funds rate would likely be appropriate if inflation declined over time as expected. With respect to the extent and timing of additional adjustments to the target range for the federal funds rate, some participants suggested that, under their economic outlooks, it would likely be appropriate to keep the target range unchanged for some time after a lowering of the range at this meeting." But "all participants agreed that monetary policy was not on a preset course".

- The 25bp cut itself was a finely-poised decision. While "most" of the 19 FOMC members backed a cut, "some" (which in Fed-speak is less than "Many" but more than "Several") members preferred to keep the target range unchanged.

- Keeping in mind that that 6 members pencilled in no cut in their Dot Plot, an additional "few" who could have supported a hold implies that the Committee was evenly split on a rate cut vs a hold coming into the meeting: "A few of those who supported lowering the policy rate at this meeting indicated that the decision was finely balanced or that they could have supported keeping the target range unchanged."

- Indeed the "some" who saw rates on hold for "some time" after this meeting is consistent with the 7 members who pencilled in rates at or above the current 3.6% Fed funds midpoint by end-2026.

- Putting a finer point on it, "Those who favored lowering the target range for the federal funds rate generally judged that such a decision was appropriate because downside risks to employment had increased in recent months and upside risks to inflation had diminished since earlier in 2025 or were little changed." But "Those who preferred to keep the target range for the federal funds rate unchanged at this meeting expressed concern that progress toward the Committee's 2 percent inflation objective had stalled in 2025 or indicated that they needed to have more confidence that inflation was being brought down sustainably to the Committee's objective."

- Indeed the bar to a January cut remains high - the holdouts even appeared to suggest that they were concerned that a December cut would be shown as unwarranted in retrospect: "Some participants who favored or could have supported keeping the target range unchanged suggested that the arrival of a considerable amount of labor market and inflation data over the coming intermeeting period would be helpful in making judgments on whether a rate reduction was warranted."